Best Disability Insurance Options For Musicians | We Discuss This Very Important Insurance Which Protects Your Income And Wealth

Updated: April 12, 2024 at 9:38 am

As a musician, you enjoy performing for audiences and creating music that impacts people. You have an extremely unique skillset matched by only a few. You enjoy your career and receive the satisfaction of what you do. However, if you are like most musicians, you probably don’t think about protecting your wealth and income with disability insurance. Or, even if you need it at all.

As a musician, you enjoy performing for audiences and creating music that impacts people. You have an extremely unique skillset matched by only a few. You enjoy your career and receive the satisfaction of what you do. However, if you are like most musicians, you probably don’t think about protecting your wealth and income with disability insurance. Or, even if you need it at all.

What if you could no longer create music or perform in front of audiences if you were sick or hurt? Have you ever thought about that?

Have you ever thought what would happen if you became sick, ill, injured, and disabled?

How would you pay your bills if you could not work?

How does this impact your family? What happens then?

Disability quickly affects your future plans and the lifestyle you worked so hard for.

In this article, we discuss disability insurance, how it protects wealth, and how musicians obtain the best disability insurance for their specific situation.

Here’s what we will discuss:

- What Is Disability Insurance?

- The Importance Of Disability Insurance For Musicians

- How Disability Insurance Protects Your Income And Wealth

- The Kind of Musician Matters (Read This!)

- Important Disability Insurance Policy Provisions For Musicians

- Disability Insurance Underwriting For Musicians

- The Best Disability Insurance Options For Musicians

- Disability Insurance Cost

- Should Musicians Apply For An Association Plan

- Final Thoughts

Let’s jump in and discuss the importance of disability insurance for musicians.

What Is Disability Insurance?

Disability insurance pays monthly benefits if you are sick or hurt and can’t perform your occupation as a musician. It is that simple. You’ll sometimes hear disability insurance as income protection insurance because that’s what it does: it replaces a portion of your income if you can’t do your job due to illness or injury.

perform your occupation as a musician. It is that simple. You’ll sometimes hear disability insurance as income protection insurance because that’s what it does: it replaces a portion of your income if you can’t do your job due to illness or injury.

So, if you can’t perform because of an injury or illness, the disability insurance company pays you a dollar benefit. You use this dollar benefit to pay for the lifestyle that you worked so hard for.

When you are back working, generally speaking, the money benefits stop. However, you still have the disability insurance policy in case something else happens or you have a relapse/reoccurring situation down the road.

Many musicians overlook disability insurance to their own detriment.

The Importance Of Disability Insurance For Musicians

We’ve written a lot about disability insurance. There are 5 reasons why disability insurance is important. We will get into those. However, they all revolve around one main theme. That theme is:

If you got sick or hurt yesterday, and can’t work at all, how will you pay your mortgage and bills today?

Honestly answer that. If your answer is, I’ll:

- Borrow,

- Raid my retirement,

- Figure it out,

- Rely on my spouse, or

- I don’t know

Then let’s have an important discussion about disabilities. Here are 3 reasons why musicians need disability insurance.

#1 A Disability Happens Often

You think a disability won’t happen to you, I know. I hear this from professionals all the time.

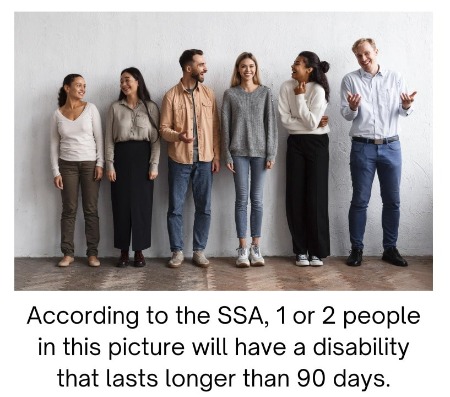

However, the probability of having a long-term disability is anywhere between 1 in 3 and 1 in 4 workers. Contrast this to unexpected death, say from a motor vehicle accident, which is 1 in 114. Even dying from cancer has better odds: 1 in 7.

