3 Types Of Disability Insurance Available For Tattoo Artists | We Discuss This Important Insurance That Pays You If You Are Sick Or Hurt And Can’t Work

Updated: April 12, 2024 at 9:39 am

We have said this before: disabilities do not discriminate. They affect the young, the old, the rich, the poor, the executive, the construction laborer, the accountant, and the tattoo artist. To properly protect themselves and their family, income-earning tattoo artists should protect their wealth and income with disability insurance.

We have said this before: disabilities do not discriminate. They affect the young, the old, the rich, the poor, the executive, the construction laborer, the accountant, and the tattoo artist. To properly protect themselves and their family, income-earning tattoo artists should protect their wealth and income with disability insurance.

John, I don’t need any, you say.

I hear that all the time from tattoo artists. They feel a disability only happens to someone else.

If you are a tattoo artist, have you ever thought about what would you do if the paycheck you just received was the last one for a year? That happens to many people, including tattoo artists.

How would you pay your bills? Seriously?

What would happen to the lifestyle you worked so hard for?

Additionally, if you own your tattoo business, what would happen to it? Honestly, if you went without income protection, you probably would have to close it down.

In this article, we discuss disability insurance for tattoo artists. Here is what we will discuss:

- Why Is Disability Insurance So Important?

- Disability Insurance Underwriting

- Disability Insurance Basics

- 3 Types Of Disability Insurance Available

- Disability Insurance Costs

- Other Options

- Final Thoughts

Let’s jump in and discuss what is disability insurance.

What Is Disability Insurance For Tattoo Artists?

Let’s say you suddenly have sharp pain in your right hand. Well, you need to use your hands to do your job, right? You go to the doctor. After a series of tests, the doctor diagnoses you with Fibromyalgia. She says you need to rest and that you must limit your work as a tattoo artist if the pain is too great. You miss work.

Here is another situation. You are stopped in your car at a stop light. The light turns green and you proceed normally. Suddenly, you are hit from the side by another car that ran his light (text messaging while driving). You are injured and will be out of work for an extended period of time. You are out of work.

Or, you felt sluggish and not yourself for a few months. Your doctor runs tests. An oncologist indicates that you have leukemia and need to start treatment. You’ll be out of work.

What is common here?

I am missing work?

Yes, but more importantly that these are all disabling situations. These situations (and many more of them) prevent you from earning an income. How will you pay your bills: mortgage, credit card, utilities – if you can’t work and earn a paycheck?

Enter disability insurance. Disability insurance pays a monthly benefit to you if you miss work due to a disabling injury or illness. The monthly benefit amount is usually a percentage of your income.

Notice, though, that these scenarios are not necessarily job-related. It is true. Most disabling injuries and conditions are not job-related at all. In fact, the council for disability awareness states that most disabilities are from illnesses.

That means the likelihood of a disabling injury happening from your actions as a tattoo artist is low.

3 Reasons Why Disability Insurance Is So Important For Tattoo Artists

Moreover, 1 out of 4 working adults experiences a long-term disability greater than 90 days. This stat comes from the Social Security Administration. If faced with a disability without disability insurance, do you have any money saved in case you can’t work for 3 months, a year, or longer? Probably not.

than 90 days. This stat comes from the Social Security Administration. If faced with a disability without disability insurance, do you have any money saved in case you can’t work for 3 months, a year, or longer? Probably not.

That’s the first reason. It’s true. But, we have life insurance, right? Moreover, you have far less of a chance of your house burning down or getting in a car accident. Yet, we have homeowners and car insurance. Why?

There’s value there, John!

Yes, but there is even more value in your ability to work and earn an income. Your work as a tattoo artist funds all those nice things. What happens if you can’t fund them?

Secondly, a disability can last a long time. Some stats say the average claim is 36 months. The claims departments I speak with tell me 18 months. Nevertheless, can you live off nothing for 3 years? Two years? Six months? I doubt it.

“Your family is the most important reason to buy disability insurance.”

Finally, the last reason is the most important one. It is your family who loves you the most. It’s not your clients. I know you appreciate them, but they’ll just move on to another tattoo artist if you are sick or hurt. Your family won’t. So, if anything, the main reason disability insurance is so important is that it protects families, keeps them in their homes, and gives you some peace of mind.

