Why Life Insurance On Children Makes Perfect Sense | We Discuss Why You Should You Buy Life Insurance For Your Child

Updated: April 12, 2024 at 9:39 am

We receive this question a lot from parents. Scour the internet for “life insurance on children” and you will read some scathing reasons from financial “experts” why purchasing life insurance on the life of children is a waste of money.

We receive this question a lot from parents. Scour the internet for “life insurance on children” and you will read some scathing reasons from financial “experts” why purchasing life insurance on the life of children is a waste of money.

Some of the reasons they state we agree with. Yes, we do! (We get into that later.)

However, these experts are missing an important component of life insurance that makes coverage on children beneficial.

In this article, we discuss the benefits and when to buy life insurance on your children. We also discuss when you should not buy life insurance on your child, too.

Confusion Abound With Life Insurance On Children – Let’s Get The Misinformation Out Of The Way

Many financial experts and planners make confusing statements about life insurance. We see this confusion more when you buy life insurance for your child.

insurance. We see this confusion more when you buy life insurance for your child.

The first one: many of the articles describe life insurance as an investment. Life insurance is not an investment. A mutual fund is an investment. A stock is an investment. Life insurance is risk protection. Let’s get that out of the way.

A little bit later, we will describe the different types of life insurance available to children. One option is term life insurance. If you know anything about term life insurance, then you know that term life is NOT an investment. This is like saying your homeowners or auto insurance is an investment.

Sure, some types of life insurance contain cash value. But, it’s not an “investment” in the traditional sense.

The second part is that the experts suggest you should put that money elsewhere, like in a 529 college savings plan. We could not agree more! You should open and contribute a 529 plan for your children!

However, the experts seem to imply that the premium money you save will be much more than the value of life insurance. It is not. Let’s provide an example.

A $50,000 whole life insurance policy on a newborn boy might cost $30 per month. Let’s say, instead, you put that money into a 529 plan each month that earned 8% annually on average. How much do you think you will have in the account in 18 years when the boy is ready for college. Do you think it will be more than $50,000?

The Answer Is…

No. You will have a lot less. You’ll have a little more than $14,000. In 18 years, who knows how much college that $14,000 will buy. With the life insurance, the child, assuming good health, will have day 1 coverage of $50,000 to protect his or her life (likely more, depending on the type of life insurance). Moreover, he or she will have other advantages (we describe those advantages later).

Some also suggest that burying a child is inexpensive, so you should have the money on hand. Like in an emergency fund! Geez…we would all like to have the money on hand. However, many don’t even have emergency savings at all! If you look on the internet, many people can’t even spare $500 to pay for an emergency. We aren’t talking about the poor here. Rather, middle-income Americans. Where will the money come from? A church collection? Borrow from your home equity? Maybe a retirement account, I suppose…Fact is, burying a child does cost money and most Americans don’t have it on hand.

Moreover, consider the pain of experiencing the loss of a child. Can you go back to work the next week after something like that? Probably not. The life insurance benefit allows YOU to take needed time off.

They Are Right About One Thing

The experts are right about one thing. They say that children have no “income value”, so there is no need for life insurance. In other words, if they pass away, there is no income impact on the family because children, generally, do not work and do not contribute to the economic value of the household.

That is true. They don’t usually have income value.

However, they miss the point again. While true, there is usually not any “income value” (unless the child is an actor or does earn money), there is “love value”. I argue that love value is stronger than income value.

Here Are The Reasons Why You Should Buy Life Insurance On Your Children

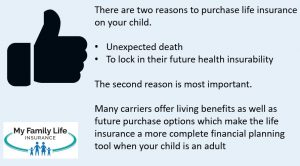

There are really only two reasons you should buy life insurance on your children. One, however, has more importance.

The first reason is that, unfortunately, children do die. Having some type of life insurance policy will mean that funds are available. Yes, the probability of a child’s death is low…thankfully. Does that mean you should ignore it? If the worst-case scenario happened, how would you pay?

The first reason is that, unfortunately, children do die. Having some type of life insurance policy will mean that funds are available. Yes, the probability of a child’s death is low…thankfully. Does that mean you should ignore it? If the worst-case scenario happened, how would you pay?

Moreover, as we addressed, could you go back to work immediately? Probably not. I know I could not. I would need time away to get my thoughts together with my family. A death benefit provides some income while dealing with this unfortunate incident.

The Main Reason To Purchase Life Insurance On The Life Of A Child

Here is the main reason to purchase life insurance on children. It is to guarantee their future insurability when they are adults. What does this mean? Simply put, because they are healthy now, you lock in their health.

Some experts brush this away like it is no big deal. But it is a big deal. This is important. Let’s say your child develops a condition that renders him or her rated or declined as an adult. Juvenile diabetes always comes to mind. If your child develops juvenile diabetes, that is generally a rating or a decline for individual life insurance as an adult.

Moreover, more and more health conditions are linked to hereditary. Genetics do play a part.

Some policies allow your child to purchase more life insurance in the future, as an adult, without any evidence of health insurability. These are the kinds of policies we like. It is an option. So, if your child has a debilitating condition as an adult…doesn’t matter. He or she can purchase MORE life insurance. This is how you show your love to buy life insurance for your child.

Additionally, some plans offer “living benefits” attached to life insurance. Living benefits allow the owner of the policy to advance the death benefit early for the following situations:

- a critical illness diagnosis like cancer

- a critical injury

- nursing home care or assisted living needs

Having this flexible option makes the life insurance policy a near-complete protection plan for your child. Really, it protects their family (i.e. your grandchildren),

And, let’s hope not, but there is money in place to bury your child if the worst-case scenario should happen. Maybe there is some extra available that you can take time off or get some counseling. I have three children myself, and I know I would.