But, John, I’m not going to get hurt or be in a wheelchair, you say.

That is a costly and erroneous mistake to think that way. A disability for a musician could be:

- Cancer

- Multiple sclerosis

- Lower back pain

- A herniated disc

- Neck problems

- Heart disease

- Loss of use of your hands, wrists, or fingers

- A stroke

- Torn ACL

- A permanent disability like a paraplegic injury

And on and on…

Anything illness or injury-related that prevents you from doing your job as a musician is a disability.

When we think of disability, we think of someone bound in a wheelchair, right? Not true. According to the Council For Disability Awareness, 90% of disabilities are from illnesses (like cancer) than from accidents. That means an illness or condition, such as cancer or a heart condition, has a higher probability of disabling you than a skiing accident.

#2 A Disability Can Last A Long Time

How long does a disability last?

I don’t know. A few months?

Maybe. The right answer is you don’t know.

Some internet stats say the average disability is 3 years.

The claims departments I speak with say 18 to 24 months.

Neither is right. The right answer is you don’t. You could be out of work 6 months, a year, 2 years, or longer.

Moreover, what will you do for money during that timeframe?

Look at Tiger Woods. He was disabled (he still isn’t 100% to golf) due to a severe car accident. He didn’t golf for a long time (and still struggles to this day). One second, he was fine, driving his vehicle (albeit too fast). About 15 seconds later, he was disabled.

Something like this can happen…

#3 Your Family Is Worth It

Sure, your patrons and fans are very important. However, there is a group of more important people. Who can be more important than my patrons and fans, you think? They pay my income.

Sure, your patrons and fans are very important. However, there is a group of more important people. Who can be more important than my patrons and fans, you think? They pay my income.

True. They do, but they don’t love you as your family loves you. By far, if you have a family, your spouse and children rely on you more than you think. They love you more than anything.

I talk to musicians every day about disability insurance. Many of them just overlook this important part.

If you end up disabled and not making money, you’ll have to answer some tough questions and potentially make some tough decisions.

- Would you and your family be able to continue your standard of living without your income? If not, what is “plan B”?

- Would your spouse have to work or work more?

- What happens to your business?

- Would you need to sell your home to make ends meet?

- Who could be flexible with the children? Would you have the money to hire someone to take care of the kids?

The tough questions can go on and on.

The answer to these questions is disability insurance. With disability insurance, you will have:

- Peace-of-mind

- Time to figure out what to do next

- Money

- Time to concentrate on getting better

- Plan “B”

- No worries (or less worries than if you had NO money)

Some Final Thoughts About Disability Insurance For Musicians

As a musician, you have a unique skill set that you need to insure. If you are sick or hurt, do you think you can do another job? Would you want to? Probably not!

or hurt, do you think you can do another job? Would you want to? Probably not!

You need to protect your income. Disability insurance is the way to do just that.

Additionally, you have to think about disability insurance as a spare tire or AAA. You don’t think you will ever need to use the spare tire (or AAA), but you are happy to have it when you need it.

Just like the spare tire gets you back on the road, disability insurance gets you back on the road of peace of mind. You don’t have to worry about money. You can concentrate on getting better and getting back to work.

Then, like the spare tire, once you are back at work, the disability insurance goes back in the “trunk” (sort-to-speak) and there in case you need it again.

Many people take the erroneous view that disability insurance should replace all their income and allow them to not work ever again. That isn’t necessarily true. While disability insurance provides a benefit to you if you are sick or hurt and can’t work, its intention isn’t to keep you on the couch. Disability insurance:

- Pays a benefit if you can’t work

- Provides peace-of-mind

- Allows you to get better without financial worry

- Gets you back to work

We will discuss this theme throughout the article.

How Musicians Protect Their Wealth With Disability Insurance

You should understand now how disability insurance protects your income in the event of a disability. However, have you ever thought about how it protects your wealth?

It is the most overlooked advantage, yet no one talks about it or discusses the wealth preservation advantage of disability insurance.

