Disability Insurance Guide For Truck Drivers [Learn Your Options & Save Money]

Updated: June 30, 2024 at 9:58 am

Truck drivers probably don’t think about disability insurance much, right?

Truck drivers probably don’t think about disability insurance much, right?

You know the importance of getting your shipments and loads on time. Your customers rely on you to be on time, unload your shipment, and ensure the shipment is in good order.

Then, you are on your way to your next destination.

People rely on you to do the job, to do the job right and fast.

What happens if you don’t earn a paycheck because of an injury or an illness? How will you pay your mortgage, car payments, home utilities, or even your truck payment if you own your rig?

If you have a family, how would you be able to pay for things?

Would your spouse have to work (or work more)?

Who would be able to watch the kids?

How would you modify your life so that you still have money coming in to pay for the lifestyle you and your family are accustomed to? (Hint: without disability insurance, you would likely have to make serious, potentially life-changing decisions.)

Disability insurance answers those questions. This is a comprehensive guide about disability insurance for truck drivers.

The difference between our guide and other online articles is that I go into great detail about disability insurance. This is a rather lengthy guide, so please use the navigation below to jump between sections if you wish.

Additionally, I don’t sugarcoat. If there is one occupation that needs disability insurance, it is the truck driver / delivery driver occupation.

- Why Trucks Drivers Need Disability Insurance

- The Types Of Disability Insurance Available For Truck Drivers

- The Kind Of Truck Driving Matters

- The Makings Of A Good Disability Insurance Policy For Truck Drivers

- Disability Insurance Underwriting For Truck Drivers (And, Why Some Truck Drivers Avoid The Application Process)

- The Premium Cost Of Disability Insurance

- How To Save Money On Your Disability Insurance Policy

- Protect Your Truck & Other Disability Insurance Options For Truck Drivers

- Final Thoughts

Let’s begin with why truck drivers need disability insurance.

Why Truck Drivers Need Disability Insurance?

Ask yourself this question:

Ask yourself this question:

“If you got hurt or sick yesterday and can’t work, how would you pay your bills today?”

Figuring things out, hoping, and praying (in this case) are not valid answers.

Crickets…

You see, your lifestyle and everything you have worked for are driven by your ability to work. The computer, tablet, or cell phone you use to read this article is likely paid for by your earnings as a truck driver.

But, John. I am not going to get sick or hurt! I am healthy!

Yes. I hear that all the time from professionals. They are healthy now, and they don’t think a disability can ever happen to them. Let’s define what a disability looks like. Contrary to what you think, a disability is not necessarily someone in a wheelchair. In terms of disability insurance, a disability is really any illness or injury that prevents you from doing your job as a truck driver. So, that could be:

- back pain / back problems

- a broken arm or leg

- cancer

- heart attack

- diabetes

- shoulder and arm problems

- hip and knee issues

- nerve issues that prevent you from properly using your extremities

and on and on…

A disability does not discriminate. It does not matter if you are brown or white, a man or a woman, or a CEO or truck driver. You face the same dilemma with a disability without disability insurance: how will you pay the bills if you are sick or hurt and can’t work?

Disability Occurrence Data From The Social Security Administration

The Social Security Administration states that the probability of having a disability is 1 in 4 workers.

I am not making it up. You can look up the statistics yourself.

Additionally, other articles state that a “long-term” disability is any illness or injury that lasts longer than 90 days. That is 3 months.

Think about that for a moment. Every 3 or 4 workers, someone can’t do his or her job, and he or she potentially will be out of work for 90 days or more.

That person isn’t earning money and is unable to provide for his or her family.

Contrast this probability to the probability of unexpected death, say from a motor vehicle accident, which is 1 in 114. Even dying from cancer has better odds: 1 in 7.

So, the answer to the question I posed above is disability insurance. Disability insurance pays your bills today if you can’t do your job as a truck driver.

People Forget Who Is Most Important

Hands down, truck driving is one of the most important functions in our economy.

