Yes, You Can I Get Life Insurance For Grandparents? Here’s How | We Discuss How Grandchildren Can Obtain Life Insurance On Their Grandparents The Right Way

Updated: April 12, 2024 at 9:38 am

Many people ask me if they can obtain life insurance on their grandparents.

Many people ask me if they can obtain life insurance on their grandparents.

Yes, you can.

In fact, doing so can be a very easy process. Many life insurance companies have made it easier for grandchildren to buy life insurance on their grandparents.

Having said that, there is a process you must follow.

Moreover, other coverage options exist if your grandparents don’t want to go through the life insurance process.

Nevertheless, you can obtain life insurance on your grandparents. In this article, we discuss how.

Here’s what we will discuss:

- Checklist Of Things You Need Before Buying Life Insurance On Your Grandparents

- Other Considerations When Buying Life Insurance On Your Grandparents

- Available Life Insurance Options – And The Better Ones Designed For Grandparents

- Life Insurance Application Process

- Other Coverage Options

- Frequently Asked Questions About Getting Life Insurance On Grandparents

- Final Thoughts

Let’s jump in and discuss some of the requirements that are needed before you can buy life insurance on your grandparents.

Checklist Of Things You Need Before You Can Get Life Insurance On Your Grandparents

I understand how much grandparents mean to their grandchildren. Your grandparents have been there for you during your life, and now you want to repay them for everything they’ve done for you.

It is an honorable act that is founded on love.

However, before applying for life insurance on your grandparents, you need to know the requirements. If none of these requirements exist, then you can’t get life insurance on them.

If they don’t want to go through the life insurance application process, please see our “Other Coverage Options” below.

Insurable Interest

The insurable interest doctrine basically states that the policy owner must have a valid and ascertainable stake in the continued existence of the insured person (or property for homeowners or commercial insurance).

In other words, for life insurance, if you are financially or emotionally affected by the passing of the insured, then an insurable interest exists.

Obviously, such a direct interest exists in a grandparent-grandchild relationship.

Now, I would recommend, and prefer, a parent (i.e. the son or daughter of your grandparents. In other words, your mom or dad) to be the policy owner, as that insurable interest relationship is much stronger. However, nearly all carriers aren’t going to question an adult grandchild owning a policy on his or her grandparent.

Close, immediate family members typically follow the insurable interest doctrine. Same with people involved in a bonafide business relationship. Moreover, carriers recognize a legal guardian under the insurable interest doctrine.

A few life insurance companies might ask why the parent isn’t the policy owner, but most carriers really won’t press unless you are applying for a lot of life insurance – like $75,000 or more.

Additionally, the insurable interest doctrine applies to the beneficiary of the policy. Carriers may question the beneficiary designation on the application if insurance benefits are going to a stranger or some other distant relative or friend.

Competent Parties

Many grandchildren often overlook this requirement. Both you as the policy owner and your grandparents must have sound mind and body.

John, but my grandparents have health conditions. Does that mean they can’t obtain life insurance?

No. You can obtain life insurance on them as long as the health conditions do not prevent them from

- answering health questions,

- understanding the questions, and

- understanding the purpose of life insurance.

For example, we have had some cases where the adult grandchild wanted to obtain life insurance on his grandmother, but his grandmother had early onset Alzheimer’s.

This is a case where the life insurance company may deem the grandmother incompetent. (Note: In these cases, life insurance with Alzheimer’s is still available. However, you would need a proper guardianship form or POA.)

Additionally, the policy owner must be the age of majority, typically 18 years or older.

Free Consent

Another important requirement is that your grandparents must freely consent (i.e. no coercion) to the application process. This may be rather obvious, but there are just some people, including grandmothers and grandfathers, who simply don’t want to go through the life insurance application process (more on that later in the article). Essentially, if they don’t want to, you can’t force them.

If your grandparents don’t want to consent to the application process, then you have 2 options:

(1) save your money

(2) work directly with a funeral home on a pre-need funeral plan

Other Considerations When Buying Life Insurance On Your Grandparents

Other considerations exist when wanting life insurance on your grandparents.