The average musician in the US makes about $39 per hour. If you work full-time as a professional musician (more on that in a minute), let’s say you earn $80,000 annually.

What happens to this income if you are disabled for 2 years? Yes, you lose $160,000. That’s a lot of money. Does your family rely on this income? Likely, they do.

Where will this money come from if you are disabled and can’t work? That is why I asked all those questions earlier.

I’ll use simple examples of how musicians use disability insurance to protect their wealth.

Examples Of The Importance Of Disability Insurance For Musicians

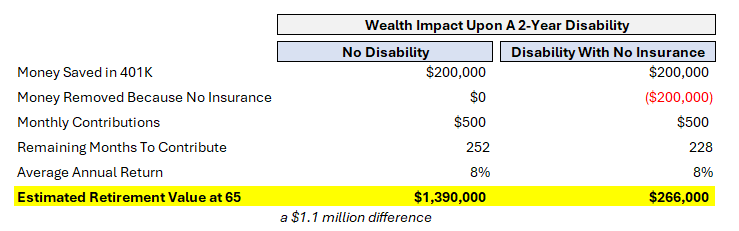

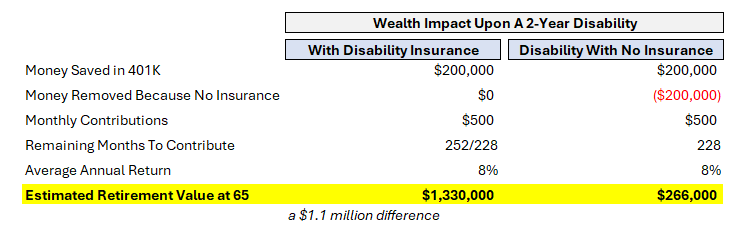

Let’s say you are a 45-year-old, male, self-employed musician. You have a consistent net income of $80,000. You have $200,000 saved through IRAs and 401(k)s and contribute $500 per month to a solo 401(k).

If you never miss work due any illness or injury, your 401(k) balance will increase to about $1.39 million at age 65, assuming consistent investment and an 8% average annual return.

Nice, right?

But, let’s say you are disabled. You got into a serious accident, and you don’t have disability insurance.

But, let’s say you are disabled. You got into a serious accident, and you don’t have disability insurance.

You need money and your spouse can only work so much. Plus, while health insurance covers some things, it doesn’t cover all expenses related to your injury. This is a fact.

So, you start withdrawing from your 401(k). Even though you pay a tax penalty for the early withdrawal, you need the money to pay for things: mortgage, kids, food, utilities, medical care, medical bills, etc. Your spouse can only do so much with the kids.

You exhaust your 401(k) completely. Thankfully, you make a recovery in 2 years’ time. You are back at work full-time.

You start your $500 per month 401(k) contributions again. But now, your retirement account at age 65 is so much different.

At age 65, your 401(k) balance is about $266,000!

Wow! $1,390,000 versus $266,000. Your 2-year disability wiped out $1,100,000 of your retirement. Why?

- You raided your 401(k)

- Your $200,000 could not compound another 20 years

- You missed 2 years of 401(k) contributions

What happens if you had disability insurance?

Here’s What Would Have Happened If You Had Disability Insurance

If you had disability insurance, you would have been in a much better position.

You wouldn’t have had to raid your 401(k). The only impact is you don’t contribute to your 401(k) for 2 years ($12,000 total).

So, using the same assumptions and variables, at age 65, you would have accumulated $1,330,000.

$1,330,000 versus $266,000. Which do you choose?

Many people tell me about the “insurance-poor” syndrome. They don’t want to buy so much disability insurance that they can’t spend somewhere else.

I get it. (Luckily, we at My Family Life Insurance take an economical approach to premium costs. More on that later in the article.) However, you see the disability insurance cost has an immaterial cost on your wealth.

Let’s say you paid $300 per month for your disability insurance. Do you think that amount is worth it? I’d say so!

Sure, we always want to pay a low and reasonable premium. But, cost should be secondary. Getting the right coverage, and getting it now, is primary.

I know. This was an easy example. But, it illustrates the impact.