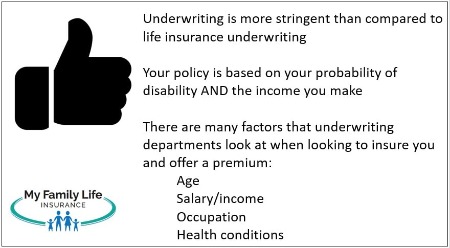

Disability Insurance Underwriting For Tattoo Artists

How do those stats make you feel? Worried? Concerned? They should. Luckily, disability insurance is available for tattoo artists. First, though, it is important that you understand how carriers underwrite disability insurance.

Disability insurance underwriting is a bit different compared to other types of insurance. Disability insurance underwriters are really insuring 2 factors:

- your future chance of disability (we already provided stats around that) and

- your income

They do this by reviewing your:

- occupation

- income

- health

- anything else material to the approval decision

If you meet their underwriting qualifications, then they will approve your application for disability insurance. We discuss these underwriting aspects in detail next.

Why Does Your Occupation Matter?

Your occupation matters. An easy, comparative example: You would agree that a construction laborer has a higher likelihood of disability than an accountant working at a desk, right?

Your occupation matters. An easy, comparative example: You would agree that a construction laborer has a higher likelihood of disability than an accountant working at a desk, right?

Yes, of course!

This is why your occupation matters.

Wait, John, you say. You just said that most disabilities are by illnesses. That isn’t necessarily job-related. What gives?

Good question. While the statistics show that most disabilities are from illnesses, people are disabled through their occupation. Back, wrist, arms, hands, and leg injuries are more prone in some occupations than others.

The tattoo artist occupation is no different.

Carriers rank or classify occupations from 1 to 5 or 6, with 1 being the most prone to occupational disability and 5 or 6 being the least. All things being equal, a person working in an occupation classified as a 1 pays a higher premium than a person in an occupation classified as a 5.

Even though the tattoo artist occupation has existed for centuries, only recently have carriers insured the occupation. Crazy, right? Maybe you have faced this yourself with other agents telling you their carrier won’t cover tattoo artists.

However, we at My Family Life Insurance work with a few carriers that will insure tattoo artists.

Additionally, many carriers have work requirements. They want to see you working in your job for at least a year and working 30 hours/week or more. The 30 hours/week is considered “full-time”. If you currently work part-time (those working between 20 and 29 hours per week), we still have disability insurance options for you.

Why Does Your Income Matter?

As discussed earlier, carriers insure your income. So, your income matters.

Carriers pay a percentage of your earned income, usually between 60% and 70%. If you are a W-2 employee, they use your gross wages as your income. If you are self-employed, they use your net income off of your tax return. The distinction has importance. You want to make sure you use the right income for disability insurance. Most tattoo artists we have worked with are independent contractors/self-employed. You want the net income number off your business tax return.

Many carriers have a minimum income requirement. Most carriers require a minimum annual income of $10,000 gross W-2 wages or net income.

The higher the income you make, the higher your monthly benefit. The higher your monthly benefit, the higher your premium, all things being equal. Is this a bad thing?

NO! Remember, they are insuring your income in case you can’t work due to a disability.

You can always apply for a lower monthly benefit amount. Why would you do that, though? If you do and are disabled, you will receive a lower benefit than what you need. However, we do work with a disability insurance rider that does allow you to purchase more disability insurance in the future.

While some coverage is better than no coverage, you should strive for 100% coverage. There are many ways to afford disability insurance. You just have to determine what is important. Having some protection for your family or none at all?

Why Your Health Matters?

Of course your health matters. We just mentioned that most disabilities are illnesses and sicknesses. A person who currently has type 2 diabetes will have to pay more for disability insurance versus someone who is healthy. Is that fair? Yes. Why? Because the person who has type 2 diabetes has a greater chance of a disability than someone who is healthy. Just a fact.

illnesses and sicknesses. A person who currently has type 2 diabetes will have to pay more for disability insurance versus someone who is healthy. Is that fair? Yes. Why? Because the person who has type 2 diabetes has a greater chance of a disability than someone who is healthy. Just a fact.

OK, John, I get that, you say. But, what happens if I am diagnosed with a health condition later?

Good question.

You are covered, no problem. As long as the condition or injury is not pre-existing, disability insurance covers you for really anything.

And what if you do have pre-existing conditions?

Every carrier is different, but likely they all will have an exclusion of coverage, limit your benefit, or a combination of both. Really depends on your situation.

We wrote about pre-existing conditions in our guide and in our disability underwriting article.

You will want to review both articles.

Health conditions are why you want to protect your income and wealth with disability insurance as soon as possible.

