How To Avoid This Life Insurance Mistake During Divorce | Your Guide To Understanding How Life Insurance Works During And After Divorce

Updated: April 12, 2024 at 9:38 am

Divorce proceedings can be tricky and complicated. Lawyers are involved and assets are split. Emotions are high. Divorce proceedings can tie up life insurance policies as well. If you aren’t careful, however, you could make a major mistake with your life insurance policy during your divorce proceedings.

Divorce proceedings can be tricky and complicated. Lawyers are involved and assets are split. Emotions are high. Divorce proceedings can tie up life insurance policies as well. If you aren’t careful, however, you could make a major mistake with your life insurance policy during your divorce proceedings.

Trust me. You don’t want that to happen.

In this article, we discuss how life insurance operates during, and after, a divorce, with specific details about a major mistake some people make with their current life insurance policy during divorce proceedings. I even illustrate a real divorce situation with a former client of mine who unfortunately made this mistake.

This is your guide about how life insurance works during and after a divorce, with emphasis on a major mistake some people make during the divorce proceedings.

Here is what we will discuss:

- What Happens With Life Insurance During Divorce

- Why Insurable Interest Matters

- The Major Mistake People Make With Life Insurance During Divorce

- Life Insurance After Divorce

- Life Insurance For Ex-Husband

- Life Insurance To Cover Alimony Payments

- Life Insurance For Child Support

- Life Insurance For A High-Risk Ex-Spouse

- FAQs About Life Insurance And Divorce

- How We Can Help

Let’s jump in and discuss what happens with assets, including life insurance, during a divorce. (Please note: I am not a lawyer and not dispensing legal advice, information, or recommendations. For questions on your specific situation, please consult a reputable divorce lawyer in your state. Your state laws govern divorce laws.)

What Happens With Life Insurance During Divorce

The divorce process starts with an official complaint followed by pre-trial hearings and motions. Both parties disclose financial information during the discovery phase. Assets include life insurance. During this phase, parties discover, negotiate, and split the assets and marital property.

Usually, per the final divorce agreement and divorce decree, any current life insurance policies can be retitled with the ex-spouse as the new beneficiary designation, policy owner, or both. Changing the beneficiary designation status is extremely important. This is important because ex-spouses no longer possess insurable interest. We will discuss this important doctrine next.

This retitling usually happens when the courts require child support payments, alimony, or other financial obligations. For example, if the spouses have minor children together, a policy owner can retitle a current life insurance policy with the former spouse (who has primary child custody) as the named beneficiary.

This retitling usually happens when the courts require child support payments, alimony, or other financial obligations. For example, if the spouses have minor children together, a policy owner can retitle a current life insurance policy with the former spouse (who has primary child custody) as the named beneficiary.

The divorce decree and separation agreement govern the retitling (I’ll explain what I mean by that in the next section). In other words, you can present a copy of the divorce decree (bonafide court order) to the life insurance company. It will make the proper beneficiary designation change or policy owner in the name of the former spouse. You can add contingent beneficiaries if you wish.

However, sometimes life insurance policies fall through the cracks. This can happen with term life insurance especially because term life insurance policies do not contain cash value. Technically, it contains no asset value.

So, what, John? Why can’t my ex-spouse remain as the beneficiary?

He or she can. The issue is whether beneficiaries remain as a married spouse as insurable interest no longer exists.

(Note: if the divorce decree requires a new policy, ex-spouses can apply for the new life insurance policy the same way they would if they were still married.)

Insurable Interest Matters

Insurable interest is an important doctrine with life insurance. It basically states that the policy owner or beneficiary of a life insurance policy must have a valid and ascertainable stake in the continued existence of the insured person.

For example, Jim and Mary are happily married. Jim takes out a life insurance policy on his life with Mary as the primary beneficiary. If Jim unexpectedly passes away, Mary will receive the death benefit. Mary will use the death benefit amount for her needs and lifestyle.

That makes sense, right? It is very common for husbands and wives to have life insurance for the benefit of the other.

Let’s change the situation. Jim and Mary are now divorced. Without additional information, does it make sense that Mary is still the beneficiary of the life insurance policy?

No.

That is the insurable interest doctrine. A special relationship must exist among the insured, policy owner, and beneficiary. In this case, that relationship is love.

I think you’ll agree with me that love doesn’t necessarily exist in a divorce situation. Unless demanded by court order (i.e. divorce decree, divorce settlement, or some other legal arrangement), why would Jim want to potentially benefit his ex-wife upon his death?

