Here Are 4 Life Insurance Options If You Have Bipolar Disorder | We Discuss The Options And How You Can Get Approved!

Updated: April 12, 2024 at 9:39 am

In this article, I will tell you how people with bipolar disorder, or manic depression, can obtain life insurance.

depression, can obtain life insurance.

If you have bipolar disorder, you may have thought that life insurance was unavailable or out of reach.

That is simply not true. You can get approved for life insurance, in some cases as early as a couple of days.

How?

You just need to know which carriers underwrite your condition the right way. There could be many options.

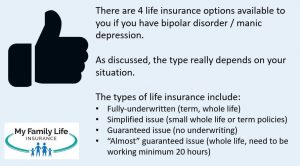

The way I see it, if you have bipolar disorder, you have 4 life insurance options available to you. We’ve helped many people obtain life insurance, and I am sure we can help you, too.

Here’s what we will talk about.

- Full Underwriting Process

- Simplified Underwriting Process

- The 4 Life Insurance Options

- Final Thoughts

Let’s jump right in and discuss how carriers underwrite your condition. This is the most important step in the entire life insurance application process

How Life Insurance Carriers Fully Underwrite Bipolar Disorder – If You Want More Than $100,000 Of Life Insurance

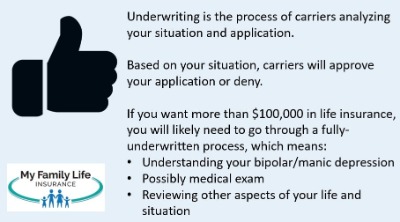

Underwriting is the process of reviewing your situation and application and then making you an offer based on your situation.

Like most situations, how carriers underwrite bipolar disorder depends on your situation. Really, no two applications are alike.

First, let me say that we can likely get you some type of life insurance if you have bipolar disorder or manic depression.

But, as we said, the types and death benefit size available really depends on your situation.

Moreover, in most cases, carriers will offer an approval – which is great – with a table rating.

A rating, honestly, is no big deal. We will discuss that more.

A rating, honestly, is no big deal. We will discuss that more.

Carriers not only want to know the severity of your condition, but also want to know other things like your height/weight, tobacco or drug use, etc.

They will also verify your information through driving records, prescription drug database, the MIB, among other databases. They will also require a paramedical exam, blood draw, and urine sample, too.

Next, we will give you a general idea of how carriers underwrite your health condition. We will also give you real success stories where we have helped people with varying degrees of bipolar disorder obtain life insurance.

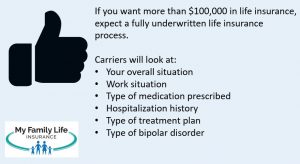

The following is if you want $100,000 or more of life insurance. If you have bipolar disorder and want $100,000 or more in life insurance, expect a fully underwritten application process. Carriers will want your doctor records among other information. (Simplified underwriting does exist, and we will discuss simplified underwriting later in the article.)

If You Work

I’ve said this time and time again…if you work, for earned income and not on SSDI disability, that proves a lot to insurance carriers. It shows you can earn an income and not let your health condition affect your everyday life. Moreover, working shows you can have conversations and relationships with people. It is a normal life activity. I know this sounds funny, but this is an important aspect.

Certainly, other factors might alter the underwriting outcome (as I will discuss next). However, earning an income in a full-time capacity demonstrates you can manage your condition while maintaining employment. That is huge. I doubt other agents will tell you that.

However, as I said, there are other aspects involved in the underwriting process. For example, if you were recently hospitalized due to your condition (for example), then the hospitalization plays a bigger role in the underwriting decision. Working full-time then doesn’t matter.

If you don’t work because of your condition, no worries. As I mentioned earlier, we can still likely get you some type of life insurance.

Have You Been Hospitalized?

Hospitalization due to bipolar disorder could impact the underwriting decision. The following is a general guide. If you have been in the hospital within 2 years of the application for bipolar disorder, expect a rating or a decline.

If it has been between 2 and 5 years, expect a moderate table rating. Additionally, if it has been over 5 years, then probably a low rating to none at all.