Why? Again, carriers typically exclude pre-existing conditions. You don’t want health conditions to exclude coverage or, worse, prevent you from obtaining disability insurance at all.

The moral of this section. If you don’t already have disability insurance, and your family will suffer financially upon your disability, you need it NOW.

Anything Else?

The carriers consider anything else material to your chances of disability. Do you like to skydive? Smoke marijuana? Drink alcohol…too much?

Have speeding tickets or recent, at-fault accidents?

All of these are lifestyle or hazardous choices that affect your disability insurance premiums.

Do you like to drive…really fast? And, have you been caught? Yup, those speeding tickets matter.

Any bankruptcy, liens, or payment issues? Those matter, too.

People ask me why financial characteristics play a part. Would you insure someone who has a history of not paying bills or liens? Right, probably not.

Remember, carriers are looking at your chances of disability. If you participate in hazardous activities or have non-preferred lifestyle choices, those will affect your premiums, benefit, benefit periods, or a combination of all.

Carriers aren’t discriminatory here. To reiterate, they are determining your chances of disability.

That’s OK, John, you say. I just won’t tell them about it.

Well, you can certainly do that. Keep in mind that disability insurance is 24-hour coverage. What does this mean? Let’s say you smoke marijuana from time to time. You don’t disclose this on the disability insurance application. One day, you smoke too much, and you trip down the stairs. You break your back and tear your ACL. You can’t work. Will the carrier cover you?

Maybe…maybe not…In my experience, I lean towards “no”, but it depends on the overall situation.

So, remove any doubt. You are better off disclosing any hazardous activities and lifestyle choices, paying a higher premium, and knowing you have peace of mind.

Disability Insurance Definition Basics For Tattoo Artists

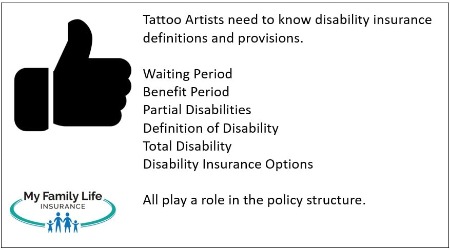

You now have a good dosing of why tattoo artists need disability insurance and how underwriting works. Now, let’s get into the plan provision basics.

These are definitions tattoo artists need to understand.

These are definitions tattoo artists need to understand.

Waiting Period – the time period before you are eligible for disability insurance benefits. For example, you can have a waiting period as low as 30 days. This means once the carrier approves the claim, you must wait 30 days before becoming eligible for disability benefits. Once you are eligible, the carriers send your disability payments 30 days later. In effect, you receive your payment 60 days from the date of disability.

During the waiting period, you receive NO disability payments. You must balance the waiting period with your premium cost and your personal savings.

Benefit Period – the benefit period is how long you can receive disability benefits. For example, a 5-year benefit period means you receive benefits for a maximum of 5 years.

Total Disability – a disability in which you can’t work 100% of the time and receive your total disability benefit

Partial Disability – a disability in which you can work partially (less than 100%). The carrier pays you a partial benefit based on the time and/or income lost due to the disability.

Definition of Disability – carriers base your disability payment on your disability definition. You really want own occupation definition whenever possible. Why? An example will explain.

Why The Definition Of Disability Matters For Tattoo Artists

We consider the plan’s definition of disability as the heartbeat of your plan. An example makes this clear.

Instead of a tattoo artist, let’s use a vocalist, full-time, as part of a symphony. She has a disability insurance policy that contains the own-occupation definition. One day, she loses her voice and her doctor says she can never sing again. She receives a disability payment because her policy is based on her own occupation as a vocalist. She can’t sing!

You can see the importance of this “own-occupation” definition. Carriers pay you a benefit if you can’t perform your occupation, even if you can do something else. The vocalist can likely do something else, but she receives a disability benefit.

What if her plan was not “own occupation”? Then, the carrier could assume, based on her education, skills, and experience that she could work in an office instead as a vocalist. In this case, she has the unfortunate “any” occupation definition. This definition is similar to the social security definition (link). This is the main reason why social security declines so many people.

The own-occupation definition gives you much more flexibility and peace of mind. Among other requirements, carriers pay you a benefit if you can’t perform the major duties of your “own occupation” even if you can work a different occupation.

Disability Insurance Riders For Tattoo Artists

Many disability insurance riders exist for tattoo artists.

Riders are “add-ons”. These riders make it easier to customize your needs.