I know your job is very important. However, you have to remember that there is also a group of people who are more important. Who can be more important than my job and customers, you think? They pay the bills.

True. They do, but they don’t love you as your family loves you. By far, if you have a family, your spouse and children rely on you more than you think. They love you more than anything.

So, disability insurance is more about protecting them if you can’t provide an income. The fact that you are looking into this now shows me you are responsible and love your family.

As I posed in the introduction, if you don’t want or feel the need for disability insurance, you’ll have to answer some tough questions if faced with a disability.

- Would you and your family be able to continue your standard of living without your income?

- If not, what changes would need to be made?

- Would your spouse have to work?

- Would you need to sell your home to make ends meet? (This actually happened to a person who contacted me. Her husband unexpectedly faced a long-term illness. The only way she said they could make ends meet was to sell their home. Unfortunately, it was too late for them. A disability insurance policy that covers your mortgage helps. Anything can help.)

- Who could be flexible with the children should you be disabled?

- What do you do next?

The tough questions can go on and on.

What Will Disability Insurance Pay For?

We will discuss the monthly benefit later in the article, but your benefit from your disability insurance policy can pay for:

- your mortgage

- any car payments

- your medical expenses and medical bills

- groceries and utilities

- children’s daycare

- school

- anything

Again, disability insurance pays a monetary benefit if you are sick and cannot perform your job as a truck driver.

But, John. I have workers compensation insurance through work. Won’t that cover me?

I hear this response a lot. Great. You have workers compensation insurance. Every employee does. It is state law.

The issue is that workers’ compensation pays only for a disability that occurs on the job, usually due to an injury.

While your chances of a truck driver getting an injury on the job are greater than mine, the risk of an on-the-job injury is still low.

Most disabilities are from illnesses like diabetes, cancer, or heart disease. Additionally, musculoskeletal issues like lower back pain, knee issues, shoulder and neck issues. Moreover, mental disorders such as anxiety or bipolar depression are leading causes of a disability.

The Types Of Disability Insurance For Trucks Drivers

There are really 3 types of disability insurance available for truck drivers. We will discuss other options later in the article.

The 3 disability insurances include:

- short-term disability insurance

- long-term disability insurance

- accident-only disability insurance

Many people ask us about the difference between short-term disability insurance and long-term disability insurance. Here’s the difference.

Short-term disability insurance is really designed for a disability that lasts a short time period. Let’s say you break your hand. Well, driving your rig with a broken hand will probably be hard, right? So, that is a disability – you can’t do your job. How long does a broken hand heal? Two to 3 weeks? Once you’ve met the waiting period (usually 7 days), you’ll be eligible for benefits and receive some disability benefits.

Long-term becomes the life-saver for those disabilities that last longer than 3 months. Cancer…a catastrophic injury…ALS…Diabetes…you name it. Most families can get by financially when a breadwinner has a short-term disability. Sure, it might be tough, but families can get by. It’s a long-term disability that can financially ruin families.

Both insurances generally use the own-occupation definition of disability. (More on that in a minute.)

We have short-term and long-term disability insurance options for truck drivers.

The Truth on Accident-Only Disability Insurance

Accident-only disability insurance is just how it sounds: it will only pay if you are disabled from an accident.

John, I can get in an accident anytime.

True, you are probably more susceptible to an accident than me. However, most disabilities are from musculoskeletal disorders and illnesses like cancer. These disabilities do not discriminate based on your occupation. You have the same chance for these disabilities as I do.

I call accident-only disability insurance a “last resort” disability insurance because it will only pay if you are disabled from an accidental event. As I mentioned, that happens, but not as often.

However, because you are a truck driver, other options exist that supplement your plan in case of an accident. We discuss these options later in the article.

