How People With Disabilities Obtain The Best And Lowest Life Insurance Rates | If You Are Disabled, Here’s How To Purchase Life Insurance The Right Way!

Updated: April 12, 2024 at 9:39 am

People with disabilities may feel life insurance is out of reach.

That’s not entirely true. People with disabilities can obtain life insurance.

If you have a disability, life insurance is likely available.

You just need to know the life insurance options for your situation.

We have helped many people with disabilities obtain the best life insurance rates for their situation. I am sure we can help you, too.

Here is what we will discuss:

- Life Insurance Underwriting For Disabled Individuals

- Types Of Life Insurance Available

- How To Obtain The Best And Lowest Life Insurance Rates

- What If You Work?

- Life Insurance For People Who Receive SSDI?

- Life Insurance For People Who Receive SSI

- Life Insurance Options for Disabled Children

- Case Studies On Life Insurance And Disabled Individuals

- Now You Know Disabled Individuals Can Obtain Life Insurance

Like most of our articles, we start with a discussion of underwriting. Why? It is the foundation of the life insurance application process. Moreover, it helps to set the right expectations for your specific situation. It is also how you will obtain the best and lowest life insurance rates for your situation.

Life Insurance Underwriting For Disabled Individuals

Contrary to popular belief, people with disabilities can obtain life insurance. The amount of life insurance and type available depends on your condition and disability.

How carriers determine your insurability is through a process called underwriting. They look at your overall situation and then analyze your situation against actuarial and risk tables. If everything looks good, then they will approve your application.

If your situation doesn’t fit, then they will decline your application.

Here’s the thing. Every carrier underwrites differently. So, carrier A may decline your application, but carrier B approves it. Moreover, some carriers offer simplified underwriting where the underwriting process is quicker and easier.

Generally speaking, carriers will look at the following during the underwriting process:

- Your health situation

- Financial / credit

- Motor vehicle records

- Lifestyle situation

- Public Records

- Anything else that allows them to underwrite

In your case as a disabled individual, life insurance carriers will look at the nature of your disability in more detail. They will want to know:

- The type of disability

- Diagnosis date

- Any surgeries

- Do you have gainful employment?

- The medication you are on

- Any hospitalizations?

- Do you need help with activities of daily living

- Is your disability related to a mental impairment or nervous disorder?

- Is there a guardianship or POA required for care?

Carriers are going to want to know how your disability impacts your everyday ability to function and live.

I call it “life functionality”.

If your disability negatively impacts your life and ability to function, then the carrier increases your life insurance rate or declines your application altogether.

But that doesn’t mean a disability is an automatic decline. No.

How A Disability Plays A Role In Functionality And Life Expectancy

For example, many carriers allow a high-functioning adult with autism, who is independent and maintains a job, to obtain life insurance. The same goes for someone who is deaf or blind.

On the other end, many carriers will decline a person with down syndrome.

They will also likely decline a person with severe schizophrenia, but they will approve someone with stable bipolar disorder.

Why? As I mentioned, the difference has to do with the person’s life functionality and longevity. A high-functioning adult with autism, independent and holding a job, should live a normal age life than a person with down syndrome, in which the life expectancy is age 60.

The life expectancy of a person with severe schizophrenia is around age 65.

These examples bring us to an important point. Carriers look at life functionality and longevity when reviewing someone with disabilities.

So, again, how you live your life with your disability matters to the life insurance carriers.

Of course, declines happen. If you can’t work due to your disability, that in itself can have a negative effect. The inability to work due to PTSD, depression, anxiety, drug abuse, or anything else has a negative effect.

However, life insurance options still exist for these situations.

Moreover, if you have additional health conditions including your disability, such as smoking while diabetic and disabled, the carrier will likely decline you. Co-morbidities, as the industry calls them, have a drastic, negative effect.

One last point to outline here. If you are disabled, not working, due to a mental illness, or substance abuse, carriers limit life insurance options.

Life Insurance Options For People With Disabilities

Let’s discuss the types of life insurance available for people with disabilities. The type will depend on your situation.

Term Life Insurance For People With Disabilities

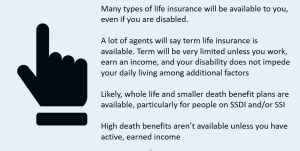

As we indicated earlier, the type of life insurance available depends on the disability. If you are able-bodied and fully working, then carriers should offer you a complete array of term life, whole life, or any other type of life insurance.

