Top 5 Devastating Mistakes People Make With Disability Insurance | How To Avoid These Mistakes And Make The Right Decision On This Important Insurance

Updated: April 12, 2024 at 9:39 am

Selecting the right disability insurance policy is no laughing matter. We all need the proper coverage. Yet, when we review policies from non-clients (people looking for our help), many of them have made some devastating disability insurance mistakes.

These mistakes aren’t in the basic realm of the “I have the wrong benefit coverage” mistake. (Purchasing an additional policy or exercising a purchase option fixes these mistakes.)

These are serious mistakes that were made for one reason or another. These mistakes will affect your disability insurance claim coverage, likely, just when you need the coverage the most.

These are devastating disability insurance mistakes that you generally can’t recover from unless you take action now.

No table of contents for this article. We will jump right into the mistakes in no particular order.

Devastating Disability Insurance Mistakes #1 – Shopping Around On Price

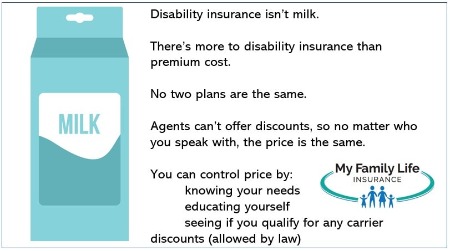

Purchasing disability insurance, or any insurance, is not like shopping for a car. You can’t stop at dealer XYZ and see what the price of a car is, and then go to dealer ABC and see if you can get the car for $5,000 less. Purchasing disability insurance doesn’t work that way.

Premiums are set by the states and the carriers. Agents have no bearing or influence on them. They can’t discount, and agent incentives to do so are against the law.

When you shop around, you are treating disability insurance as a commodity like bread, gas, and milk. You erroneously equate the value of disability insurance to the premium cost only. In our opinion, the premium cost is actually a third of the value, at most.

When you shop around, you are treating disability insurance as a commodity like bread, gas, and milk. You erroneously equate the value of disability insurance to the premium cost only. In our opinion, the premium cost is actually a third of the value, at most.

The other two-thirds are the benefit value within the policy. No 2 policies are the same. Apples-to-apples comparisons are futile. Here at My Family Life Insurance, we compare carrier quotes, but we also note that there are significant differences among the carriers.

We base our recommendations on your needs and situation, not necessarily on cost. Cost is secondary. You want your policy to perform when you need it the most (i.e. when you are hurt or sick and can’t work). That makes the benefit value of primary importance.

How can shopping on costs only prove disastrous? Here is an example.

Example Of Making A Decision On Cost Only

For example, there are many disability insurance riders available with all carriers. I’ve seen competitor quotes where the agent throws all riders into the quote. Doing so creates a discussion about potential benefit value, but it also creates sticker shock. People just freeze when they see that. I saw one quote for a dental hygienist that was $800 per month. It didn’t match her income or needs. Maybe it was right for a CEO; however, not for a dental hygienist.

Conversely, I’ve seen quotes with nothing…no value…and thereby cheap. The applicant inadvertently thinks the policy is better because it is cheaper. Then applies. The value of the policy (likely low) won’t be known until the insured files a claim.

Honestly, the $800 per month may have been the right policy, but it was the wrong approach.

What do you do to avoid this situation? We discuss that next.

How To Avoid Mistake #1

There are 3 ways to avoid this disability insurance mistake. You can:

- Research all the options available and figure it out,

- Contact a reputable agent, and/or

- Some combination of #1 and #2

It’s important that you do some research and education. However, the key to avoiding mistake #1 is to find a dedicated and honest disability insurance agent who works in your best interests only. I am really not tooting my horn here.

This agent should have access to many carriers to match your specific needs to the right disability insurance policy. Let the agent do the shopping for you. If he or she has access to over 10 disability insurance carriers, there will be one carrier policy that meets your situation and budget.

Knowledgeable, honest disability insurance agents are worth their weight in gold. Their value is priceless. I am sure you can agree that when you find someone who works only in your best interests, you don’t want to lose that person. You value his or her knowledge. Great agents continue to serve long after the application. They help you during the underwriting process and provide service long after the transaction.