Carriers have age limits: Most carriers have application age limits at age 80. A few others will accept an application up to age 85. Only a few will allow an application beyond that. If you want life insurance on your grandparents, it’s important to get it as soon as possible.

Not all life insurance is available in all states: while many life insurance options generally exist for grandparents, they are not available in every state. For example, more life insurance options exist in Texas compared to New York. The reason is due to insurance regulation, which is outside the scope of this article.

Not all life insurance is available in all states: while many life insurance options generally exist for grandparents, they are not available in every state. For example, more life insurance options exist in Texas compared to New York. The reason is due to insurance regulation, which is outside the scope of this article.

Carriers may limit death benefit options: Do you want $100,000 on your 70-year-old grandmother? Sounds easy, but that death benefit amount likely won’t happen. The reason is that your grandmother likely doesn’t have the same economic value that she had when she was, say, 40 years old compared to now age 70. However, as your grandmother, she inherently contains emotional value around love. This emotional value contains worth. However, carriers will limit this worth (i.e. death benefit) from $25,000 to $50,000, depending on the carrier.

Carriers have made the application process easier: Carriers have made the life insurance process easier for seniors. We will discuss more later, but gone are the days of a medical exam, phone interview, long turnaround times, etc. Having said that, hundreds of life insurance companies now offer life insurance for seniors and grandparents.

Contestability And Know Their Health

Be aware of contestibility and suicide clauses: Maybe this isn’t a concern to you, but I do need to mention contestibility and suicide clauses. Every life insurance policy issued in the United States has a 2-year contestibility clause and a 2-year suicide clause. The contestability clause means that if your grandparent passes away within the first 2-years of the policy, the carrier has the right to investigate the death claim and make sure no fraud took place. Additionally, if a grandparent passes away from suicide within the first 2-years, the carrier simply returns the premiums you paid back to you. After 2 years, these clauses terminate. As I mentioned, maybe these don’t apply to you, but I have seen these clauses enforced by life insurance companies.

Know their medical and lifestyle situation: Maybe obvious, but we need to know their medical and lifestyle situation BEFORE they apply. That way, we can direct them to the right carrier the first time. All parties waste too much time, especially when a carrier declines a grandparent, when information should have been disclosed from the outset.

Now that you have an idea of what is needed before applying, let’s get into the various life insurance options available to grandparents.

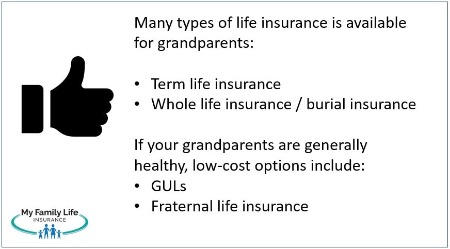

Life Insurance Options Available To Grandparents

Many life insurance options are available to grandparents. However, just because they are available, they may not be the best life insurance for them.

Note that all these life insurance options will pay out a death benefit that you can use for your grandparent’s funeral costs and final expenses, such as medical bills and any outstanding debt.

Let’s jump into the life insurance options.

Term Life Insurance For Grandparents

Depending on your grandparent’s age, term life insurance is an option. In my opinion, though, it is not the best life insurance for them. Here are the reasons why:

(1) It lasts for a set term period, like 10 years or 20 years. With a few exceptions, a carrier might offer a 30-year term period. With term life, your beneficiary receives the death benefit if your grandparent passes away within the term period. If not, then the beneficiary receives nothing. If you plan to use the death benefit amount to pay for funeral expenses and other costs, then term life insurance is not the right life insurance option.

(2) It can be harder to qualify for term life

(3) If your grandparent qualifies and accepts the policy, there is no option to renew if your grandparent’s health deteriorates and it’s near the end of the term period. Moreover, as we stated earlier, many carriers have application age restrictions. Your grandparents could be healthy as a horse, but if their term period expires and they are now beyond the application age limits, then there is no option.