If suicide ideation or attempts were the reason for the hospitalization, that could change the underwriting picture. Usually, any suicide attempt is a decline with most carriers. However, no worries. We still have life insurance options for you.

Type Of Medication

The type of medication matters. Let’s say you use 1 or 2 medications, and they are not antipsychotic drugs. That is usually no issue with most carriers. For example, if your doctor prescribes only lithium, which is a mood stabilizer, then that alone is usually no issue.

As we implied, the prescription of anti-psychotic drugs makes a larger impact. For example, if you take Seroquel, that could place you with a rating.

Again, underwriters balance this decision with other factors in your application.

Type Of Treatment Plan / Are You Following It?

Your treatment plan matters to underwriters. Obviously, if you are following your treatment plan, that is beneficial to your application. Underwriters like that. It shows stability and, usually, no impact on your everyday activities.

your treatment plan, that is beneficial to your application. Underwriters like that. It shows stability and, usually, no impact on your everyday activities.

The type of plan, however, matters, too. If your doctor has you on a first-line psychotherapy treatment, that is great. Moreover, if you have shown to follow your treatment plan with no interruption with normal daily activites, that is beneficial to you.

However, more intense treatment plans like electroconvulsive therapy likely require a rating. Again, this is all determined in conjunction with other underwriting factors.

Bipolar 1 Disorder or Bipolar 2 Disorder?

The type of bipolar disorder matters as well. Some life insurance carriers lump all bipolar disorders together. We usually don’t want to work with those carriers that do that. It shows they don’t know how to properly underwrite your health condition.

As you are aware, bipolar 1 disorder presents more intense and significant manic episodes than bipolar 2 disorder. People with bipolar 1 disorder may exhibit longer manic symptoms compared to those with bipolar 2. Carriers know this, and they know bipolar 1 could hinder normal activities (like working) compared to bipolar 2 disorders.

So, if you have bipolar 1 disorder, then your life insurance options will likely be limited compared to someone who has been diagnosed with bipolar 2 disorder.

As we have said, no worries. We likely can still help you obtain some level of life insurance.

So, What Does Fully Underwritten Life Insurance Mean For People With Bipolar Disorder?

OK, we went through a lot. But, isn’t good to see what is involved in the underwriting process?

So, what does this all mean?

Well, if you want more than $100,000 of life insurance, say $500,000, then you will have an involved underwriting process.

But, that is OK. Most people have to go through paramedical exams and explain their health history. Moreover, the carriers see all that through databases like the prescription drug database.

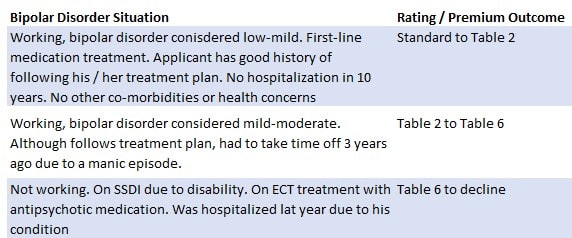

Based on what I described, here’s a table that shows potential ratings for your situation:

Most people we work with end up in the table 2 to table 6 range. Don’t despair; it is still a good premium rate (as you will see later in the article). Moreover, don’t worry if you are declined; we still have life insurance options for you.

Search For Premiums Yourself

You can search for premiums yourself. Just enter some pertinent information like your date of birth. Change the “health class” to “standard”. Note: the premium will likely be a tad higher compared to the rates you will see, but they will give you a decent idea about costs.

(Also, note that we will reserve the right to give you a call or text message, but we aren’t one of those agencies to keep calling and bothering you.

Simplified Life Insurance Underwriting For Those With Bipolar Disorder

John, thanks for sharing the underwriting for me, you say. But, I want less than $100,000 in death benefit.

If that is the case, then you might qualify for simplified underwriting.

Simplified life insurance underwriting is a lot different than the fully underwritten process we just described.

In this case, all the carriers do is (generally speaking):

- Verify your medical background in databases like MIB

- Confirm prescription drug usage in databases like milliman intelliscript

- Review your answers to health questions

- Speak to an underwriter through a personal phone interview

If all works out, then you have life insurance.