26 States Revoke A Divorced Spouse Beneficiary

That is why, currently, 26 states automatically revoke the spouse (if divorced) as the primary beneficiary. You can see states in the picture.

These states say, your intention likely isn’t to enrich your former spouse. The fact that your former spouse remains the primary beneficiary is likely due to neglect and forgetfulness rather than by choice. So, these states simply automatically reject your former spouse as the primary beneficiary. Any death benefit money then passes to the contingent beneficiaries. If no contingent beneficiary exists, then the death benefit amount goes to the owner-insured’s estate.

Let’s go back to the divorce example and assume Mary needed that death benefit money because she has a rare illness that prevented her from gainful employment. She needs that money for financial support. What would happen then? Well, if she lives in a state that automatically revokes a divorced spouse, then she would likely not see any death benefit money. That money would go to Jim’s estate and then passed through probate.

What should have Mary done?

The Major Mistake People Make With Life Insurance And Divorce

That is the mistake Mary made. Inadvertent? Probably. As the beneficiary (in this example), she can’t make changes to the life insurance policy. Per state law, the carrier must revoke her as beneficiary. (Because she is no longer his wife. She is his ex-wife.)

However, she could have consulted her divorce attorney who could have consulted Jim’s lawyer. They probably could have modified the court order (divorce decree) through a petition. Additionally, they could have requested a beneficiary change from the life insurance carrier. Again, I am not a lawyer. You will want to consult an attorney in your state for specific questions.

However, she could have consulted her divorce attorney who could have consulted Jim’s lawyer. They probably could have modified the court order (divorce decree) through a petition. Additionally, they could have requested a beneficiary change from the life insurance carrier. Again, I am not a lawyer. You will want to consult an attorney in your state for specific questions.

Additionally, forgetfulness or not, this example underscores the importance of bringing all financial instruments to the table. Divorcing couples need to know this. The onus is on them.

The right steps would have been to:

- consult a lawyer,

- contact the life insurance carrier, and

- contact the ex-spouse

- change the beneficiary designation to an ex-spouse status

Do you think this situation won’t happen? It does, and it happened to a client of mine.

A Real Example Of This Happening

Long ago, when I first entered this business, I worked for a captive insurance company as a new insurance agent. Like many captive carriers, they had a bunch of “orphans” assigned to me. An orphan is a person who purchased an insurance policy with no current assigned agent. The selling agent left the carrier, leaving the policyholder without an assigned agent, which was now me.

I contacted this woman who was on my orphan list and introduced myself. I told her I was going to be in her area on “x” day and asked if it would be OK if I stopped by her residence and introduced myself. She said that it was OK.

We met and reviewed her life insurance policies. She then mentioned to me that one of the policies was in her ex-husband’s name (as owner) with her as the beneficiary. I asked her if her divorce decree included this life insurance policy as part of the divorce settlement. She said she was not sure. I recommended that she call the carrier and consult her decree. If she is still on the policy as a spouse/wife beneficiary, then she contacts her divorce lawyer as well as her husband to officially change her beneficiary to ex-spouse status. If I recall, she had children teenager age (like 14 and 16).

Unfortunately, her husband (she told me) fell on hard times, developed a serious drug addiction, and was homeless. She was paying the premiums on the policy, with hopes that if he passed away, she would receive the death benefit money. She said if she contacted him, he would likely cancel the policy (because he was the owner) out of spite.

Carrier Follows State Law

I explained the insurable interest doctrine in layman’s terms, as best I could. I told her that marriage is the concrete that allows a spouse to be owner and/or beneficiary. If divorce cracks this concrete, insurable interest (based on love) does not exist. She questioned what she was hearing from me. In other words, she didn’t believe me and thought because she was still the beneficiary, she would still receive the death benefit money if her husband died. I told her I wasn’t sure. However, I continued to recommend she speak to her attorney to make sure her beneficiary designation as “wife/spouse” remained legitimate in the state’s purview. If not, then take the steps to change it to official “ex-spouse” status. Unbeknownst to me at the time, I did not realize Massachusetts automatically revoked beneficiary designations for a divorced spouse.

Her husband passed away about 2 months later. When she filed the death claim, she was in shock that the life insurance carrier withheld the death benefit. The claim department told me that the claim was now in state court, all because she was listed as wife/spouse beneficiary.