Instead of your 401(k) in this example, replace it with any other assets. Maybe you would have to sell your home or borrow? Without adequate disability insurance, people do so all the time.

A disability has a serious and negative impact on your wealth if you don’t have disability insurance.

The Type Of Musician You Are Matters

John, you make great points. I am ready to apply.

Sounds great. However, before you do, disability insurance companies don’t insure every musician.

Remember, you work in the entertainment industry. Even though you possess a unique skill set of playing a musical instrument or singing, you entertain.

Remember, you work in the entertainment industry. Even though you possess a unique skill set of playing a musical instrument or singing, you entertain.

Some carriers simply don’t like that. They will decline your application immediately.

Additionally, most musicians are self-employed workers or independent contractors. Disability insurance companies want to see consistent and regular net earned income from your career as a musician. We discuss earned income later in the guide.

Having said that, not many disability insurance companies insure musicians. Look at this insurance company here. This is out of their occupation guide (more on that later). The “no” means they do not insure musicians.

However, some disability insurance companies do. Look at this one.

This disability insurance company will provide insurance coverage for musicians working in symphony, theater, or concert settings. They will decline applications from musicians who perform at night clubs, for example.

Nevertheless, we have helped many musicians obtain disability insurance. Here is a general guide to availability based on the type of musician you are.

If You Are A Part-Time Musician

We have helped part-time musicians obtain disability insurance. The parameters include:

- working over 20-hours as a musician

- not performing in a night club, tavern, bar, etc.

- generated earned income from your part-time musician work

Even if you have another part-time job, we can likely get you disability insurance.

If You Play In Rock Clubs, Night Clubs, Music Halls, Etc.

If you play predominantly in rock clubs, stadiums, etc., we can get you disability insurance.

Only a couple of carriers will accept the rock club / stadium / music hall musician. Here are the parameters:

- Need a net earned income of $100,000 or over from your music career

- Established musician with a consistent history of performing

- performing / working on a full-time basis

We have actually insured many popular musicians and artists. If you are an agent or management company representing a musician or artist, feel free to contact us. Other musician and artist management companies have enjoyed working with us because we are private, are serious, and give you our undivided attention in insuring your client. Contrary to what you may think, we really don’t need to speak to your client, either. Contact us if you would like to learn more.

If You Peform For Churches Or For A Funeral Home

If you perform in churches for Saturday and Sunday services, we have a solid carrier that will insure you. However, as we discussed before, parameters include:

- working over 20 hours as a musician

- not performing in any night club, tavern, bar, etc. on the side

- generated earned income from your part-time musician work

While we have insured many church musicians, many aren’t eligible because they only work fewer than 20 hours a week and/or have low or no earned income.

If You Are A Symphonist / Orchestra Musician

Yes. Many carriers will insure you if you perform for a symphony or orchestra. Most symphonists that we have worked with are employees. We use your gross income to determine the monthly benefits available to you.

We have helped insure many symphonists. Feel free to reach out to us if you have any questions.

If You Are A Music Teacher

Music teachers have no problem obtaining disability insurance. Most disability insurance companies accept applications from music teachers. Additionally, we work with one that improves the occupation classification to a class 5 provided the music teacher is:

- self-employed

- has worked as a music teacher for 2 years or more

- consistent earned income

- work more than 20 hours as a music teacher

As you can see, we have helped many musicians obtain disability insurance.

Important Disability Insurance Policy Attributes For Musicians

Hopefully, we have made a great case showing that musicians need disability insurance.

OK. I am now ready to apply, John.

Sounds good, but first, we really need to go over some important disability insurance policy characteristics for musicians.

Having the right foundation in place is essentially knowing what is “under the hood” of your policy.

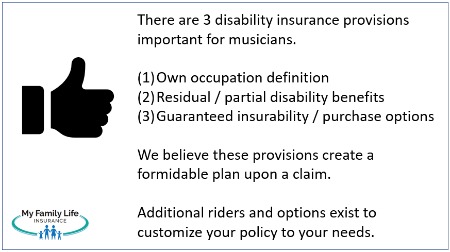

The Disability Definition Matters

The definition of disability matters.