The death benefit amounts we are talking about here are low, like $25,000 to $35,000. These amounts are typically burial insurance and final expense policies.

They are usually whole life insurance plans although we work with a few that offer term life insurance.

These face amounts are good for people who don’t work, on SSDI because of their bipolar, have bipolar 1, among other factors.

The underwriting decision is usually quick, usually a day turn-around.

Usually, the main factors in the decision, as we discussed, are:

- Your information in the MIB

- The kinds of medications you take

- Your answers to health questions

Let’s discuss the last two – medications and health questions – in more detail.

How Your Medication Affects Simplified Life Insurance Underwriting For People With Bipolar Disorder

In the previous section, I talked about how the type of medication affects underwriting. For example, if you are prescribed Seroquel, that drug makes a larger impact on the underwriting decision than lithium.

The simplified underwriting process is no different. However, the decision is more “black and white”.

In other words, carriers specifically state which prescription drugs they accept. They also have a list of “knock out” drugs, which means if you were prescribed any “knock out” drugs, then they decline your application.

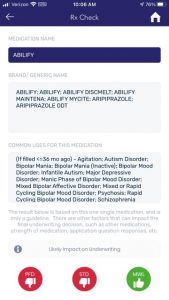

For example, if you take Abilify for your bipolar disorder, the best this carrier below can offer you is a graded-benefit life insurance policy. (More on what that in a minute.)

However, if you take lithium, as you can see, you could receive a standard life insurance policy (which is better compared to the graded benefit).

I’ll go over standard versus graded-benefit in the next section.

So, in your case, we want to work with carriers that are favorable with the medication you have taken and prescribed.

How The Health Questions Affect Simplified Life Insurance Underwriting For People With Bipolar Disorder

The questions on the application matter. If the carrier asks about bipolar disorder or, in some cases, generic mental/emotional disorder, on the application, then likely the disorder is a problem. In other words, they will decline your application.

Here are some real questions from carriers offering simplified underwriting:

![]()

These carriers would deny your application.

These carriers would deny your application.

We obviously do not use these carriers for your situation. Who would we use then?

That is right. The carriers that don’t ask about bipolar disorder on the application.

Moreover, there are many carriers that will cover your health condition.

However, many of these applications have hospitalizations and drug/alcohol abuse questions. If you have recently been hospitalized due to your condition, for example, the carrier will deny your application.

Ok. Now that you know what the carriers look for when someone with bipolar disorder applies for life insurance, let’s discuss the 4 types that are available.

4 Types of Life Insurance That Are Available To People Who Have Bipolar Disorder

We have helped many people with bipolar disorder obtain life insurance. Here are the 4 types that are available. We also go into estimated costs, which are subject to change at any time.

As we said, the availability and eligibility really depend on your situation. Nevertheless, we are confident we can help you obtain some level of life insurance coverage.

As we said, the availability and eligibility really depend on your situation. Nevertheless, we are confident we can help you obtain some level of life insurance coverage.

#1 Fully Underwritten Term Life Insurance Or Permanent Life Insurance

As we suggested in the fully underwriting section, term life insurance or permanent life insurance, like whole life or universal life, is available.

As we discussed, however, the main thing carriers are going to look at is your earning a salary or income with full-time employment.

I know it sounds weird, but working is a normal activity. If you demonstrate the ability to work full-time, coupled with following your treatments, you are likely to get either term life insurance or permanent insurance.

As we said, the actual premium rate you pay is determined by your overall situation.

Here is where you may end up:

- Mild case, working full time, hospitalization over 10 years ago, following treatment plan: standard rate to table 2.

- Mild-Moderate case: still working full-time, but has hospitalization 3 years ago, could be table 2 to table 6.

In fact, most of the people we have helped insure end up in the table 2 to table 4 range.

Is that bad? Not really. Here is what that might cost, for a 40-year-old, male and female, needing $250,000 of term life insurance:

Male: $40 to $60 per month Female: $30 to $55 per month

You can see, the premiums aren’t that bad.

Again, the actual premium depends on your situation.

