Understanding Your Long-Term Care Insurance Options | Likely Care Is In Your Future

Updated: April 12, 2024 at 9:40 am

Deciding on options for long-term care insurance has typically been filed under “head in the sand” by most families and individuals.

Deciding on options for long-term care insurance has typically been filed under “head in the sand” by most families and individuals.

If you are like most people, age 50 or older, you probably have thought about long-term care. However, you delay the decision to protect yourself and your family. Usually, the decision to learn more about long-term care insurance and the various options happens when you experience a defining and stressful moment. What are these moments?

You or your spouse receive an Alzheimer’s diagnosis.

Or your parents or in-laws need long-term care and are looking for help from you!

No longer is long-term care becoming an “if” you need it. Look at your parents, friends, and the fact that we are living longer. Long-term care is becoming a “when” you need it.

How will you pay? What is your plan?

In this article, we will discuss your long-term care insurance options. Specifically, we discuss:

- What Is Long-Term Care Insurance?

- The Myths Of Long-Term Care Insurance

- What Are Your Insurance Options?

- Now You Know Your Options For Long-Term Care

Let’s start and discuss what is long-term care insurance. You likely have a great idea.

What Is Long-Term Care Insurance?

Long-term care insurance is simply an insurance policy that covers assistance for the inability to perform activities of daily living. In other words, these are generally everyday activities. That is it. It’s not as complicated as what other organizations, agents, and agencies make it out to be. If you need help, for example, of getting out of bed, that is an inability to perform an activity of daily living.

What are these activities of daily living? There are 6 of them, and they are:

- eating

- toileting (i.e. ability to get on and off the toilet)

- dressing

- transferring

- bathing

- continence

It’s safe to say that if you need help with one of these, you need help from someone, right?

That’s where long-term care insurance comes in. It’s “long-term” because usually, your inability to perform the activity of daily living is “long-term”.

That’s what long-term care insurance is. It’s not medical insurance or anything like that, which is why health insurance and Medicare don’t cover long-term care needs. If they do, it is limited.

There are various long-term care insurance options on the market today. They all, however, have one qualification for an insured to receive benefits:

you need help with two out of six activities of living OR you have severe cognitive impairment

Long-Term Care Is Not Only Nursing Home Care…

Many people erroneously think that long-term care insurance is for nursing home care. While long-term care insurance does pay for assistance, it also pays for:

Many people erroneously think that long-term care insurance is for nursing home care. While long-term care insurance does pay for assistance, it also pays for:

- assisted living communities

- adult day care

- home health care

- other types of custodial facilities

- skilled nursing facilities / rehab

Fact is, long-term care insurance pays for coverage in several facility situations. Contrary to what you think or believe, you – generally – have no control where you end up. Your health condition and situation determine that.

With a proper long-term care insurance plan, you do, however, have more control of your assets and savings. That leads us to the one reason you want long-term care insurance.

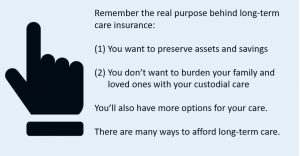

The One Reason You Need Long-Term Care Insurance

OK. There are actually 2 reasons. The two reasons are:

(1) you want to preserve your assets and savings, and

(2) you don’t want to burden your family with any potential chronic care needs

If you know anything about long-term care needs, you know the service can be very expensive. Just look up the Genworth cost of long-term care in your area. The potential costs are outrageous. Look at 20 or 30 years from now at a modest inflation rate. This underscores the importance of a long-term insurance plan.

The second reason is the family burden. I don’t need to share stories of how sons and daughters had to leave their jobs to take care of their parents. That happens all the time. You probably know of people going through that right now. Think about your foregone economic earnings. Lost time. A drastic change in family dynamics. Stress. Caregiver burnout at a maximum. None of these changes for the better anytime soon, either. In fact, I can almost guarantee your life will change forever.

That’s how one of the many long-term care insurance options help. They can minimize the negative impact of the lack of care. If you think I’m kidding, let’s talk about the myths of long-term care insurance next.