Remember that term life insurance contains level premiums for a “term” such as  10 years, 20 years, or 30 years. Term life insurance costs the least per dollar of death benefit coverage. We believe term life insurance is the most appropriate life insurance coverage.

10 years, 20 years, or 30 years. Term life insurance costs the least per dollar of death benefit coverage. We believe term life insurance is the most appropriate life insurance coverage.

Depending on your disability, you may have to pay an extra premium, called a table rating.

A rating should be the least of your concern. What matters the most is getting the coverage in place, first, to protect your family. We can discuss premiums later. By working with an agency like My Family Life Insurance, which must keep your best interests first, you can be certain you’ll receive the right life insurance for your situation.

A couple of things to note. Carriers underwrite term life insurance thoroughly. One of the underwriting factors for term life is earned income or salary. So, if you don’t have gainful employment, term life insurance likely is not an option.

Feel free to search for rates here. Note that rates change, and they could be higher based on your situation. However, these rates will give you an idea of the cost.

Permanent Life Insurance

Then, there is permanent insurance. These are types of life insurance that last your entire lifetime. Whole life insurance is the most common permanent insurance.

Whole life is more expensive than term life insurance for the same dollar death benefit. Why?

(1) Premiums last your “whole life”. In other words, whole life insurance policies are underwritten to pay a death benefit.

(2) It contains cash value.

Then, universal life comes into play. A guaranteed universal life policy can work really well for those seeking long-term protection (almost or nearly permanent) without the whole life insurance premium cost.

Again, if you work and your disability does not present an issue with your life functionality, then permanent life insurance is an option.

However, if you are disabled, you do not work, and your disability presents a life functionality issue, then permanent life insurance likely is not available.

Contact us if you would like permanent insurance of $75,000 or greater.

Burial Insurance – Simplified Issue Whole Life

Burial insurance is a type of whole life insurance policy. It contains a small death benefit like $25,000 or $35,000.

Just as it sounds, people use burial insurance to fund their burial, funeral, and end-of-life expenses.

Contrary to what people may say, people with disabilities can obtain burial insurance, and rather easily.

If you have a moderate to serious disability which impacts your everyday life, burial insurance likely is your only option.

Underwriting is very simple (hence, “simplified”). Usually, carriers require a health questionnaire filled out and/or a phone interview with an underwriter. Note: many carriers are eliminating the phone interview step.

There are two subcategories of burial insurance. Those policies that offer an immediate benefit and those that offer a delayed or graded benefit.

Obviously, obtaining an immediate benefit is your priority. If you have a policy with an immediate benefit and die the next day, your family receives the death benefit money.

A policy with a delayed, or waiting period, benefit pays the full death benefit after a period of time has elapsed. If you pass away within the waiting period, some carriers pay a percentage of the death benefit to your beneficiaries. After the waiting period, the death benefit is available in full.

Usually, people with more severe disabilities obtain these types of life insurance.

These policies are good for disabled individuals as they accept many types of health conditions and they do not underwrite for financial / earned income.

Guaranteed Issue Life Insurance

I wrote about the 5 types of burial insurance not to buy, and I listed guaranteed issue life insurance as one of them.

I like guaranteed issue life insurance. It fills a need for many people. However, I included it in that article because most people opt for a guaranteed issue life insurance policy when they could qualify for something better.

A guaranteed issue life insurance policy is simply a whole life insurance policy with no health questions. The issuance is guaranteed. You apply, pay the first month’s premium, and then you have life insurance.

Easy!

However, because the carrier does not underwrite, it does not know the health status of applicants.

What would you do in this case if you were a carrier?

I’d increase the premium or maybe add some limitations.

Correct? Guaranteed issue life insurance comes with a 2-year waiting period, typically, because no underwriting.

We work with many guaranteed issue plans. Feel free to search below. Make sure your health status is set to “poor”.

Nevertheless, a guaranteed issue life insurance can prove valuable for people with disabilities, depending on their situation. For example, it is usually the best option for individuals who have a POA or guardianship.

We also work with a guaranteed issue term carrier. You can self-enroll here.