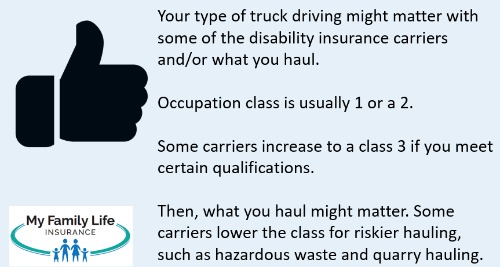

The Kind Of Truck Driving Matters For Disability Insurance Companies

The trucking industry offers many types of truck driving, including long-haul, short-haul, local delivery, and hazardous waste.

Disability insurance companies classify your occupation differently depending on the type of truck driving and/or material you haul.

Disability insurance companies classify your occupation differently depending on the type of truck driving and/or material you haul.

What do you mean, John?

All the disability insurance carriers classify occupations by the probability of a disabling occurrence.

The carriers generally classify occupations from a class 1 to a 5 or 6. An occupation with a class 6 has the lowest disability risk due to occupation, while class 1 has the highest. All things being equal, you’ll pay a higher premium if you are a class 1.

Disability insurance carriers usually classify truck drivers as a 1 or 2. Some companies we work with elevate the occupation class to a class 3.

So, what does this have to do with truck driving?

Well, as I mentioned, the type of trucking you do matters to disability insurance carriers.

Types Of Truck Driving

If you are a short-haul driver, returning home each day, carriers will likely classify you as a 2.

Some carriers may classify long-haul truck drivers as class 2 as well. However, some disability insurance companies will classify long-haul truck drivers as a class 1. Additionally, if you haul hazardous materials or work for an oilfield company, many carriers classify you as a 1. It doesn’t matter the type of truck you drive. Some companies may even decline your occupation because of the type of material you haul.

If you work for a logging company or a quarry, carriers will classify as a 1.

Carriers usually classify small, delivery and box trucking as a class 2.

Owner operators and independent contractors may be eligible for a class upgrade with many disability insurance companies. So, depending on type of trucking/hauling, a truck driver could be eligible for a class 3 risk.

This is the best risk class available for truck drivers.

Why The Low Class?

Here’s why. Continual and prolonged truck driving causes musculoskeletal issues, back pain, arthritis, joint problems…you name it. Additionally, truck drivers generally don’t get enough exercise, sitting for prolonged periods in the cab. Obesity and diabetes, among other factors, contribute to the lower class. Driving long hours at night sometimes contributes to the lower class as well.

See our list of disabling conditions above.

However, we will discuss ways you can save money a little bit later.

The Makings Of A Good Disability Insurance Policy For Truck Drivers

Our goal when designing disability insurance plans for truck drivers is the combination of value and premium.

I’m being honest here. Your disability insurance policy will cost more because of your occupation risk class. We already talked about that. That doesn’t mean you should avoid disability insurance.

On the contrary, this section discusses important provisions that you need in your policy. Knowing what you need and what you don’t need can help you save money.

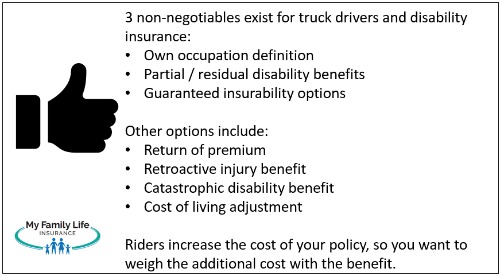

3 “Non-Negotiable” Disability Insurance Provisions For Truck Drivers

I’ve seen many competing quotes from truck drivers. They receive a quote from another broker. The quote contains every disability insurance rider available to them. The quote is expensive and causes “analysis paralysis” (or the truck driver contacts us 🙂

We believe there are certain “non-negotiable” provisions with disability insurance for truck drivers.

So, these are the 3 non-negotiables you’ll want to make sure are included in your policy:

- own occupation definition

- partial / residual disability benefits

- future purchase option / guaranteed insurability option

The first is the own-occupation definition. Luckily, many carriers make this definition of disability available for the truck driver occupation.