However, as we wrote in our article, we feel some of these are worth the money and some aren’t.

You will want to make sure the riders serve their purpose for you. Like adding accessories to a new car, adding riders increases your monthly premium.

Several riders I feel are worth it, though. These include the:

Enhanced partial/residual disability benefit: allows a partial benefit if you can work, just not full-time. Typically, this benefit pays based on your income loss due to your partial disability. It also pays when you are coming off of a total disability and returning to work.

Be aware. Many carriers say they already have a partial disability benefit. This is true. Sort-of. However, you have to read the definition. Most plans state a partial disability pays only after a total disability. You want to avoid this. It means if you can work part-time, you won’t receive a partial benefit until only after that disability transfers to a total disability. Some disabilities can remain a partial disability for a long time. It behooves you to pay the extra money to have this flexibility.

Guaranteed Insurability Option: this allows you to purchase more disability insurance in the future. No additional underwriting is required. In other words, once the carrier approves you, you can buy more disability insurance in the future without any medical underwriting. How great is that?

Every carrier is a tad different here, so you want to thoroughly read the parameters.

We believe the:

- Own-occupation

- Enhanced partial/residual benefit

- Guaranteed insurability option…

…creates a formidable disability insurance plan for tattoo artists.

How Can You Get Disabled?

Before we get into the types of disability insurance for tattoo artists, let’s talk about the different ways one can get disabled and not work.

(1) from an illness or condition like cancer or multiple sclerosis

(2) an injury on the job

(3) an injury off the job

(4) gradual wear and tear which may or may not relate to your occupation. For example, you develop carpal tunnel syndrome in your wrists. Or, you have a progressive, degenerative knee problem. Or, degenerative eye/sight loss.

A disability can occur from anything. Keep in mind, though, that the average long-term, disability lasts around 2 to 3 years. So, throw those images of people in wheelchairs out of your mind. While a catastrophic disability does happen, thankfully the probability is low.

This is why disability insurance for tattoo artists is so important. There are, conceivably, an unlimited number of ways to a disability.

3 Types Of Disability Insurance For Tattoo Artists

Three types of disability insurance exist for tattoo artists. We discuss them here.

#1 short-term disability insurance. These plans pay a benefit for disabilities of a short duration. The waiting period can be as low as 7 days and the benefit period 3 or 6 months.

Be aware here. The carriers that offer short-term plans generally do not cover partial disabilities. So, you have to determine if the short-term insurance is worth the cost.

Most of the time, an emergency savings plan is a “short-term disability insurance plan”. As a CFP® Professional, I actually recommend this savings route over a short-term disability insurance plan.

However, you will have to determine if short-term disability insurance is worth the money. Contact us. We are here to give transparent and honest answers.

#2 long-term disability insurance. These plans pay a longer benefit. It is these plans that help you and your family if your disability lasts for 6 months, a year, or longer.

I recommend these plans. If you want a “combination” short-term/long-term plan, we can set up your waiting period at 30 months.

#3 Accident-only disability insurance. These plans pay only if you are disabled due to an accident, with 24-hour coverage.

Since a majority of people don’t suffer a disability from an accident, you can expect premiums are low. Are these worth it? They can be. Remember, accidental injuries could lead to a disability.

Bonus: Disability Insurance Coverage For Tattoo Artist Business Owners

Are you a business owner or self-employed? If so, you can enroll in a policy that will pay your business expenses upon a disability. The policy is called a business overhead expense policy.

will pay your business expenses upon a disability. The policy is called a business overhead expense policy.

You use the disability benefits to pay for business expenses like rent, fees, taxes, etc.

Premiums are tax deductible. If structured properly, benefits are income tax-free as well.

This type of policy will ensure your business remains solvent during your inability to work from a disability. This is an additional reason why tattoo artists need disability insurance.

Additionally, we also work with a good disability insurance carrier on the group employer insurance side. Remarkably, you could insure yourself and someone else in your company, assuming you have employees (not independent contractors).

Moreover, the carrier we like to use will insure husband/wife/spouses 2-person companies and family-owned companies.

Depending on the number of participants, you could apply at guaranteed issue (which means no medical underwriting)! Family members and spouses can apply, which is usually not the case with most small group insurance plans. Monthly benefits are up to $7,500 per month. This is another opportunity for tattoo artists to purchase disability insurance.

Disability Insurance Cost For Tattoo Artists

Everything sounds good, right? But, you want to know the answer to the most important question.