You generally want some type of “own-occupation” coverage. Own occupation means you receive a disability benefit if you can’t do your job as a musician, even if you can do another job.

Two common types of own-occupation definitions exist (there are more, but these are the most common):

- True or pure own occupation

- Modified own occupation

True or pure own-occupation coverage means you can work in another occupation while receiving disability benefits for your inability to perform your own occupation as a musician.

It’s extremely important that musicians have own occupation coverage.

So, let’s say you damage your hands which prevents you from holding musical instruments and performing. However, you can teach. If that is the case, you will receive disability benefits in addition to your earnings as a music teacher.

Modified own occupation is a bit different. You will receive a disability benefit based on your inability to do your job as a musician. However, you can’t work in another job. So, if you work as a music teacher, you won’t receive disability benefits under the modified own occupation definition.

Finally, there is the stringent “any occupation” definition. This means, simply, if you can work in any gainful occupation (for which you are reasonably suited, considering your education, training, and experience), the carrier denies disability benefits. So, under this definition, you won’t receive a disability benefit because the insurance carrier says you can work as a music teacher.

(The Social Security Administration has a stringent any occupation definition).

Generally, I recommend staying away from this “any” occupation definition if you can help it.

The plans we work with contain the favorable own occupation definition for musicians. Moreover, you can align this definition to match some or all of your benefit period.

Waiting Period And Benefit Period

There are several definitions and provisions you’ll need to understand about disability insurance to make an informed decision.

There are several definitions and provisions you’ll need to understand about disability insurance to make an informed decision.

First is the elimination period, or waiting period. It is the period of time that elapses before disability benefits begin.

The waiting period starts on an approved claim.

For example, if you select a 90-day elimination period, your benefit eligibility begins on the 91st day of your disability. However, typically with carriers, you won’t receive your benefit until 30 days later (day 120 of disability or so). This means you need to have adequate savings to carry you and your family until benefits begin.

For long-term disability insurance, you can go as low as 30 days for a waiting period. (If you want short-term disability insurance, contact us. It may not be as worth it as you think.)

The second definition is the benefit period. The benefit period is the maximum time you receive your benefit for 1 claim. Disability benefit periods can be as low as 2 years and, with some carriers, as high as to age 67.

If the average disability lasts around 30 months, then a 5-year benefit period should be OK.

We will get into premiums later, but the corresponding costs are like a see-saw. A shorter elimination period usually costs more whereas a shorter benefit period costs less, all things being equal, of course.

Partial Disability / Residual Disability Benefits

Have you ever thought if you got hurt or sick, and could still work a little bit, but not full-time?

No, John.

Well, that situation happens a lot. You have an injury or illness that keeps you from working full-time. You can still work. However, you aren’t earning your full-time income.

This is still a disability. However, most plans wouldn’t pay a benefit.

What?

Let me explain further. Some plans will only pay a partial benefit after a total disability. See this excerpt.

But, what if your disability is a partial disability to begin with?

For example, let’s say a doctor diagnoses you with MS or carpal tunnel syndrome. Maybe you can only work a few days per week. But, your disability, currently, is not a total disability.

Then, the carrier won’t pay a benefit until your disability is considered a total one.

That could be months or years down the road.

So, your policy must contain robust partial disability benefits that pay a benefit even upon a partial disability.

Additionally, this rider provides monetary benefits when you return to work from a total disability.

I think you’ll agree with me that this rider is pretty important, right?

We at My Family Life Insurance offer these types of plans for musicians.

Guaranteed Insurability Options

Guaranteed insurability options are an important component of any disability insurance plan.

Essentially, this option (a rider) allows you to purchase more disability insurance in the future without going through health underwriting again. (We discuss underwriting next.)

All you need to do is show your income or salary increased, and then you have more disability insurance.

No underwriting is just how it sounds. You could be diagnosed with diabetes, have a bodily injury, be diagnosed with RA, or be charged with a misdemeanor and still purchase more disability insurance.