The own-occupation definition means that the disability insurance company pays a disability benefit if you can’t perform your own occupation as a truck driver. It pays even if you can work in another job, say as a security guard.

I believe the own occupation is an important option for truck drivers. It gives you flexibility if you can still work in a different occupation. Additionally, it prevents the disability insurance company from deciding whether to pay a benefit or not.

What do you mean, John?

Here’s what I mean. At the other end of the definition of disability spectrum is the “any” occupation. If you have this definition, the disability insurance company determines if you can perform any occupation based on your education, experience, and skill set. So, let’s say you get hurt as a truck driver, but the disability insurance company reviews your injury and thinks you can work as a security guard. If that is the case, the company doesn’t pay you a benefit.

Partial / Residual Benefits

Another “non-negotiable” feature is partial disability benefits. You’ll want this. All this means is that the carriers pay you a partial benefit if you can work, but just not full-time. Many carriers offer this, but they have a stringent definition. We work with carriers that offer an easier definition for truck drivers. In other words, you will receive a benefit after you get through the waiting period (more on that next).

Finally, the third non-negotiable is a future purchase option / guaranteed insurability option. This option allows you to buy more disability insurance in the future as your income increases. You don’t have to go through underwriting again (more on that next). All you need to do is show your income increased (through a W-2 or tax return).

Because of the severity and magnitude of disability risk for truck drivers, this is one option you’ll want to add unless you are at the top of your pay scale.

Let’s discuss the basics you need to know about your policy, followed by disability insurance riders / options that you can add to your policy.

Disability Insurance Policy Basics For Truck Drivers

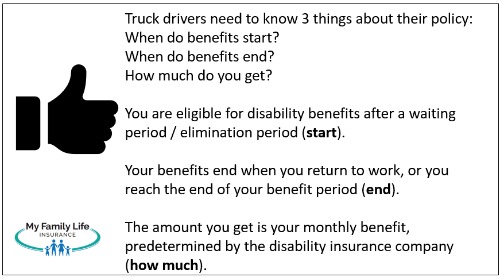

You’ll need to understand several definitions and provisions of disability insurance to make an informed decision. In this section, we will discuss:

- when do benefits start

- when do benefits end

- how much you get

When Do Benefits Start?

You’ll be covered for any injury or illness immediately after approval of your application. However, upon claim, disability benefits start after a waiting/elimination period. The waiting period is the time period that elapses before you are eligible for disability benefits. For example, if you select a 90-day elimination period and are disabled, you’ll be eligible for disability benefits on the 91st day. However, typically with carriers, you won’t get paid until day 120 or so. This means you need to have adequate savings to carry you and your family until benefits begin.

For long-term disability insurance, you can go as low as a 30-day waiting period. That means you will receive your first benefit payment around day 45 to day 60.

When Do Benefits End?

Then, you have the benefit period. Contrary to what you think, the benefit period is not how long your contract lasts. You’ll have the disability insurance as long as you pay the premium, until the contract end age, which is usually age 65, age 67, or age 70 (with a few carriers). At that point, your contract ends.

The benefit period, however, is how long you’ll receive a disability benefit for one claim.

For example, let’s say you throw out your back. That will make it hard to drive a truck, right? So, that is a disability. After the waiting period, you become eligible for benefits.

For truck drivers, disability benefits on one claim can be paid for as long as 5 years. The benefit period, in this case, is 5 years. Disability insurance companies don’t allow a benefit period longer than 5 years due to occupational risk.

You may think that a 5-year benefit period is too short. Actually, being disabled for 5 years is a very long time. Most disability claims are settled within 24 months. Therefore, a 5-year benefit plan should be OK.

(Note: if you are interested in a “to age 65” benefit period, we do have options for select truck drivers if you own your own company and have bonafide employees. See our “other options section” below for more detail.)

How Much Do You Get?

Your monthly benefit is how much you get. The salary or income you earn derives the monthly benefit.