Everything sounds good, right? But, you want to know the answer to the most important question.

How much does this all cost?

Yes! You read my mind!

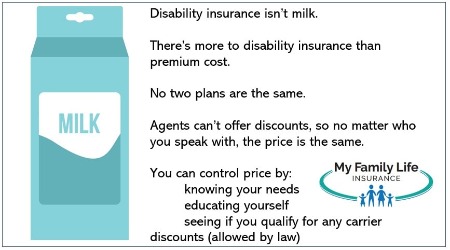

First, let me stress that buying disability insurance isn’t like buying bread and milk. It is not a commodity, and “shopping around” is wearisome. It is a waste of your time.

You can’t get it cheaper elsewhere. Insurance premiums are regulated at the state level. Every broker and agent offers the same price. The difference is knowledge, carrier option/availability, and structuring a policy to meet your needs and budget.

Having said this, remember the intention of disability insurance. It pays a benefit if you are sick or hurt and can’t work. As we discussed, that can happen and is common, too.

So, while you won’t spend thousands and thousands each month for coverage, you may have to spend $100 to $200 each month, maybe more and maybe less.

The premiums correspond to everything we discussed in the underwriting section. If you make great money as a tattoo artist, expect to pay a higher premium to insure that income (all things being equal).

Is $200 per month a lot? Maybe for milk, it is. But disability insurance isn’t milk.

$200 per month equates to about $6.67 per day. That is a latte or a sandwich every day.

I think you’ll agree with me that, if you make a claim, the $200 monthly premium (or whatever it is) is worth every penny.

Alternative Types Of Disability Insurance Coverage For Tattoo Artists

There are other types of coverage that can replicate that of a disability insurance policy. Are they perfect? No. They aren’t disability insurance. They do not have the same coverage as a disability insurance policy for tattoo artists, but they can provide monetary support.

There are plans that can pay lump sum benefits in case you are in an accident with injury or diagnosed with a specific illness.

If you are in an accident or suffer a covered accidental injury, an accident insurance policy pays a fixed benefit based on the accident or a lump sum payout. You use the money any way you would like. You can use the money to pay for medical bills, utility bills, groceries, etc. The plans we like offer 24-hour coverage.

If you are diagnosed with cancer, heart problems, or any other covered disease or condition, a critical illness plan pays a similar way. Many plans pay a lump sum – say $100,000 – to you for whatever you want. Again, that can be mortgage payments, groceries, even a trip to Disney World if you want. Moreover, there are plans that pay a smaller monthly benefit, but help with monetary assistance through your treatment and recovery. The type you pick is up to you.

These plans are useful if you are declined for disability insurance. Moreover, you can carry these policies well beyond age 65, making them useful in case you need them in old age.

Now You Know The Types Of Disability Insurance Available To Tattoo Artists

Tattoo artists can obtain disability insurance. In this article, we discussed the importance of disability insurance, underwriting, and several options available.

Are you ready to discuss? Unlike other agencies, we aren’t the bothersome types that call you day and night. Contact us or use the form below.

We will follow up with a phone call or email usually within 24 to 48 hours.

In our conversation, we want to get to know you and your needs. Moreover, unlike many other agencies, we have duty of care to you. What does this mean? We put your interests first, not our own. This means if there is a better solution available that we can’t provide, we inform you of that solution and put you in touch.

Learn More

Are you interested in learning more about the information in this article? Please fill out the form below, and we will email you additional information or give you a call. We always work in your best interest. By entering your information, you are providing your express consent that My Family Life Insurance may contact you via e-mails, SMS, phone calls, or prerecorded messages at any phone number(s) that you provide, even if the number is a wireless number or on any federal or state do-not-call list. Additionally, you understand that calls may be placed using automated technology, and that consent is not a requirement for purchase. Your information will NOT be sold and will remain private. However, you may opt out at any time. We respect your privacy first and foremost. By contacting us, you agree to receive text messages from our number (800) 645-9841. If you no longer wish to receive text messages, you may opt out at any time by replying "STOP".

Published by

2 thoughts on “3 Types Of Disability Insurance Available For Tattoo Artists | We Discuss This Important Insurance That Pays You If You Are Sick Or Hurt And Can’t Work”

Comments are closed.

Would like to get a quote for disability insurance

Hi Eder,

Thanks for reaching out to us. You can give us a call at (800) 645-9841 X 1 or use the contact us link on our website. I’d be happy to give you a call or schedule a time to discuss your options.

John