How Do People With Disabilities Obtain The Best And Lowest Life Insurance Rates?

Here are how people with disabilities obtain the best and lowest life insurance rates.

- Analyze your situation and set reasonable expectations on life insurance availability. I can’t stress this point enough. For example, if you don’t work, do not expect carriers to insure you for large death benefits. You should also understand that rates, likely, will be higher because of the impact on your “life functionality”

- Contact us and tell us your situation

- We will analyze your options and offer recommendations

- When you are ready, we will have you apply with us. Usually, we do everything over the phone or via video conference. There is no need to meet in person.

- Depending on your situation, the application process could take a day to a few weeks.

Do we at My Family Life Insurance get approvals for our clients all the time? No. Sometimes, carriers decline our clients. We’ve analyzed the reasons which typically fall into 2 buckets:

- Forgetting an important piece of information about your background, like bankruptcy or felony

- Think your condition is stable, but your doctor indicates it is moderate to severe

However, I would say that we at My Family Life Insurance have a good record of getting our clients the best rates on their life insurance, provided they were transparent with their situation and background.

Life Insurance Options If You Are Disabled And Work

People who work full-time with disabilities likely will have many life insurance options including term life insurance.

As I mentioned earlier, your working ability matters to life insurance carriers.

It is really the best situation.

Depending on your situation, you might have a table rating.

For example, we have insured many adults with high-functioning autism. Technically, they are disabled.

We have also helped working professionals who are deaf or blind obtain life insurance. Moreover, those with bipolar disorder (link).

If you work full-time, and your disability is stable causing no life functioning issues, chances are term life insurance is available.

Additionally, carriers may offer:

- whole life

- universal life, including indexed universal life

- return of premium term life

- and more

You can check out some example premium rates in the quoters above.

However, the best thing to do is to contact us about your situation. We can help.

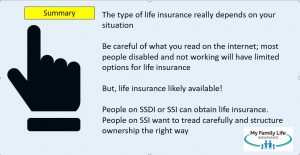

Life Insurance Options For People Receiving Disability Benefits Or Social Security Disability Income (SSDI)

At this point, you hopefully understand that nearly all disabilities are insurable as long as your disability is stable and not impeding your life functionality.

We search and work with over 60 carriers (we work with many), because all the carriers underwrite your disability differently.

Here’s a problem some people run into. Some people who have disabilities don’t work.

We described the benefits of working earlier. Working doesn’t guarantee policy approval, but it sure does help.

If you don’t work, are receiving disability benefits, or are receiving social security disability income (SSDI), your life insurance options are limited.

In these cases, the fact that you are receiving SSDI indicates you have a long-term and debilitating disability that affects your everyday lifestyle. You aren’t working. Most term life insurance carriers will decline you.

Just look at this excerpt here.

For example, a person with diabetes (type 2) called us recently. He was looking for $250,000 of term life insurance. Nowadays, carriers insure people living with diabetes all the time. The problem: he was receiving SSDI benefits and was disabled due to his diabetes. No chance a carrier covers him for that amount.

But other options exist.

Before we get into those options, people with SSDI can obtain life insurance. Many agents say otherwise. Having life insurance does not prevent you from receiving your disability benefit. There is no asset or resource test with SSDI.

Burial Insurance Available For People On SSDI

You can still obtain life insurance, though. If you are receiving SSDI, you could obtain burial insurance as we described earlier.

Depending on your age and your condition, you could receive an immediate benefit. We’ve worked with many individuals with disabilities and on SSDI and have been very successful in placing them on burial insurance policies.

We would pick the carrier based on your situation and disability.

Feel free to check out estimated quotes. (Again, we reserve the right to send you a thank you email or say hello via phone, but we don’t sell your info or bombard you a billion times a day with phone calls.)

Guaranteed-issue life insurance could likely be the best choice for you if you have a severe disability. As we described earlier, there are a number of these plans available.

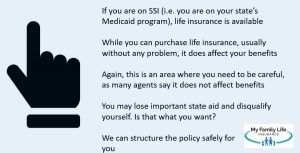

Life Insurance Options For People On SSI – Supplemental Security Income

If you receive SSI, supplemental security income, your options are very limited, but by no means a dead-end.

If you receive SSI, you are likely on Medicaid. As we wrote before, you can receive Medicaid and purchase life insurance. You just need to go about it the right way.