If you are an employee, most carriers will allow a monthly benefit of 60% of your salary. For example, if you have a gross monthly salary of $5,000, the carrier insures $3,000 (60%).

If you are an employee, most carriers will allow a monthly benefit of 60% of your salary. For example, if you have a gross monthly salary of $5,000, the carrier insures $3,000 (60%).

However, if you are a self-employed contractor or owner-operator, some carriers will insure 70% to 80% of your net income.

What is net income? It is your gross business sales receipts minus business expenses. Let’s say you earned a gross income of $300,000, but your truck note and other trucking expenses cost $200,000. Your net income is $100,000. This is the insurable number. Why?

This is the number you’ll use to pay your house mortgage, utilities, food, insurance, etc. That is why.

But, John, you say. I owe a note on my truck. If I’m disabled, I need to pay that, too.

No worries. We discuss another type of disability insurance that covers that. We discuss that later in the guide.

Optional Disability Insurance Riders

You can add optional riders at an additional cost to your policy to best fit your needs and budget. Some can be a waste of money, and others are important. You only purchase a rider to enhance your plan. Some popular disability insurance riders for truck drivers include:

Return of Premium Rider: Returns your net premium if you never make a claim or if you make a small claim. Honestly, you can save your money here. Return of premium riders can be expensive and not worth the money.

Retroactive Injury Benefit Rider: Pays benefits from the date of total disability due to injury if disability occurs within 30 days of the injury and continues through the elimination period. This might be a viable option for truck drivers, considering the inherent risk of their jobs.

Activities of Daily Living Rider: Pays an additional benefit if you cannot perform two or more of the activities of daily living or if you are cognitively impaired. This is also known as a catastrophic disability.

Accident Insurance: Some plans offer an indemnity accident insurance plan. I think this is a viable option, with good benefits, and cheap. Considering the risk of your job, an accident insurance policy is worth the extra premium for truck drivers. The plans also will pay for an accidental death along with severe injuries or situations like ICU care or a coma.

Cost-of-Living Adjustment: This benefit increases your disability benefit by the cost-of-living IF you are on a total disability claim for more than a year. Honestly, this can be a costly rider.

We wrote a detailed article about disability insurance riders. Please contact us if you have any questions.

Disability Insurance Underwriting For Truck Drivers

John, I am ready to apply.

That sounds good. However, you need to understand disability insurance underwriting and how it relates to your premiums.

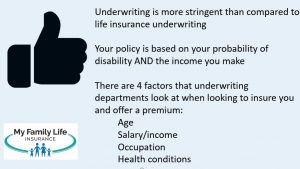

Disability insurance underwriting is more stringent than life insurance underwriting.

The reason why is that your chance of disability (as we indicated earlier) is much higher than your chance of an unexpected death.

Here is what underwriters are looking at when you submit an application:

- age and gender

- health

- occupation

- income

- lifestyle

- anything else

Age & Gender

Your age and gender impact your underwriting. Generally speaking, disability insurance companies will only accept applications from people aged 18 to 60. They usually do not accept applications from people over 60 because these people are close to Social Security retirement age. Without getting into the details, these people, if disabled, can apply for their retirement benefits sooner or withdraw their own retirement funds.

Additionally, at this age, these people really don’t need a disability insurance policy, but rather a long-term care policy.

In general, your gender matters as well. Women submit more claims than men; therefore, premiums will cost more for women, all things being equal.

Health

Obviously, your health matters.

If you are healthy with no medical conditions, you should pass health underwriting without a problem. Generally speaking, the younger you are, the less likely health underwriting will impact your approval decision and premium. This is why I encourage young professionals, including truck drivers, to apply for disability insurance.

The issue, however, is that nearly all of us have mild to moderate health conditions. That creates a lot of angst with health underwriting. Generally speaking, if you have an existing health condition prior to applying for disability insurance, that health condition is a pre-existing condition. In general, disability insurance companies exclude pre-existing conditions from coverage. In other words, if that pre-existing condition causes a disability, the company doesn’t pay a benefit.