The Myths of Not Needing Long-Term Care Insurance

In our opinion, four major myths exist about the need for long-term care insurance. Here they are below.

1st Myth: You’ll Never Need Care

The first myth, that you won’t need it, is just a false statement. If you are in great  health now, you have no idea how you will be in 10 or 20 years. If you have this thinking, it is now time to stop. Remove this thinking now.

health now, you have no idea how you will be in 10 or 20 years. If you have this thinking, it is now time to stop. Remove this thinking now.

Instead, focus on the fact that you and your spouse will probably need some type of long-term care in the future. You will save yourself, your family, and your heirs time, stress, and money if you address your needs now. In fact, the Department of Health and Human Services estimated that 7 out of 10 Americans will need some type of long-term care in their future. This isn’t some made-up statistic. I am sure you will all agree the Department is not in the business of creating panic to sell long-term care policies. Rather, they are out to educate.

Myth #2: My Family Will Take Care Of Me

I have family and friends who will take care of me, you think, so I am all set. Here is myth #2: assuming people will be around to help you. Sure, you have family members or friends who may be able to take care of you if you need long-term care services. We all do. Did you ask them that? Are they willing up to give up their own time, money, livelihood, and family to take care of you? What if you need round the clock care? Or, if you need more help than your spouse, family member, or friend can provide? Assuming someone will be there to take care of you is false and can have a major, negative family and financial impact.

Myth #3: Medicare Will Pay

But, John, I don’t need to worry. I have Medicare, you say. Here is myth #3: thinking Medicare will pay for long-term care services.

Wait. You are aware that Medicare won’t cover a long-term care event, right? Medicare will assist with skilled nursing care for 100 days after a 3 day stay in a hospital. After those 100 days, all costs are on you. How will you pay? Essentially, anything with a value can be used to pay for this care. This includes your home, retirement savings, general savings, anything. Is this what you want? We didn’t think so, either.

Myth #4: I Don’t Have Assets Or Money

I only have moderate assets, you say, so I don’t need long-term care insurance. This brings us to myth #4: even with moderate assets, you might need it. If you are poor and destitute, then long-term care insurance is probably not for you. However, middle-income families could need it. As we indicated earlier, the decision to purchase long-term care insurance boils down to:

I only have moderate assets, you say, so I don’t need long-term care insurance. This brings us to myth #4: even with moderate assets, you might need it. If you are poor and destitute, then long-term care insurance is probably not for you. However, middle-income families could need it. As we indicated earlier, the decision to purchase long-term care insurance boils down to:

- do you intend to pass down the assets (including a home) to your heirs?

- do you intend to keep some of these assets for your enjoyment?

- will your family be ready and willing to drop everything in their life, quit their job, and help you?

Let’s face it. Even middle-income families need some level of long-term care insurance and planning.

There are several more myths, but the above are the most common. Do these strike a chord? They should.

The good news is that there are many types of long-term care insurance options that make planning affordable.

It is time to start talking about long-term care and analyzing your long-term care options. Next, we will discuss those long-term care insurance options.

Several Long-Term Care Insurance Options Exist

It is clear that nearly all of us will need some type of long-term care services in our future. When you think of long-term care, you probably think of a smelly and cold nursing home. Contrary to what you think, most long-term care services can take place in the home. Does that make you feel better, knowing that you have a good chance to remain in your home? And, insurance covers!

There are many options. Let’ talk about the different long-term care insurance options next.

Self Fund Your Care

While this option is not “insurance”, everyone has the option to self-fund care. This option is a viable one for the wealthy, but it is an option for everyone nonetheless.

If you want to self-fund care, and both you and your spouse end up needing long-term care services, plan to spend $500,000 of your assets or more. If you have moderate assets and wish to self-fund, expect to qualify for Medicaid (in its current state) at some point. When you officially become destitute, Medicaid will be primary payer. Be wary of state recapture provisions to pay Medicaid back. That means your house and other assets can be used to repay Medicaid.

If you want to protect some of those assets, we discuss how a funeral trust can work in protecting some of your assets.