You see, receiving SSI is based on an asset and resource test. To make a very long story short, if you earn income and have assets above the SSI threshold, you will likely lose your SSI benefits.

Medicaid considers cash value life insurance like whole life insurance as an asset. It could terminate or reduce your Medicaid benefits if you have too much cash value in the life insurance.

Many agents get this wrong, to the detriment of the insured-applicant. I’m floored about that. Even the social security administration states that cash-value life insurance is an asset resource. The same for burial contracts, which are also an asset.

Whole life insurance is an asset. That means a whole life insurance policy, guaranteed issue or a traditional burial insurance policy, could negatively impact your SSI benefits. IF (purposely capitalized) you own the policy.

Life Insurance Options For People On SSI / Medicaid

There are a couple of ways around this. You could:

(1) have someone else, like a son or daughter, own the policy, as long as this person is not on Medicaid him or herself. He or she would be the owner. Having someone else own the policy on you should not affect your SSI benefits. We have helped many people in this regard. Please reach out to a lawyer in your state if you have questions

(2) open a funeral trust and transfer or pay money into the trust. Medicaid can’t get at the money in the trust. It is not an asset. It will not affect your SSI benefits.

(3) utilize simplified issue term life insurance. We work with one term life insurance plan that works well with people receiving Medicaid. Term life insurance has no asset value.

(4) enroll in a guaranteed-issue term life insurance plan (if available in your state)

(Note: we are not experts in estate planning or Medicaid law. We recommend consulting with a lawyer who is an expert in this area in your state.)

What About Disabled Children And Life Insurance?

What About Disabled Children And Life Insurance?

We all want the best for our children. Purchasing life insurance on a child is one of the ways people like to insure the next generation.

You may think children with disabilities are unable to obtain life insurance. That is not true. We have helped many families obtain life insurance on their disabled children.

The right type of life insurance, as we have said, depends on your situation. For example, we have helped many families obtain life insurance for their autistic children. We have also helped many families obtain life insurance on children with down syndrome.

Many carriers work great in the children’s life insurance market, even for those children who are disabled.

Life Insurance Options For Disabled Children

Sometimes, a guaranteed issue type of life insurance is the only option. However, as of this writing, the guaranteed-issue market for children has changed considerably.

If you have a disabled child and want life insurance on his or her life, you have come to the right place. Here is how we can help. You may need to purchase a small policy yourself and add a child rider to your policy. Here are the options for your disabled child:

- a small whole life insurance policy on yourself. One carrier we work with will allow up to $15,000 whole life insurance, guaranteed issue, from ages 0 to 17.

- A small term life insurance policy with a guaranteed issue child term plan from 0 to age 25

- Another term plan where you can purchase up to $10,000 of life insurance on a child, age 0 to 25, convertible to permanent insurance (recommended).

- If you are a non-military federal employee, purchasing a $50,000 of guaranteed issue life insurance allows the purchase of $10,000, guaranteed issue, on a child or grandchild from age 0 to 25

- Up to $10,000, guaranteed issue, whole life insurance, age 0 to 75. Anyone over the age of 17 would need a POA or guardianship with appropriate verbiage. Your child can’t have applied AND been declined for life insurance during the previous 2 years (approximately, timeframe subject to change).

So, you still have options, but many of these options require the parent to apply and be approved for life insurance.

Case Studies Where We Have Helped People With Disabilities Obtain Life Insurance

Here are a few real cases where we have helped people with disabilities obtain life insurance.

Here are a few real cases where we have helped people with disabilities obtain life insurance.

Do we obtain approval every time? Not every time, unfortunately.

As I mentioned earlier, declines stem from our clients not being transparent about their situation or forgetting about some important aspect of their background.

But, these 3 cases should give you an idea of what is possible.

Man With Loss Of Use Of Left Arm

64-year-old man, non-smoker, retired due to a work disability where he lost the use of his left arm.

Healthy every other way. Wanted to apply for $75,000 of whole life insurance.

We found him $50,000 and $25,000 immediate-benefit policies.

Woman On Medicaid

55-year-old woman on SSI / Medicaid. Has schizophrenia and other health issues. Non-tobacco user, but does smoke marijuana about 3 times a month.