A pre-existing clause could look something like this:

“Policy XYZ1 shall not provide benefits of any kind for any loss to the insured caused by any disease or disorder of right knee, including ligaments.”

What, John? This stinks.

It does, but you have to see this from the carrier’s perspective. You already have a health condition. If they were to cover that, your monthly premiums would be through the roof.

More importantly, while a disability can happen anywhere at any time, do you think your health condition will cause a disability?

Really think about this.

If your health condition is managed well with your physician, then I would guess a disability is going to happen (if it does) from something else.

Most people get angry when they find out a health condition isn’t covered. Rather than get angry, see what the disability insurance policy will do: it will cover you for those other situations that are covered under the plan.

Occupation

We already discussed how your occupation plays a role in underwriting. Disability insurance companies that accept truck drivers generally classify the occupation as a 1 or 2, depending on the type of driving/hauling. We work with a company that elevates the class to a class 3 for independent operators and business owners.

Income

As we indicated earlier, your income or salary plays a role in underwriting. Companies will insure (generally speaking) 60% to 65% of your gross salary (if you are an employee) or 70% or more of your net income if you are a business owner.

Lifestyle and Anything Else

Your lifestyle matters, too. Do you like to use marijuana? Marijuana use makes an impact.

Do you like to rock climb, or do you participate in hazardous activities like skydiving?

Additionally, do you have a felony or any bankruptcies? Although those don’t contribute to a disability, they do play a role in underwriting. Many carriers will decline applications from people currently on probation or who have had recent bankruptcies.

Do you regularly go to the chiropractor? That can play a role as well.

The underwriting department analyzes anything they deem material to your application.

We’ve discussed these unique situations in our disability insurance underwriting article. If you have any questions, feel free to contact us.

Why Many Truck Drivers Don’t Go Through With An Application

While we have helped insure many truck drivers, we have also had many truck drivers take a pass on an application. This is unfortunate because disability insurance is the only type of insurance that pays a benefit if you can’t work due to an illness or injury.

Your health insurance plan doesn’t do that. Neither does your life insurance (although some plans offer living benefits which is outside the scope of this article). A life insurance plan with living benefits isn’t as comprehensive as an individual disability insurance policy.

I already illustrated the need for disability insurance.

So, why do many truck drivers take a pass on an application? The main reason is that they already have some moderate health conditions. As I mentioned earlier, these health conditions, in all likelihood, would be excluded from coverage. Many truck drivers experience:

- obesity

- musculoskeletal issues with their back, neck, shoulders, and/or knees

- diabetes

These health conditions are not only excluded from coverage, but also possibly lead to a premium increase in combination with other comorbidities. For example, if you have controlled diabetes, the carrier may keep your premium stable. However, if you have diabetes in combination with a slipped disc and a bad left knee, the carrier may increase the premium for the increased risk.

This underscores the importance of obtaining disability insurance when you are healthy. If you obtain a policy BEFORE these issues arise, you are 100% covered. Moreover, no rating or premium increases.

Additionally, we can always help you save money in other ways.

We discuss premiums next.

Premium Cost Of Disability Insurance For Truck Drivers

Well, John, you say. This all sounds good, but how much will this cost?

That’s the $1,000,000 question.

The cost for disability insurance can be really expensive…or it can be really cheap.

Many agencies would gladly hand you a quote that’s hundreds and hundreds of dollars each month.

Not us. We aim to balance a comprehensive disability insurance plan versus your other needs.

Here is an example illustration.

A $2,500 monthly benefit, 5-year benefit period, 90-day waiting period for a 30-year-old-man employee truck driver costs about $125 per month.

That’s about $4 per day. You certainly have $4 each day to pay for disability insurance, right?

Conversely, if he was an independent operator, the same plan could cost around $62 per month through a class upgrade with one company we work with.