This is an important component many people overlook. You don’t need this option if you feel you are at the top of your pay scale.

The own-occupation, partial benefits, and guaranteed insurability options create a formidable plan.

But, let’s talk about disability insurance riders available to musicians.

Disability Insurance Riders For Musicians

Disability insurance riders allow you to customize your plan to your needs.

However, customization also increases the cost. It’s like purchasing a car. The “base” car might cost “XYZ”, but with customization, your car now costs “XYZABCD”.

Adding riders isn’t a bad thing. As I write in my disability insurance riders guide, you just want to make sure the riders are:

- Valuable

- Cost-effective

- Important to you

You can add optional riders at an additional cost to your policy to best fit your needs and budget. Some popular disability insurance rider options for musicians include:

Return of Premium Rider: This rider pays back all of your premiums should you never go on claim. If you do go on claim, the rider pays the net benefit (premiums less any benefits paid).

Retroactive Injury Benefit Rider: Pays benefits from the date of disability due to injury if disability occurs within 30 days of the injury and continues through the elimination period.

Activities of Daily Living Rider: This rider pays an additional benefit if you can’t perform two or more of the activities of daily living (dressing, toileting, eating, transferring (i.e. walking)) or cognitive impairment. These conditions are a catastrophic disability. Depending on your status as a musician, this rider may be beneficial to you.

Contact us to find out more.

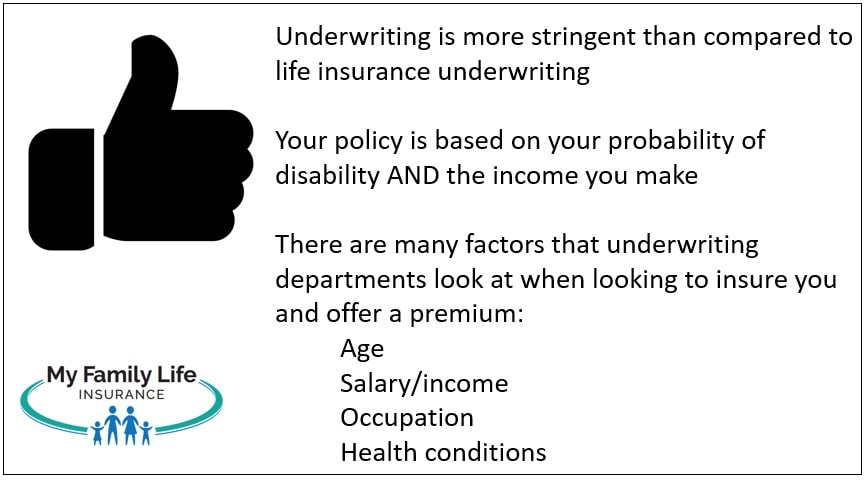

Disability Insurance Underwriting For Musicians

Disability insurance underwriting for musicians consists of 5 areas:

- your age

- income

- health conditions

- your musician occupation

- lifestyle situations

Your age and income are straightforward. The older you are, the more expensive the policy will be.

The higher your income, the higher the benefit, and the higher the premium. Don’t worry about the actual premium. As I illustrated earlier, you could have a serious, impact on your wealth without disability insurance. Nevertheless, we always strive to get you the lowest premium for your situation. I’ll discuss that more when we talk about premiums below, and how we are different than other agencies.

In case you were not aware, your income is your W-2 gross salary if you are an employee and your net income (after business expenses, but before taxes) if you are self-employed.

Self-employed individuals obtain their net income right off the appropriate tax return. Net income is the income remaining after business expenses, but before taxes. Many musicians we work with are self-employed. However, many symphonists are employed by the symphony or orchestra and receive a W-2.

So, if your W-2 salary is $80,000, carriers use that number for underwriting. Carriers also like to look at the last 2 years or 3 years and average out. So, having the last 2 or 3 years of salary on hand is handy for the application process.

Let’s talk about health conditions and your occupation next. Disability insurance underwriting is a little more complicated than, say, that of life insurance.