We placed her in a graded benefit term life insurance policy. She is the owner of the policy. We later enrolled her in a small whole-life plan in which her daughter is the owner and payor on the policy.

Man With Bipolar Disorder And Sleep Apnea

We had a 52-year-old real estate professional looking for $500,000 of term life. His bipolar disorder and his sleep apnea were both stable. He did not miss any work from his bipolar disorder and was never hospitalized.

We were able to get a carrier to approve him for the $500,000 at table 3 rating.

Now You Know People With Disabilities Can Obtain Life Insurance

There are many life insurance options for people with disabilities. The right plan for you depends on the nature of your disability and how the disability affects your everyday life.

If you work and are independent, you have more life insurance options. You may have to pay an additional rate because of your disability. However, a decline is unlikely to happen.

If you are on SSDI or on SSI, your options are limited. Moreover, people on SSI should consider someone else to own the policy or purchase a term plan. It is always recommended to speak to a qualified attorney in Medicaid cases as state laws change.

Don’t know what to do or where to start? That is why we are here. Contact us or use the form below.

We would be more than happy to help you with your life insurance needs. As usual, we only work in your best interest and nothing less. That means if there is a plan or policy elsewhere which works better in your situation, we will direct you to that solution.

Working in your best interest is the only way we know how to work with our clients.

Learn More

Are you interested in learning more about the information in this article? Please fill out the form below, and we will email you additional information or give you a call. We always work in your best interest. By entering your information, you are providing your express consent that My Family Life Insurance may contact you via e-mails, SMS, phone calls, or prerecorded messages at any phone number(s) that you provide, even if the number is a wireless number or on any federal or state do-not-call list. Additionally, you understand that calls may be placed using automated technology, and that consent is not a requirement for purchase. Your information will NOT be sold and will remain private. However, you may opt out at any time. We respect your privacy first and foremost. By contacting us, you agree to receive text messages from our number (800) 645-9841. If you no longer wish to receive text messages, you may opt out at any time by replying "STOP".

Published by

14 thoughts on “How People With Disabilities Obtain The Best And Lowest Life Insurance Rates | If You Are Disabled, Here’s How To Purchase Life Insurance The Right Way!”

Comments are closed.

I’m looking for life insurance to cover my disabled son. He is 30 and has autism I’m his legal guardian.

Hi Joyce – Thank you for reaching out. I will send you an email, and I hope we can chat soon.

John

I am a bisabled man born 1967 that needs life insurance for myself to cover my funeral expenses.

Hi George,

Thanks for reaching out to us. I will send you an email shortly with more information.

John

Hi I am looking for life insurance for my 22yr disabled son that has autism. Everywhere has turned him down due to his disability.

Hi Pearl,

Thanks for your comment. We likely can help you and your son. I will email you some additional information, and I hope we can touch base soon.

John

My cousin is mentally disabled and I can’t find I death insurance for him he is 46 and I’m his legal guardian

Hi Elizabeth,

Thanks for reaching out to us. Depending on the state you live in, we can help. I can email you more information shortly.

John

As a 100% disabled combat Veteran and 82nd Airborne Bn Scout Recon with PTSD but good physical health it is extremely defeating that no one will “take the risk” of insuring me so that my family will be taken care of, even though my disability is a result of fighting for the very people that deny me. I took the risk on their behalf, to see they didn’t have to fight, so they could take care of their families.. only to turn their backs on mine.

Thanks for your service. It is because of people like you, I am able to write in freedom, work in freedom, have religious freedom, sleep in freedom. From my heart, I do thank you for your service.

PTSD diagnosis can be tricky, but we have helped veterans in similar situations.

If you’d like to chat, I am happy to. (800) 645-9841

John

Need life insurance. Been on disability over 10 years

Hi Steven,

Thanks for reaching out to us. I appreciate it.

Can definitely help you out. You can give us a call at (800) 645-9841 X 1.

Here’s a summary of what we would need to know:

(1) age

(2) nature of your disability

(3) have you applied elsewhere? If so, with whom?

(4) other basic information such as height/weight, tobacco use, etc

It’s a simple process, and we have helped many people on disability obtain the life insurance they need.

John

Im interested in life insurance

Hi Robert,

Thanks for reaching out. I’ve tried to reach you several times. We can definitely help if you want life insurance.

John