That is affordable, right? Keep in mind, this price includes:

- the own occupation definition

- partial disability / residual benefits

- guaranteed insurability option

Keep in mind that the cost of disability insurance depends on the following:

- age – this is huge. Don’t wait to apply when you are older or if you get ill or hurt

- income – if you make a lot of money as a truck driver, then higher protection will cost more

- health – obesity and other conditions might increase the cost of your policy (we discussed this earlier)

- state of residence – some states are simply higher in premium cost than other states

Having said all this, we at My Family Life Insurance have been providing economical disability insurance solutions to truck drivers for many years. I am confident we can help you out. Let’s talk about some of the ways you can save money.

How Truck Drivers Can Save Money On Disability Insurance

There are various ways truck drivers can save money on this important insurance. I’ll admit that I have seen competing quotes from other agencies that don’t even consider your other needs. Here are some ways you can save money on disability insurance. Just know that there are tradeoffs.

We talked about these throughout the article:

Use a 2 year benefit period – the average claim period from the underwriters I speak with is 24 months. A 2 year benefit period will save money and still provide “plan B” in case you are disabled.

Increase the waiting period to 90 days. Then save 3 months of expenses in case you are disabled.

Ignore some “nice-to-have” riders. Riders can make a plan extremely costly. While own occupation, guaranteed insurability, and residual disability insurance riders make sense, others, in our opinion, may not or may only if your needs warrant the extra cost.

For example, a very popular “return of premium” rider could double your monthly premium. You can easily invest this same amount on your own through an annuity or some other savings vehicle.

Contact us if you have any questions.

Protect Your Truck & Other Disability Insurance Options For Truck Drivers

This section discusses:

- how to protect the business loan on your truck

- cover your business expense commitments (other than the loan on your rig)

- group disability insurance

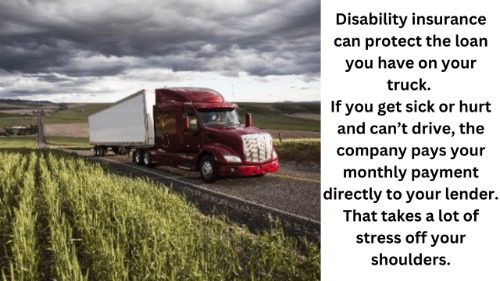

Protect Your Truck If You Are A Business Owner

Your truck is likely your largest business expense. If you have a loan or note against your truck, and disabled, how will you pay for the loan?

Oh, John. The bank will forgive me. I don’t need to worry about that.

I’m sorry, but you do need to worry about it. Banks are in the business of making money. They aren’t going to let you off the hook. You made an agreement, right, to pay the loan? The last thing you need to worry about is getting a letter or a phone call from the bank saying you still need to pay your loan when you can’t work.

I’m sorry, but you do need to worry about it. Banks are in the business of making money. They aren’t going to let you off the hook. You made an agreement, right, to pay the loan? The last thing you need to worry about is getting a letter or a phone call from the bank saying you still need to pay your loan when you can’t work.

Thankfully, a type of disability insurance exists that will pay for your loan upon a disability. It is called business loan disability insurance.

Upon a disability, the disability insurance company pays the remaining amount of your loan directly to the lender. Let’s say you have 8 years remaining on your loan. The disability insurance company pays that benefit directly to your lender for the next 8 years.

These types of plans are usually affordable because the term is short (like 5 or 10 years) and the monthly amount can be relatively low.

Having a disability insurance policy that covers your truck loan removes a lot of stress.

Contact us if you have any questions.

A Plan to Pay Your Business Expenses

If you own your own trucking business or are self-employed, you have the advantage of a policy that will pay your business expenses upon a disability.

The policy is called a business overhead expense policy. Premiums are tax deductible. If structured properly, benefits are tax free as well. This type of policy will ensure your business remains solvent during your inability to work from a disability.