Why Health Conditions Matter In Underwriting

To get right to the point, usually, carriers generally exclude pre-existing health conditions from coverage. For example, if you have a pin in your right wrist from breakage 5 years ago, your policy excludes coverage on that right wrist.

If you had complications of pregnancy, then the carrier excludes any complications of future pregnancies.

If you are on anxiety medication, the carrier excludes coverage of any mental or emotional disorders.

That’s just how disability insurance works. Remember, the carrier is underwriting your potential disability. So, it will (generally) exclude any health complications or injuries you’ve had in the past.

If you have more serious health conditions, the carrier could place a rating on your policy. A rating is an extra premium the carrier charges for an increased disability risk. Moreover, the carrier may limit options such as limited waiting periods or reduced benefit periods.

Having an exclusion or a rating is not a reason to ignore a disability insurance policy. There are nearly endless ways for a disability to occur.

We discuss many scenarios about disability insurance underwriting. Additionally, we illustrate why it is NOT advantageous to decline a policy with any exclusions.

Your Occupation Matters

We discussed this earlier. This is an important aspect of disability insurance for musicians. So, all the disability insurance carriers classify occupations. In general, the carriers classify occupations from a 1 to a 5 or 6.

An occupation with a class 6 has the lowest occupational disability risk and class 1 has the highest. All things being equal, you’ll pay a higher premium if you are a class 1.

The classification for musicians depends on what you do. Here are various types of musicians with corresponding class:

- Symphonist / Orchestra – 3

- Rock Clubs / Concert Halls – contact us

- Churches / Funeral Home – 3 or 5

- Music Teacher – 3 or 5

What does this mean?

Again. all things being equal, carriers with a higher occupation classification save you money with lower monthly premiums.

Your Lifestyle Matters, Too

People don’t realize that your lifestyle matters, too. So, if you:

- Like going to the chiropractor a lot,

- Smoke marijuana, or

- Have many speeding tickets or car accidents,

Then these types of situations play a role in underwriting. For example, if you go to the chiropractor consistently, the carrier may exclude your back and spine from coverage, including wellness.

Please contact us for specific situations.

We addressed lifestyle situations in our disability insurance underwriting guide.

The Best Disability Insurance For Musicians

You are probably wondering who we like to work with. First, we work with many disability insurance carriers. So, we are sure we can find one that meets your needs and budget.

The carriers we like all contain:

- the own-occupation definition

- partial disability benefits

- guaranteed insurability options

and additional options as discussed. The disability insurers we like also have solid, value-added benefits like re-training programs.

I know other websites list popular carriers (per marketing rules, websites really shouldn’t list carriers unless prior, expressed agreement). We work with them, too, and even more.

For example, if you are a Christian, we also work with a disability insurance carrier dedicated to the Christian community.

Some plans may offer lump sum benefits if you are still totally disabled after 5 years (for example).

Moreover, as we said before, if you work part-time as a musician, we have disability insurance options.

Contact us if you would like to learn more. We are happy to chat with you.

Disability Insurance Cost For Musicians

The cost of disability insurance depends on everything we discussed in our underwriting section.

But, more often, the cost of disability will be around the cost of a cup of coffee or even the cost of lunch.

“In fact, the cost of disability insurance costs around 2 cents for every dollar you make.”

Here’s an example. Let’s use a 30-year-old female, self-employed musician. She earns $80,000 net income annually.

A 90-day waiting period, 5-year benefit period with a true own occupation definition, partial/residual disability benefits, and guaranteed insurability option costs about $122 per month for a $5,000 monthly benefit. That $122 per month insures 75% of her net income. It costs about $4.07 per day.

Does cost matter? Of course, it does! However, review my wealth example earlier. While every claim situation is different, I think you’ll agree with me that not having any disability insurance creates a potentially devastating situation. Just look at our wealth example earlier in the article. Having disability insurance protected $1,000,000 in wealth. Spending $122 per month on disability insurance (or whatever amount it is) certainly is worth it.

It makes sense to have some amount of disability insurance.

Should Musicians Obtain The Disability Insurance Plan Available For AFM Members?