Death Benefit Proceeds Went To Probate, Likely

I do not know the outcome of this real situation, as she never contacted me again. However, I’m sure the death benefit proceeds were included in probate. If you read my article about life insurance and probate, then you know probate law can be cold and heartless. Not necessarily in a bad way.

I can only guess that the death benefit proceeds went to his side of the family, with the possibility of some of the death benefit money going to his ex-wife (my client) because of the minor children.

However, he was unemployed, was living on the streets, and did not fulfill child support obligations. One could make the argument that she self-supported herself and can do so without the death benefit proceeds.

You can see what a tangled web this mistake weaved.

Life Insurance After Divorce (Per Divorce Decree)

We just reviewed this beneficiary designation mistake. However, what happens if, during the divorce proceedings per the divorce decree, you need a new life insurance policy?

This happens when:

- an ex is receiving alimony income

- minor children are present

- the ex-spouse may have a health condition or other financial obligation

Thankfully, the process is simple.

Life insurance through this process is also known as court-ordered life insurance. The courts order it through the divorce decree.

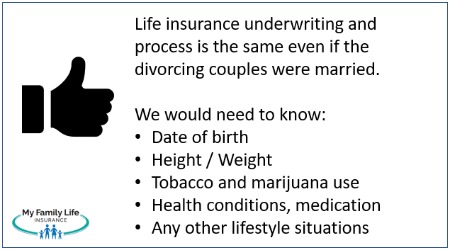

If you want to work with us, we would need a copy of the divorce decree. The decree will outline the life insurance coverage, type of policy, life insurance beneficiary, who is the paying spouse, etc.

We then will need health and lifestyle information on the insured ex-spouse including:

- date of birth

- height/weight

- any health conditions or lifestyle situations such as reckless driving or substance abuse situations

- tobacco and marijuana use situation

Depending on the ex-spouse’s situation, the ex-spouse may go through an accelerated underwriting process or a fully underwritten process.

We have helped many divorcing couples obtain life insurance on their ex-spouse, per a divorce decree. We have even helped people declined by traditional life insurance carriers obtain life insurance coverage. Please contact us if you would like to learn more.

Life Insurance For An Ex-Husband

I receive many inquiries from women about getting life insurance for their ex-husbands. Yes, you can get life insurance on your ex-husband provided you show insurable interest.

We discussed the important insurable interest principle earlier in the article.

Generally speaking, you can show insurable interest in the following situations in a divorce:

- you are receiving alimony from your ex-husband

- he is responsible for child support

- he has other financial obligations to you (like a joint mortgage)

These are valid situations where an insurable interest exists. If he passes away unexpectedly, the life insurance payout will provide the remaining funds to fulfill his obligations.

You would make sure you are the designated beneficiary. I also recommend that you are also the owner of the policy. That way, only you can cancel or modify the policy.

If you want to work with us, your ex-husband would have to provide underwriting information to us including health, lifestyle, etc. He would sign the life insurance application as the insured. You would sign the application as the policy owner (recommended). We do this over the phone. It is an easy process. Note: you both don’t need to be on the phone with us at the same time.

Contact us if you have any questions.

If your husband has serious health or lifestyle situations, we can probably get him life insurance. See our section on high-risk situations below.

Life Insurance For Alimony Payments

We have helped many divorcing couples establish life insurance for alimony payments. If the payor of the alimony unexpectedly passes away, the life insurance pays the death benefit to the ex-spouse. Again, the divorce decree usually establishes this requirement.

I hear from many alimony payors that a traditional term life policy doesn’t work. They have a valid concern. They don’t want to enrich their ex-spouse anything beyond what the divorce settlement states. For example, let’s revisit our divorcing couple from the beginning of the article. Let’s say the courts require Jim to pay Mary $2,000 per month of alimony until she reaches age 65. They are both 41 years old.

It would be incorrect to establish a 25-year term for a $600,000 death benefit (12 months X $2,000 X 25 years). If Jim dies at age 58, Mary just inherited $600,000 when, per the divorce decree, she should have received $192,000 (8 years until age 65 X $2,000 X 12 months).

A decreasing term life insurance policy works extremely well in this situation. It will pay the remaining monthly benefit to the beneficiary until the term ends. In our example, if Jim had a decreasing term policy, the policy would have paid Mary $2,000 per month until age 65.

Cost is a major benefit of a decreasing term policy. It can be 20% to 40% less expensive than a comparable term life policy.

Contact us if you would like to learn more.