Having said all this, we have helped adult grandchildren obtain term life insurance on their grandparents. It is an option. However, you must be aware that if your grandparents outlive the term, you will likely not be able to obtain additional life insurance coverage at that point.

Final Expense Insurance / Burial Insurance For Grandparents

Burial insurance is a great way for grandparents to insure themselves with life insurance.

Burial insurance is simply a whole life insurance policy with a small death benefit amount like $25,000. It is also commonly called final expense insurance as it is used to pay for end-of-life expenses like funeral expenses.

The purpose of the burial insurance is to pay for burial expenses and funeral costs. The death benefit amount goes to the named beneficiary (you as the adult grandchild or directly to the funeral home if the carrier allows that). You then, in turn, use the death benefit amount to pay for the funeral costs.

Many advantages exist with burial insurance including:

(1) easier underwriting. Many burial insurance carriers accept many health issues and health problems. For example, many will accept cancer history, heart disease, stroke, stent surgery, COPD, schizophrenia, kidney disease, etc.

(2) no medical exam required: Carriers simply ask about your medical history through a “yes/no” questionnaire.

(3) will last your grandparent’s lifetime: as long as your grandparents (or you) pay the monthly premium, the insurance carrier will pay the death benefit upon your grandparent’s passing (subject to contestability and suicide clauses mentioned above). The death benefit money will be there when you need it the most. Conversely, as I mentioned, term life will only pay a death benefit IF your grandparent passes away during the specified term.

If you’d like to see what final expense / burial insurance plans cost, feel free to quote below:

Note: different types of burial insurance exists, depending on your grandparent’s health. These types include a graded benefit and guaranteed issue whole life insurance policies. Guaranteed issue whole life insurance is typically reserved for people with moderate to severe health conditions or situations.

Other Types Of Life Insurance Available For Grandparents – A GUL

John. I searched the quoter. The monthly premiums seem expensive. My grandparents are pretty healthy for their age. They just take some cholesterol medication and lisinopril for high blood pressure.

A client said this to me in an email.

If your grandparents are generally in good health – no cancer, heart issues, kidney, liver, diabetes, etc. – then we can likely get them some low-cost burial insurance.

That is right. There are better options for healthier grandparents and these options provide a lower rate compared to the burial insurance options I presented above.

options provide a lower rate compared to the burial insurance options I presented above.

What are they?

The first one is called guaranteed universal life insurance (GUL). A GUL is a type of permanent life insurance. While I am not going to go into the details (I do so in my article about low-cost burial insurance for seniors), a GUL will last your grandparent’s lifetime but will contain little to no cash value.

What is cash value? The cash value component in a permanent life insurance policy is like a buffer. Without going into the details, cash value helps control policy expenses. In whole life insurance, it is one reason why monthly premiums are stable and guaranteed.

In universal life, premiums are not stable or guaranteed unless you have a guaranteed universal life insurance policy. Then, a GUL acts similarly to a whole life policy, but it costs a lot less.

How much less? Let’s say a healthy 60-year-old grandmother wants $50,000 of permanent life insurance. Here is a comparison (rates subject to change):

A GUL will cost about $112 per month

A traditional burial insurance policy will cost, at minimum, $152 per month.

A $40 per month savings goes a long way today.

Whole Life Insurance From A Fraternal Carrier Goes A Long Way

A whole life insurance policy from a fraternal benefits society usually is much cheaper than a traditional burial insurance policy.

Many people haven’t heard of fraternal carriers, but they are some of the oldest institutions in the US. Many of these companies have seen every economic boom and bust, and they continue to perform strong.

The reason why whole life insurance is cheaper through a fraternal carrier is because these carriers are not-for-profits. They exist to serve a non-profit mission and serve their members. When you purchase a life insurance policy, an annuity, or some other type of financial product through a fraternal carrier, you become a member. As a member, you will enjoy different benefits offered through the fraternal including charitable causes.

The revenues they earn through their insurance products pay office salaries, rent, etc. Then, the profits they earn go back to their members in the form of member benefits like college scholarships as well as charitable givings like college scholarships and other causes.