Another Example Of Shopping On Costs

Why is shopping around yourself a devastating disability insurance mistake? Because you are only focused on price and not the overall value. Most times, you will select the lowest-cost option, thinking it is the right one for you. This is a potential, long-term, expensive, and damaging solution. How does this happen? Here is a real situation:

You are a dental hygienist and find a policy for yourself. It is cheap, through your national association. (Disability insurance plans through associations are usually cheap. See our article on disability insurance association plans on why.)

You have problems with your right wrist. Your doctor diagnoses you with carpal tunnel. He says, right now, you can still work, but just not full-time. You are limited to working two days per week.

Knowing you have a disability insurance policy, you file a claim for partial benefits. You are disabled, right?

However, the plan does not pay. See the snapshot right out of the association’s plan. You did not meet the carrier’s definition of partial disability which requires a total disability first. You wonder how you are going to fill the income gap when you have limited use of your hands. (And, you are angry, too.)

As you can see, by focusing on cost only, you just made a devastating, long-term expensive mistake.

Devastating Disability Insurance Mistakes #2 – Not Accepting The Policy

When you apply for a disability insurance policy, there is no guarantee you will receive the premium rate quoted or benefits. In fact, nearly all carriers adjust the final offer one way or another. This isn’t a bad thing.

To obtain the lowest cost policy for your given situation, you need to be honest and disclose any and all health conditions or lifestyle risks. Then, agents can design an accurate quote (but still an estimate).

Disability insurance underwriting is stringent. Generally speaking, you also need to go through medical underwriting which includes a paramedical exam, height and weight check, blood/urine sample, and potentially additional questions. Many carriers offer a non-medical underwriting process for benefits under a certain monthly amount.

If you get a higher premium than originally quoted, such as a rating, it is important to remember who the recipient of this disability insurance money is. The recipient is not only you, but your wife, husband, children, or another loved one. Why would you sacrifice their financial security by not accepting the policy? You can always accept the policy and then work with your agent (or another one) to work on improving the policy.

important to remember who the recipient of this disability insurance money is. The recipient is not only you, but your wife, husband, children, or another loved one. Why would you sacrifice their financial security by not accepting the policy? You can always accept the policy and then work with your agent (or another one) to work on improving the policy.

Most times, we have found, people decline the policy, then procrastination sets in. Months and years might go by. Suddenly, they need disability insurance, but they have the inability to purchase a policy because they just had open heart surgery or some other significant health condition. They jeopardized their family’s financial security.

A premium increase isn’t that much more when you really analyze it. For example, an additional $30 per month in premium might seem a lot, but it is only $1.00 per day. We can find $1.00 per day, right?

How To Avoid Mistake #2

Most of us have health conditions that make disability insurance premiums higher compared to the premiums of a healthy person. This is where a qualified agent helps. He or she can review your situation and then match a policy at the lowest cost possible.

Let’s say you have type 2 diabetes. If you tell us the front end, we can give a more accurate quote than if you don’t.

Let me guess…you’ll just invest the money you would have paid, right? As the saying goes, if I had a nickel every time someone told that to me, I would be a very rich man. I am honest about that.

Not taking the policy is a huge disability insurance mistake. Here’s a true story.

“Steve” runs a successful massage therapy studio. He told me he has anxiety, but upon underwriting and delving into his doctor’s records, he is actually bipolar and has borderline schizophrenia.

Those mental disorders are very hard to cover, but the carrier approved him for a modified policy. The policy excluded these conditions, however.

Steve became angry when I told him about the modified policy. He declined it. The policy still covered him in case anything else was to happen, such as an illness like cancer or an accident.

And something did. Steve was an avid bicyclist. A year later, I learned he injured his head and other body parts when a car struck him. He is lucky to have lived.

Steve lost his career, though, and money became tight. He did contact me about revisiting the disability insurance policy (how I learned about his situation). Unfortunately, due to these events, he is not insurable.

So, just take the policy. There are more important people in your life connected to that policy.

Devastating Disability Insurance Mistakes #3 – You Are An Expert

We are all experts at something. If you are a hair stylist, you know how to style and cut hair the right way for your client. If you are a mechanic, you have a skill set unmatched by many people. Same if you are a physician, dentist, veterinarian assistant, teacher, and on and on.

Disability insurance agents are experts, too. Sure, determining your need is not rocket science. We put together an easy, and accurate, disability insurance needs analysis for you. What is difficult is finding the right fit for you and your family’s needs.