AFM members have access to a disability insurance plan. What is the AFM? If you are a musician, it is the American Federation of Musicians. It is an association, and the disability insurance plan is an association plan.

We have written about disability insurance association plans before. Many associations offer them. Is the disability insurance plan through the AFM good for musicians? Is it good for you?

As always, we give transparent advice. You might be thinking, “Of course, John is going to talk about this. He wants my business.” Of course, I would love to work with you. However, as a CFP® Professional, I place your best interests first. Like anything I do, if I can help you and the plan is right for you, great. If not, I tell you what is better and point you in the right direction. It is that simple. The last thing I would do is put you in a plan that doesn’t work for you.

In my opinion, the plan through the AFM is neither good nor bad. Advantages exist; however, disadvantages exist, too. In my opinion, the disadvantages outweigh the advantages. The best way to obtain disability insurance is through a robust individual plan (or supplemented with your employer plan). Nevertheless, let’s discuss the disability insurance plan in more detail.

Advantages Of The AFM Plan

The Hartford underwrites the plan. They are a good carrier, and they underwrite many association plans. Association disability insurance policies tend to be “plain vanilla” so they can meet the needs of ALL association members. They work similarly to group disability insurance plans (through employers).

The AFM offers 2 plans for AFM Members. Here are some general advantages:

- premiums are usually cheaper – association disability insurance plans usually are cheaper compared to individual policies

- simple underwriting – Underwriting is usually simple with a simple application. However, The Hartford may still require a paramedical exam with blood and urine sample

- Add a spouse – you can add your spouse to the plan, if you wish

- Work requirement – only a minimum of 20 hours per week. As we stated before, we do work with disability insurance companies that will accept an application if you work as a part-time musician, 20 hours or more per week.

- Pre-existing conditions included (sometimes) – pre-existing conditions are included in coverage after a waiting period.

Let’s discuss the disadvantages next.

Disadvantages Of The AFM Plan

While many advantages exist with the AFM plan, so do disadvantages.

- own occupation coverage for 2 years only. After that, the plan has the any occupation

- coordinates with social security and any other benefits you receive (not good)

- limited partial disability benefits

- no guaranteed insurability option

- no other available benefits

What do you think? Only a 2-year own occupation definition? What happens if you develop a nerve pain in your hands that prevents you from correctly holding your instrument? Or, you are a singer who loses your voice? After 2 years, you are on the any occupation definition. If The Hartford deems you can do “any” other job at that point (likely, you can), your benefits stop.

Again, I urge you to review this plan if you are interested. However, I feel an individual plan is the best way to protect your income and wealth. Sure, you pay more, but better benefits and options exist with an individual plan.

Now You Know How Musicians Obtain The Best Disability Insurance

We hope now you have a solid idea why musicians need disability insurance, and how disability insurance protects musicians’ income and wealth.

We discussed plan options, underwriting, and costs.

Confused? Don’t feel that way. We’re here to help educate you and protect your income and future. Don’t know where to start? Use this disability insurance needs analysis worksheet.

Follow the instructions; it is rather easy to fill out (we at My Family Life Insurance try to make understanding insurance easy).

Next, feel free to reach out to us for our assistance or a quote. Or, use the form below.

We only work for you, your family, and your best interests only. We have helped many musicians secure the right disability insurance for their specific situation, giving them and their families peace of mind.

Learn More

Are you interested in learning more about the information in this article? Please fill out the form below, and we will email you additional information or give you a call. We always work in your best interest. By entering your information, you are providing your express consent that My Family Life Insurance may contact you via e-mails, SMS, phone calls, or prerecorded messages at any phone number(s) that you provide, even if the number is a wireless number or on any federal or state do-not-call list. Additionally, you understand that calls may be placed using automated technology, and that consent is not a requirement for purchase. Your information will NOT be sold and will remain private. However, you may opt out at any time. We respect your privacy first and foremost. By contacting us, you agree to receive text messages from our number (800) 645-9841. If you no longer wish to receive text messages, you may opt out at any time by replying "STOP".