How great is that?

We work with many fraternal carriers, even more than the average broker.

Here is an example of a 65-year-old man looking for $15,000.

Fraternal carrier: $61 per month

Traditional burial insurance carrier:$81 per month

A $20 per month difference can go a long way for people nowadays.

Life Insurance Application Process For Grandparents

If you are interested in obtaining life insurance on your grandparents, then follow this easy process.

If you are interested in obtaining life insurance on your grandparents, then follow this easy process.

Contact Us: You will need to contact us. Your grandparents don’t need to be on the phone at this point, but it would be beneficial if they were.

Tell Us About Your Grandparents’ Situation: You need to know your grandparents’s health and lifestyle situation. We would need to know, for instance, their height/weight, tobacco status, medication they are on, health conditions diagnosed, and any lifestyle situations such as wheelchair use, assisted living, etc.

Carrier Selection: We review your grandparents’s situation, offer a carrier recommendation, and discuss the next steps. Most times, we will have your grandparents answer the health questions straight from the application.

Your Grandparents Apply: At this point, your grandparents need to be on the phone with us (either with you or a 3-way call). We go through the application. Your grandparents will have to answer informational questions like address, provide basic information like social security number and date of birth as well as the health questions. You will have to answer questions as the owner as well as provide a bank account for premium drafting. You will both sign the application electronically via email, so it is important your grandparents have an email address. If they don’t, then please create one for them.

Approved: If everything you and your grandparents told us checks out (carriers do look up their health history through the MIB and their prescription drug history), then carriers should approve your application.

Declines do happen still, and these declines mainly stem from not knowing your grandparent’s health status and health history or simply withholding information. As I mentioned earlier, a lot of time among all parties is saved when we know all the information at the outset.

Other Coverage Options

Other coverage options exist if your grandparents don’t want to proceed with the life insurance application process. As we said earlier, in order for the life insurance process to work, your grandparents have to freely consent to the application process.

Annuity contracts – Annuity contracts are an easy and safe way to save for final expenses. Carriers, usually, do not require underwriting. With an annuity, you just pay monthly premiums into the contract. The annuity value increases over time, either at a fixed rate or per the contract guidelines. The money grows tax deferred.

Two disadvantages exist with annuities when it comes to saving for a funeral. The first is that you may not have enough money accumulated to pay for the funeral upon your grandparent’s passing. Contrast with life insurance, which will pay the full death benefit no matter when your grandparent passes away, even if you pay one month. With an annuity, you will receive whatever the amount is contained in the annuity.

This leads us to the next disadvantage. The annuity growth is taxable to you at ordinary income taxes when you request distribution. Moreover, depending on your age, you could also face a tax penalty upon this distribution.

Funeral Trust

Funeral Trust – A funeral trust works as well. A funeral trust is an irrevocable life insurance trust. These trusts are great for people who are on SSI and need to qualify for Medicaid. You either make monthly payments into the trust or transfer some other type of asset into the trust, such as a CD, etc. The money inside grows on a tax-deferred basis (like an annuity). Upon your grandparent’s passing, the trust pays the accumulated value directly to a funeral home.

Just like the annuity, there is no health underwriting, etc. With annuities and a funeral trust, you can reach out to us. While your grandparents would still need to freely consent, the application process is even easier.

Frequently Asked Questions About Life Insurance On Grandparents

I’ve received many life insurance questions about insuring grandparents. I summarize them below with answers. Of course, if you have any specific questions, contact us or just give us a call at (800) 645-9841.

My Grandparents Are On SSDI. Can I Still Get Life Insurance On Them?

Yes, you can still obtain life insurance on your grandparents if they are on Social Security disability insurance (SSDI). In fact, we have helped many people, both young and older who are on SSDI, obtain life insurance.

I don’t want to go deep into the details, but the federal government offers and manages the SSDI plan. You are eligible through proper work credits and work history.

I Have A Grandmother Who Receives Medicaid (SSI). Can I Get Life Insurance On Her?