When You Should Not Buy Life Insurance For Your Child?

Some people should not buy life insurance on their children. Here are some situations below.

If you are very affluent, then you probably don’t need to purchase life insurance on your children. You have money for the worst-case scenario. But, most people don’t.

Also, if you don’t have your stuff (saying it nicely) straight on your own finances, you shouldn’t buy life insurance on the life of your child.

Most adults don’t have enough life insurance for themselves or none at all. Purchase some. Or, buy some disability insurance if you don’t have any. Did you know that you are more likely to face a long-term disability than die unexpectedly? There are better ways to show your love to your children. Getting your own financial stuff straight is one way to do that.

Should The Grandparents Buy Life Insurance?

This is an option. Many grandparents want to do something for their grandchildren. One way is to contribute money to a 529 college savings plan. (Yes!)

The other is purchasing life insurance for their grandchildren. The grandparent would be the owner of the policy. If you are comfortable with that, that is one option. If you want to learn more how this would work, please contact us. We can discuss how this would work. Most carriers are lenient with grandparents purchasing life insurance on their grandchildren.

Life Insurance Options Available On Children

Many agents say there is only one type of life insurance available on the lives of children. But, there are three options. We discuss them here.

Indexed Universal Life Insurance

I am sure you have heard of indexed universal life insurance (IULs). Agents espouse the potential “income tax-free” cash value all the time.

While IULs can be complicated, and there are many disadvantages, they can make sense for children.

There are several reasons why:

- the child is young, and has a long-term ability to grow the cash value

- you can start with a minimum amount to get coverage in place, and then adjust premiums higher over time. The ability to “overfund” an IUL is a major advantage

- policies with living benefits make the plan a strong, long-term financial planning tool when your child becomes an adult

You may spend around a minimum of $50 per month for $100,000 or $250,000 depending on the age of your child.

Most plans offer a future purchase option for your son or daughter to purchase more life insurance regardless of their health situation. Again, as we said, that is an important reason to buy life insurance on children.

I like IULs for children a lot; however, in my opinion, they do require some understanding. They can be rather complicated, but we do a good job of breaking down these complicated components into an easy-to-understand format. Contact us if you would like to learn more.

Whole Life Insurance

Just as it sounds, whole life insurance is designed for the insured’s whole life. If you can afford whole life insurance, that is great. You may spend around $30 per month for $50,000 on a newborn boy and $20 on a newborn girl. Whole life will have cash value. The cash value will grow, but, as we said, don’t get too hung up here. What you want is a policy that offers a future purchase option that the child can purchase (when an adult) with no evidence of insurability. And, if the child never has to use it, great.

you can afford whole life insurance, that is great. You may spend around $30 per month for $50,000 on a newborn boy and $20 on a newborn girl. Whole life will have cash value. The cash value will grow, but, as we said, don’t get too hung up here. What you want is a policy that offers a future purchase option that the child can purchase (when an adult) with no evidence of insurability. And, if the child never has to use it, great.

Whole life insurance on your child can make sense. Premiums are low, usually around $30 per month, give or take. (Sorry, “experts”. What can a family do with an extra $10 to $30 per month which I previously described?)

Whole life has level premiums (i.e. they never change). The premiums periods are for life, 20-year pay, 10-year pay, or pay to age 65. These options are “paid-up” options. Contact us to learn more about these options.

Term Life Insurance

Term life insurance is available and offers the lowest cost of protection for your child.

It is designed to last only a set number of years. For children, though, term life insurance on children usually lasts up to age 25. You want a term life insurance policy that will convert to whole life with no evidence of insurability. Nearly all juvenile term life policies offer this option. However, you also want a policy that, once converted, will give you guaranteed purchase options. These options come with no evidence of insurability.

Term life is very affordable. A $20,000 or $25,000 term life plan may cost $25 to $30 a year. (Maybe a bit more depending on the carrier). Yes, a year. How much college will $30 a year buy in 18 years? Just over $1,100. That won’t buy a lot of college at all!

A word to the wise with all of these options. You had better have life insurance for yourself. A carrier will not approve your child if you have little to no or very little life insurance on yourself.

Now You Know Why Life Insurance On Your Child Makes Sense

We hoped you learned why life insurance on children makes sense. In our opinion, there are two reasons:

(1) children do unfortunately die. You will have money in case this happens.

(2) more importantly, your child has a future purchase option with no evidence of insurability. It is like a “call option”. If your child doesn’t need it, great! If so, though, the ability to purchase more is there.

Are you considering life insurance for your child? Do you need assistance with determining which carriers are right for you? We can help. We can also help if you are on the fence. Some children don’t need life insurance. Other parents need to focus on their own financial situation before considering life insurance for their child or children.

We only work in your best interest. We are beholden to you and your family, not to an insurance carrier. If we can’t help you with your situation, we will point you in the right direction and part as friends. Contact us today or use the form below.

Learn More

Are you interested in learning more about the information in this article? Please fill out the form below, and we will email you additional information or give you a call. We always work in your best interest. By entering your information, you are providing your express consent that My Family Life Insurance may contact you via e-mails, SMS, phone calls, or prerecorded messages at any phone number(s) that you provide, even if the number is a wireless number or on any federal or state do-not-call list. Additionally, you understand that calls may be placed using automated technology, and that consent is not a requirement for purchase. Your information will NOT be sold and will remain private. However, you may opt out at any time. We respect your privacy first and foremost. By contacting us, you agree to receive text messages from our number (800) 645-9841. If you no longer wish to receive text messages, you may opt out at any time by replying "STOP".