Life Insurance For Child Support

You can set up life insurance for child support the same way. The noncustodial parent is the insured. The custodial parent is the owner (preferred way) and beneficiary. If the noncustodial parent is the policy owner, I recommend working with your attorney to make sure the policy can’t be modified (i.e. canceled) without your consent.

Decreasing term life insurance works well here, too. We would set up the life insurance to expire whenever the youngest child turns the age of majority or what is stipulated in the divorce decree.

Contact us if you have any questions.

Life Insurance For An Ex-Spouse With A High-Risk Situation

John, I’ve tried to get life insurance for my ex-husband. However, he takes suboxone. No carrier will insure him.

I’ve heard this situation before. We can get him life insurance.

If your ex-spouse has a serious health condition or lifestyle situation, we can get him or her insured (likely).

Just provide a copy of your divorce decree or divorce settlement outlining the specific requirements for the life insurance. We will then consult our alternative life insurance carriers and provide you with a quote.

We have helped ex-spouses get insured in the following situations (including, but not limited to):

- drug abuse / substance abuse situations

- hazard occupations or hobbies like skydiving

- overweight issues

- severe diabetes

- felony history

- heart issues / recent heart attacks

- and more

I am happy to say we have helped ex-spouses obtain life insurance when they thought they were otherwise uninsurable. Just contact us. Let us know your situation, and we can see if we can help.

Frequently Asked Questions About Life Insurance And Divorce

We answer some frequently asked questions about life insurance and divorce.

What Happens to Existing Life Insurance Policies During a Divorce?

That depends on the situation and the divorce decree. If the courts require alimony, child support, or other type of obligation then the existing life insurance can be modified to include the ex-spouse as the beneficiary. We discussed how some existing policies can fall through the cracks. If this happens, the outcome could be detrimental to the beneficiary.

Can I Change the Beneficiary Designation on my Life Insurance Policy After Divorce?

Yes. You would submit a change of beneficiary form to the current life insurance carrier and request the change. Since you are switching from a spousal beneficiary designation to an ex-spouse beneficiary designation, the carrier may request a copy of the divorce decree.

Are There Tax Implications Associated with Life Insurance in a Divorce?

No. The tax advantages of life insurance remain intact even after a divorce.

What Type of Policy Is Best During A Divorce?

That depends on your situation. However, term life insurance, specifically decreasing term life insurance, works well in child support, alimony, and other obligation situations.

If you are obligated to pay for your spouse’s funeral or final expenses, then a permanent life insurance policy like whole life insurance works well.

Again, the type of life insurance policy depends on the situation. We can help.

What Happens to My Group Life Insurance Policy During A Divorce?

Group life insurance policies do not have the same state revocation laws as individual policies do. Group policies follow ERISA laws. The current person named as the primary beneficiary would receive the death benefit should the insured pass away.

Be aware that the divorce decree may require the beneficiary designation to remain in your ex-spouse’s name.

Should I Review and Update My Life Insurance Coverage After Divorce?

Yes. It is good practice to always review your life insurance beneficiary designations annually.

Can a Former Spouse Be Forced to Maintain a Life Insurance Policy for the Benefit of the Other Party or Children?

Yes. If the divorce decree states so, then a spouse could be forced to maintain a life insurance policy. The former spouse will have to maintain that policy until the obligation has been fulfilled.

Now You Know How Life Insurance Works During And After A Divorce, And The Mistake People Can Make

We hope you learned how life insurance works during a divorce and a major mistake some people make with the life insurance / divorce process.

Are you going through a divorce and need life insurance assistance? Contact us or use the form below.

As we stated earlier, we have helped many divorcing couples obtain the life insurance they need, even in situations where they were declined before.

We only work in your best interests and will find the policy you need to satisfy your divorce obligations. If we can’t, we will point you in the right direction as best we can and part as friends. You can always reach back out to us if your needs change.

Learn More

Are you interested in learning more about the information in this article? Please fill out the form below, and we will email you additional information or give you a call. We always work in your best interest. By entering your information, you are providing your express consent that My Family Life Insurance may contact you via e-mails, SMS, phone calls, or prerecorded messages at any phone number(s) that you provide, even if the number is a wireless number or on any federal or state do-not-call list. Additionally, you understand that calls may be placed using automated technology, and that consent is not a requirement for purchase. Your information will NOT be sold and will remain private. However, you may opt out at any time. We respect your privacy first and foremost. By contacting us, you agree to receive text messages from our number (800) 645-9841. If you no longer wish to receive text messages, you may opt out at any time by replying "STOP".