#2 Simplified Issue Life Insurance – Burial Insurance

Burial insurance is also available. What is burial insurance? It is a whole life insurance policy with a small death benefit, like $30,000. The main purpose of the life insurance is, as the name suggests, is for your burial, funeral, and final expense needs.

Burial insurance is an easy application and underwriting. See the simplified underwriting section above. As long as

- the carrier doesn’t ask about bipolar disorder,

- the carrier accepts your medication, and

- there is nothing else in your background that adversely impacts your application…

…you will obtain burial insurance. It is really that easy.

Additionally, term life insurance policies with small death benefits are available as well.

These policies are key for people who might be on SSDI or SSI, for example. In fact, we have helped many people with bipolar disorder on SSDI obtain burial insurance or small term life policies.

There are a couple of types of burial insurance:

- an immediate benefit pays the benefit, just as it sounds, immediately. If you pass away tomorrow, the carrier pays the benefit…immediately.

- However, a graded-benefit policy pays a percentage of the death benefit or return of your premiums in the first couple of years if you were to pass away.

People with moderate to severe health conditions usually end up with a graded-benefit policy.

As we said, however, we aim for immediate benefit policies. We have helped many people with bipolar disorder obtain immediate benefit life insurance policies.

Feel free to check out premiums, feel free to use the quoter below. If your bipolar disorder is in good condition, select “excellent” under health class. If not, select “decent”. Please note we might give you a call, email, and/or text to say “hello” and see how we can help, but we won’t bother you 1,000 ties per day as other people do.

#3 Guaranteed Issue Whole Life Insurance For People With Bipolar Disorder

If you have a severe case of bipolar disorder, you may think life insurance is impossible for you.

That is right, John, you say. I applied and was denied because of the severity of my bipolar disorder.

Well, I am here to say life insurance is available.

It is called guaranteed issue whole life insurance.

Unlike the fully underwritten and simplified underwriting life insurance, with guaranteed issue life insurance, there is no underwriting.

Hence the name, “guaranteed issue”.

In other words, there is no:

- MIB lookup

- Prescription drug check

- Health questions

- Treatment plan analysis

- etc., etc.

All you do is apply, and viola, you have life insurance.

Sounds great, John, you say. But, too good to be true.

Well, not necessarily. Let me explain how guaranteed issue life insurance works.

How Guaranteed Issue Life Insurance Works

There is no underwriting, that is for sure.

But, carriers that offer guaranteed issue life insurance do not know the health status of applicants. So, they put a “waiting period” on the death benefit.

Usually, that waiting period is 2 years.

That means if you were to pass away by illness or natural causes within the first 2 years of the policy’s start date, your beneficiaries receive the premiums you paid + any interest.

So, it’s like I get my money back…well, my beneficiaries do, right?

That is right. Keep in mind, when I hear people say they don’t want guaranteed issue life insurance, I ask them what they will do next.

They tell me they will save.

You would need to have a return of like 5,000% in the next 2 years to get any significant amount saved.

I tell them with the guaranteed issue life insurance, you are already saving. If you pass away in the next 2 years, then your family receives the premiums you paid + interest. It is even better than saving, because after 2 years, then your policy pays 100% of the death benefit.

People tell me it is too expensive.

Estimated Premiums

Well, it could be. However, check this out. Here is a real guaranteed issue rate for a 60-year-old female wanting $10,000 of life insurance versus an immediate benefit (subject to change any time):

- Guaranteed issue: $41 per month

- Immediate benefit: $35 per month

So, the guaranteed issue life insurance isn’t that much more.

How we approach all this: well, we will try for an immediate benefit first, but if you don’t qualify, then we will pivot to a guaranteed issue life insurance policy.

Don’t forget: guaranteed issue life insurance is usually whole life insurance. It has cash value. If you are on Medicaid, the life insurance may affect your Medicaid assistance. Contact us to learn more.

Additionally, we offer guaranteed issue life insurance for people age 40 and less.

If you want to see what premiums might cost, enter your pertinent information in the quote below. Select “poor health” under health class. Of course, we might call, email, and text you to say “hello” and thank you for coming to our website. We don’t bother you every day, and if you don’t want our help, you just need to tell us that.