Yes. Grandparents who are on Medicaid / SSI can obtain life insurance. The requirements and process require care, but we have helped many individuals on SSI obtain life insurance. Contact us to learn more.

If I Have A Power-Of-Attorney Or Guardianship Form On My Grandparents, Can I Still Get Life Insurance On Them?

Yes, but it is tricky. Not all carriers accept a POA or guardianship form. Moreover, even with those carriers that do accept these forms, the POA or guardianship form must contain the proper verbiage that allows you to buy life insurance on your grandparents’s behalf.

We are one of the very few brokers that work with carriers that will accept POA and guardianship documents. The life insurance is not available in every state. Contact us to learn more. If you have specific questions, please reach out to a qualified elder care attorney as we are not lawyers and do not know the specific estate laws in each state.

If My Grandparents Have A Terminal Illness, Can I Get Life Insurance On Them?

Yes, you can. However, if your grandparent has a terminal illness, then he or she can probably only get guaranteed issue whole life insurance. Nearly all guaranteed issue policies have a waiting period of 2 years or more. If your grandparents have a terminal illness, then it might simply be best to save your money and/or work with a funeral home directly.

If My Grandparents Have A Critical Illness, Can I Get Life Insurance On Them?

Yes, many of the burial insurance carriers accept people with a critical illness like:

- cancer

- stroke

- heart disease

- multiple sclerosis

- rheumatoid arthritis

- kidney issues

- and more

As we indicated earlier in the article, contact us with your grandparents’ situation. I am sure we can find your grandparents the life insurance they need.

Can I Get Life Insurance On My Grandparents Without Their Knowing?

No. You will need their consent to proceed with the life insurance application. They will also need to answer health questions and sign the life insurance application.

As we discussed earlier, if you have a proper POA or guardianship form on your grandparents, then you could obtain life insurance without their knowing. However, you typically receive these documents on incapacitated people.

What Is The Best Life Insurance For My Grandparents?

The internet is full of superlatives like “best”, “cheapest”, and “greatest”. The best life insurance for your grandparents is the one that will insure them at the lowest possible cost. That is it.

We at My Family Life Insurance work with many life insurance carriers. I am sure we can find your grandparents a life insurance policy that fits them and you well.

Contact us if you’d like to learn more.

Now You Know How To Get Life Insurance On Your Grandparents

We hope you learned that you can obtain life insurance on your grandparents. Many carriers have made the life insurance process much easier. However, as we noted, certain requirements must be in place before applying. Notably, these requirements include having insurable interest, free consent, and competent parties.

Many life insurance options exist for your grandparents, depending on their health status and lifestyle situation.

Would you like to get started with us? Contact us or use the form below.

We have helped many adult grandchildren obtain life insurance on their grandparents. Are you afraid we will call you 1,000 times per day? No, we aren’t like that. That is bothersome, and that is the last thing we want to do. If you reach out to us, we will have an easy (i.e. not salesy) discussion about the options for your grandparents. Once we have the necessary information, we can offer recommendations, and you can decide if you want to move forward.

As always, we only work for you and your and your grandparents’s best interest. If there is a better option available that we don’t service, we will point you in the right direction as best we can. Putting your needs and best interests first is the only way we know how to work with our clients. You can always reach back out to us if your needs change.

Learn More

Are you interested in learning more about the information in this article? Please fill out the form below, and we will email you additional information or give you a call. We always work in your best interest. By entering your information, you are providing your express consent that My Family Life Insurance may contact you via e-mails, SMS, phone calls, or prerecorded messages at any phone number(s) that you provide, even if the number is a wireless number or on any federal or state do-not-call list. Additionally, you understand that calls may be placed using automated technology, and that consent is not a requirement for purchase. Your information will NOT be sold and will remain private. However, you may opt out at any time. We respect your privacy first and foremost. By contacting us, you agree to receive text messages from our number (800) 645-9841. If you no longer wish to receive text messages, you may opt out at any time by replying "STOP".