This is something you don’t want to do alone. Would you try to fly an airplane without experience? Of course not.

This is something you don’t want to do alone. Would you try to fly an airplane without experience? Of course not.

There is a platform currently where you can apply for disability insurance on your own with no agent assistance. It’s not a good idea.

Why? Because there are so many moving parts with disability insurance. From underwriting to riders, there are so many choices. Unless you work every day in disability insurance and have the skill set, do you know what to do?

The mistakes we have seen are from people who simply purchased a policy themselves and did not understand how disability insurance works.

True story. We have a client who went through the online process herself. She almost applied with the same carrier we quoted her. That is right. The same carrier.

Our quote was higher. She stopped her application (thankfully) and ask me why my quote was higher. The reason was I put on the important residual disability rider whereas she did not. If she went through with her application and then faced a partial disability, she would not have received a benefit.

Some Agents Just Don’t Know Disability Insurance

Moreover, many agents think they know disability insurance, but they don’t. I see this often, especially with more and more carriers making it easier for agents to sell.

This situation happened to my family. A personal story: my wife needed disability insurance. A co-worker referred an agent to us. My wife had a temporary condition during the pregnancy of our first child which at that point, occurred two or three years before. The condition wasn’t disabling by any means. She was working just fine when we met the agent. We even had another child at that point with no issues. We submitted the policy.

My wife was later declined due to the condition. It made no sense. And, the agent was nowhere to be found to help us through it. We did finally obtain disability insurance, sans the agent. (That was actually when I delved into the disability insurance area and have been helping individuals and families ever since.)

There are insurances myself I don’t delve into. The reason is that I feel I am not an expert in these insurances. For example, while I understand health insurance, recommending and advising plans is something I won’t do. I refer that to an expert team I work with.

How To Avoid Mistake #3

You don’t want to tackle disability insurance alone. Like the previous mistakes so far, disability insurance selection requires the assistance of a knowledgeable and reputable agent. Sure, you can try to tackle it on your own, but the consequences might be severe. You won’t know until you file a claim.

Moreover, many agents or advisors think they know disability insurance, but they don’t. There is more to the disability insurance equation than cost and coverage determination. Good disability insurance agents know the underwriting process and benefits of each carrier. They educate you on your needs and your family’s needs, and that their recommended carrier is the right one for you. They also talk about your case to the carrier. Good agents should do that to avoid what my wife went through.

They should also talk about how and when your policy will pay. Wouldn’t you like to know that BEFORE you purchase a policy?

How to avoid mistake #3? Simply, find an honest and knowledgeable disability insurance agent.

Devastating Disability Insurance Mistakes #4 – Your Employer Offers It So You Don’t Want Any

Many companies offer disability insurance for their employees. It is a nice benefit.

Most times, your company pays for it all or some part of it.

Yes, That is me. I am all set, John.

Are you? Are you sure about that? Not getting additional disability insurance is one of the major mistakes people make.

Three major problems I see with group employer disability insurance:

- Plain vanilla structure

- Benefits can be capped

- Benefits are taxable

Most group employer disability insurance is plain vanilla. It has to be in order to meet the needs of all employees.

So, the plan you have with your employer may meet your needs, but not Sally, 2 cubicles down from you.

Group / employer disability insurance usually:

- Limits own occupation definition

- Has no or limited riders

- Increase premiums every year

- Automatically approves

In order to keep costs down, carriers may cap the monthly benefit. For example, it is common for carriers to offer something like this:

“cover up to 60% of your gross salary not to exceed $3,000 per month”

What if you make $100,000? That typically yields a $5,000 monthly benefit on the private insurance market. If your company’s plan only offers $3,000, you probably are underinsured.

Additionally, the benefit is taxable. It’s taxable because the carrier pays or you pay for it pre-tax.

You’ll have to record your benefit amount on your taxes. That means, ultimately, your monthly benefit might be 20% to 30% less than what you receive when you account for taxes.

Can your family live off that?

No. What can I do?

How To Avoid Mistake #4

To avoid mistake #4, you want to purchase a supplemental disability insurance plan.

plan.

It is an individual, private plan. The carrier stacks its benefit on top of the group employer plan.

There are 2 advantages here.

One benefit is that your total disability benefit matches your total earned income. So, if you make a claim, you will have more money coming in to pay for things (and, some money to offset any tax impact).

Another benefit here is cost. An example will make this clear.