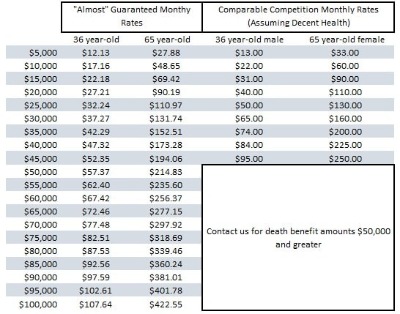

#4 (Almost) Guaranteed Issue Life Insurance For People With Bipolar Disorder

Finally, there is an “almost” guaranteed issue life insurance. How is this different from traditional guaranteed issue?

Well, there is only one question on the application:

“Are you working full-time?”, full-time being 20 hours per week or more.

If you work and earn an income, then you qualify for guaranteed issue life insurance up to $100,000. Currently, the type of life insurance available is whole life.

This “almost” guaranteed life insurance is through a limited partnership. It has an immediate benefit, unlike traditional guaranteed issue. In other words, there is no waiting period.

You just need to work, that is it.

Additionally, you need to agree to join the limited partnership. I won’t get into the detail of why the limited partnership is needed as you can read all about it in our article.

Do you think these premiums are expensive? Check them out. All things considered, I don’t think they are. We recently helped a 36-year-old male and a 65-year-old female with this life insurance. They are both working full-time. See the comparative rates.

Final Thoughts About Getting Life Insurance If You Have Bipolar Disorder

If you have bipolar disorder, you can obtain life insurance. Usually, your health condition is no issue. As we discussed, the type available really depends on your situation.

You can purchase a:

- fully-underwritten policy

- simplified issue policy with a smaller death benefit

- guaranteed issue life insurance

- “almost” guaranteed issue life insurance

I am sure you have questions. Feel free to contact us or use the form below.

If you haven’t realized by now, we only work in your best interest, not our own or any insurance carrier. It’s the only way we know how to work with our clients: place them and their families first. The best part? There is no risk of contacting us.

If you don’t want our help or we can’t help you, we will do our best to point you in the right direction. We will part as friends, seriously! You can always reach back out to us at any time.

Learn More

Are you interested in learning more about the information in this article? Please fill out the form below, and we will email you additional information or give you a call. We always work in your best interest. By entering your information, you are providing your express consent that My Family Life Insurance may contact you via e-mails, SMS, phone calls, or prerecorded messages at any phone number(s) that you provide, even if the number is a wireless number or on any federal or state do-not-call list. Additionally, you understand that calls may be placed using automated technology, and that consent is not a requirement for purchase. Your information will NOT be sold and will remain private. However, you may opt out at any time. We respect your privacy first and foremost. By contacting us, you agree to receive text messages from our number (800) 645-9841. If you no longer wish to receive text messages, you may opt out at any time by replying "STOP".

Published by

4 thoughts on “Here Are 4 Life Insurance Options If You Have Bipolar Disorder | We Discuss The Options And How You Can Get Approved!”

Comments are closed.

I was diagnosed with bi-polar 1 around 7-8 years ago. The only medication that I take, and have taken, for my illness is V****; although I was previously on L*****, too, over 2-3 years ago. I have not been hospitalized for my illness for more than 6-7 years ago. Since my diagnosis, I have continuously been participating in approved rehabilitation or treatment/counseling programs for more than 6 years on a regular monthly basis.

Hi – (because you included health information, I hid your name and medication). Thank you for reaching out to us. Yes, we can help as we have helped many in similar situations. I can give you a call today.

John with My Family Life Insurance

I am currently 100% stabilized for my bi-polar illness, taking only ***** medication, actively participating in appropriate treatment & counseling programs for 6-7 years, and have not been hospitalized for my bipolar illness for a period in excess of 6-7 years. As a result, I am considered to be fully stabilized by my physicians & Therapists for more than 6+ years

Hi – (because you included your medication, we hid your name). Thanks for reaching out to us. Yes, we can help. Stability is key. Have you applied elsewhere for life insurance? I will contact you today.

John