Traditional Long-Term Care Insurance

A traditional long-term care insurance policy works very well. I personally believe this is the best type of insurance to mitigate the risks of long-term care services. There are many robust benefits including a cost of inflation benefit. Shared benefits among spouses are typical. So, if both you and your spouse purchase 3 years worth of long-term care services, in total you have 6 years to share between both of you.

The best plans nowadays are qualified plans. These plans offer tax benefits as well as asset protection (based on the state you live in). For example, if you have $500,000 long-term care insurance plan, then $500,000 of your assets are protected.

Premiums are tax deductible up to certain limits, and tax benefits are especially beneficial to self-employed individuals. Most states have partnership provisions protecting your assets as well. For example, Massachusetts has a favorable partnership plan for families who purchase long-term care insurance.

Hybrid Or Asset-Based Long-Term Care Insurance

One of the drawbacks, people say, of a traditional long-term insurance policy is the “use it or lose it” viewpoint of premiums. Why pay for something you may not use, people think? I beg to differ, but that’s how people feel about traditional long-term care insurance.

One of the drawbacks, people say, of a traditional long-term insurance policy is the “use it or lose it” viewpoint of premiums. Why pay for something you may not use, people think? I beg to differ, but that’s how people feel about traditional long-term care insurance.

Enter hybrid or asset-based life insurance. A hybrid life insurance policy or annuity utilize life insurance or an annuity with a long-term care rider. They are not as robust as traditional long-term care policy, but they don’t have the “use it or lose it” stigma as with a traditional long-term care policy.

The premise of the hybrid life-long-term care insurance goes something like this: if you don’t need the long-term coverage, then your heirs receive the death benefit. Additionally, you have cash value. So, there isn’t the “lose it” stigma that comes with a traditional long-term care policy.

I beg to differ. These plans aren’t qualified plans and don’t have the asset protection like a traditional long-term insurance policy has. However, they can fit the need for many Americans just looking for a “what if” scenario. And, affordably, too.

You can afford some type of long-term care insurance.

Short-Term Care Insurance Can Work When Nothing Else Will

Did you know that about 50% of long-term care services are for less than a year? It’s true. That leaves many people thinking if they need to insure for the long-term. Self-insurance might not be feasible. So, what do you do?

Enter short-term care insurance. A short-term care insurance policy will pay for these services of less than one year. Not all states recognize short-term care. You’ll need to need to check with your state. These policies are usually less expensive. Moreover, even those who were declined for a traditional long-term care insurance policy may qualify for short-term care insurance.

Why is that? The carrier knows these policies only pay a benefit for up to one year. After that, the insured is responsible for paying his or her care.

Talk about underwriting easiness! By knowing the maximum period is 12 months, carries can offer lower premiums.

It’s Always An Option…

Medicaid is always an option. I like to call Medicaid the payer of last resort, and it really is. Once you have spent down your assets to your state’s asset level, you qualify for long-term care services through Medicaid. If that makes you feel good, know that you won’t have many assets or your spouse to live off. You are essentially penniless. How does that make you feel? Yes, bad.

Additionally, there are state recapture rules, which means Medicaid will place a claim on your non-countable assets upon your death. If you don’t have a lot of assets, Medicaid is probably the best solution.

Likewise, those who set up an irrevocable trust, retitling most of their assets into the trust will essentially have Medicaid pay for long-term care services.

Note – the government is aware of the constraints on Medicaid. Moreover, you have probably heard about President Trump’s plan to remove some of Medicaid’s services. This is an area to pay particular attention to – democrat or republican. Expect future changes with Medicaid. Your future long-term care options here might be limited.

Now You Know Your Options For Long-Term Care Insurance

There is a real need for long-term care services in your future. Maybe not you, but probably your spouse. Start to have the discussion. Understand the long-term care insurance options. Know the advantages and disadvantages of each option. Reach out to us if you need assistance. Whatever you do, don’t stick your head in the sand and hope for the best. Hoping is not planning.

Feel free to fill out the contact form below, and we will email you additional customer literature, explaining these options in more detail. We are here to help and work only in your best interest.