A business overhead expense policy pays for:

- your truck fees and title

- any commitments you made like fuel commitments

- commerical insurances

- anything else that is a direct expense of running your business

This is an additional reason why truck drivers need disability insurance. Contrast this policy to a traditional disability insurance which pays a percentage of your income.

Carriers who offer this type of insurance typically offers a discount on a disability insurance policy. Additionally, we work with carriers that offer an occupation upgrade as well.

I recommend setting this up as a 30-day waiting period. It will cost more, but you’ll have your money much more quickly if you are disabled. Most business overhead expense policies only have a 1 or 2 year benefit period.

Note that the cost of your truck loan (if any) should not be rolled up into the business overhead expense policy. The reason is that these plans have short benefit periods.

Group Disability Insurance For Truck Drivers

If you own your own trucking business, do you have any employees?

If you do, then group disability insurance is available.

Group disability insurance is different than an individual policy. Group disability insurance is through your company. Your company is the policyholder of the disability insurance policy. You and any other employees enroll in the plan and receive a certificate instead of a policy.

Advantages and disadvantages exist with group disability insurance. The main advantage of the group disability insurance carrier that we work with is that they offer guaranteed issue disability insurance starting at 2 employees.

They also will insure husband and wife groups as well as family businesses. Most other carriers won’t.

So, think about this. You could be 5’8″ 310 pounds with diabetes and still obtain disability insurance as long as you have an employee.

John, my wife helps me and comes on the road with me. Does she count?

Yes. We have helped many husband-wife trucking companies / owner-operators obtain disability insurance this way. As long as your wife is a bonafide employee of the company, then you are both eligible.

Additionally, pre-existing conditions are covered. If you make a claim for a pre-existing condition within the first year of the plan, you’ll receive a partial disability benefit. After that 1st year, the carrier covers pre-existing conditions 100%.

Both short-term and long-term disability insurance is available.

Contact us if you are interested.

Other Insurances

If disability is out-of-reach or you are uninsurable, there are other types of insurance which act like disability insurance (but not). They are affordable, too. Here they are:

hospital indemnity insurance – the ones we like pay a lump sum benefit for hospital admission or outpatient surgery. What can you do with $6,000 in the short-term. I bet a lot.

critical illness insurance – will pay a lump sum benefit if you are diagnosed with cancer, heart disease, or some other covered condition. These plans can be a viable option for truck drivers.

accident insurance – we touched on accident insurance earlier. There are a couple of different types, all affordable. When you think about the occupational risk, an accident insurance policy is an affordable way to protect yourself.

Now You Know Why Truck Drivers Need Disability Insurance

We hope now you have a solid idea why truck drivers need disability insurance. In this guide, we discussed:

- disability insurance types for truck drivers

- why the kind of driving or hauling matters

- disability insurance policy characteristics

- underwriting

- cost

- other disability insurance options for truck drivers including those for business loans, business expenses, and group disability insurance

Confused? Don’t feel that way. We’re here to help educate you and protect your income and future. Don’t know where to start? Use this disability insurance needs analysis worksheet. Follow the instructions; it is rather easy to fill out (we at My Family Life Insurance try to make understanding insurance easy).

Next, feel free to reach out to us for our assistance or a quote. Or, use the form below. We only work for you, your family, and your best interests only. We have helped many truck drivers and families secure disability insurance to give them peace of mind.

Learn More

Are you interested in learning more about the information in this article? Please fill out the form below, and we will email you additional information or give you a call. We always work in your best interest. By entering your information, you are providing your express consent that My Family Life Insurance may contact you via e-mails, SMS, phone calls, or prerecorded messages at any phone number(s) that you provide, even if the number is a wireless number or on any federal or state do-not-call list. Additionally, you understand that calls may be placed using automated technology, and that consent is not a requirement for purchase. Your information will NOT be sold and will remain private. However, you may opt out at any time. We respect your privacy first and foremost. By contacting us, you agree to receive text messages from our number (800) 645-9841. If you no longer wish to receive text messages, you may opt out at any time by replying "STOP".