Let’s use the example numbers above. You are a 35-year-old female and make $100,000 as an accountant. You accept your employer’s disability plan which has a maximum monthly disability benefit of $3,000.

However, you are underinsured, so you seek a supplemental plan.

One carrier offers an additional $3,670. So, if you file a claim, you will receive $6,670 per month ($3,000 from your group plan and $3,670 from your private plan).

The private, individual plan costs around $92 per month. That is just over $3.00 per day.

Certainly, with everything you spend your money on, you can find $3.00 per day to protect 80% of your salary, right?

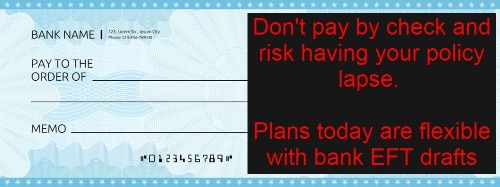

Devastating Disability Insurance Mistakes #5 – You Pay By Check

How often do you write checks nowadays?

Probably rarely.

With automatic bank draft, you don’t have to worry about missing a payment.

As long as you pay the premium, you will have disability insurance.

That means, no lapses. That means you will have coverage if you need to make a claim.

It means coverage is there when you need it the most.

Paying by check is one of the major mistakes I see people make with disability insurance.

With such important insurance like disability insurance, why would want to pay with a check, potentially forget to pay, and then find out you don’t have coverage when you need the policy the most?

Well, John. I want more control over my money!

Everyone does. Let me tell you a story.

We had a client years ago who would pay by check. While she dutifully paid every quarter, sometimes she would be late on a payment.

Carriers always notify us (and you, too). We ultimately would get ahold of her. She got busy or something and forget to pay. But, she would pay and get back on track.

Then one day she missed a payment. We reached out to her. Crickets. We kept doing so. Nothing.

Her policy lapsed.

We heard from her when she contacted the carrier to make a claim. Unfortunately, time passed way too long.

How To Avoid Mistake #5

Ultimately, the ability to pay rests on the insured/policy owner. While carriers and agents notify you, it ultimately isn’t their responsibility if you miss a payment.

The best way to avoid this mistake is simply to put the payment on automatic draft.

A disability insurance payment isn’t the electric bill.

If you don’t pay, worst case, the electric company shuts off your electricity. Then you would have to back pay your bills and likely a fee.

But, in doing so, your electricity is back on.

Not with disability insurance (or with other types of insurance as well). After the grace period, usually 31 days, then the carrier cancels the policy.

Once it’s gone, it’s gone. Unless you reapply and pass the underwriting process again.

While many carriers are great to work with on the claims side, when it comes to reinstating a lapsed policy, many will require underwriting again. They won’t budge.

Additionally, if you are sick or hurt and have a lapsed policy, then you are simply out of luck.

So, just put your payment on automatic draft to ensure the coverage is there when you need it the most.

Now You Know The 5 Devastating Disability Insurance Mistakes People Make & How To Avoid Them

Have you made any of these devastating disability insurance mistakes?

- Shopping around

- Being an expert

- Not accepting the policy

- Thinking your employer policy is enough

- Paying by check

If so, there is still time to fix them.

Don’t find out you made mistakes until you make a claim.

Do you know where or how to begin? Contact us or use the form below.

We have helped many professionals fix their disability insurance mistakes.

Are you worried about contacting us and then receiving 1,000 phone calls each day? We aren’t like that. Contact us or use the form below. There’s no risk of contacting us. If we can’t help you, we will point you in the right direction as best we can. You can always reach back out to us if your needs change.

We only work with your best interests and are happy to help you and your family.

Learn More

Are you interested in learning more about the information in this article? Please fill out the form below, and we will email you additional information or give you a call. We always work in your best interest. By entering your information, you are providing your express consent that My Family Life Insurance may contact you via e-mails, SMS, phone calls, or prerecorded messages at any phone number(s) that you provide, even if the number is a wireless number or on any federal or state do-not-call list. Additionally, you understand that calls may be placed using automated technology, and that consent is not a requirement for purchase. Your information will NOT be sold and will remain private. However, you may opt out at any time. We respect your privacy first and foremost. By contacting us, you agree to receive text messages from our number (800) 645-9841. If you no longer wish to receive text messages, you may opt out at any time by replying "STOP".