Best Disability Insurance For Real Estate Agents And Realtors [Know Your Options And Protect Your Livelihood]

Updated: January 30, 2025 at 1:24 pm

Real estate agents and realtors usually aren’t thinking about disability insurance, right?

I mean, you’re busy! You are on the go all the time. Open houses, client meetings, touring homes and properties, researching neighborhoods, on the phone, and best of all… closings! Your mental and physical ability to tour properties, represent clients, and show homes are vital to your livelihood.

What if you could no longer do that job? Have you ever thought what would happen to your income if you became sick, ill, injured, and disabled?

How would bills be paid if you could not work? The lifestyle you worked so hard for and your future plans could quickly be affected. In this article, we discuss disability insurance and the best disability insurance for real estate agents and realtors.

Here is what we will discuss:

- Why Real Estate Agents and Realtors Need Disability Insurance

- Types of Disability Insurance for Real Estate Agents and Realtors

- Disability Insurance Structure for Real Estate Agents and Realtors

- Business Owner Disability Insurance Coverage

- Best Disability Insurance for Real Estate Agents and Realtors

- Disability Insurance Underwriting for Real Estate Agents and Realtors

- Estimated Cost of Disability Insurance

- FAQs Disability Insurance for Real Estate Agents and Realtors

- Final Thoughts About Disability Insurance for Real Estate Agents and Realtors

Let’s jump in and discuss why real estate agents and realtors need disability insurance.

Why Real Estate Agents And Realtors Need Disability Insurance

Your clients are very important. There is also a group of people who are more important. Who can be more important than my clients, you think? They pay the bills.

True. They do, but they don’t love you as your family loves you. By far, if you have a family, your spouse and children rely on you more than you think. They love you more than anything.

Additionally, your clients aren’t going to pay your bills if you can’t work, right?

There are tough questions that need answering. Really, consider these questions and think about your lifestyle, your spouse, your children, and the love you have for them:

- Would you and your family be able to continue your standard of living without your income?

- If not, what changes would need to be made?

- Would your spouse have to work or work more?

- Would you need to sell your home to make ends meet?

- Who could be flexible with the children?

- Would you have the money to hire someone to take care of the kids?

As you can see, the tough questions go on and on.

A disability destroys dreams. What are your dreams for you and your family? What happens to these dreams with a disability? They don’t have to, though. You see, disability insurance answers the questions above. Yes, it does! With disability insurance, you have peace of mind knowing that you have a plan – and income – in place should the unexpected happen.

Yes, But A Disability Won’t Happen To Me…Right?

You think a disability won’t happen. However, the probability of having a long-term disability is anywhere between 1 in 3 and 1 in 4 workers. Those disability insurance statistics come from the Social Security Administration. Contrast these disability insurance statistics to unexpected death, say from a motor vehicle accident, which is 1 in 114. Even dying from cancer has better odds: 1 in 7.

But, John, I’m not going to get hurt or be in a wheelchair, you say. I hear this all the time. The truth is that no one knows their future. Moreover, I can write an encyclopedia about the tragic stories and phone calls from people who faced a severe, unexpected disability with no disability insurance.

The fact is, being in a wheelchair is not a common disability. According to the Council For Disability Awareness, 90% of disabilities are from illnesses (like cancer) than from accidents. That means an illness or condition, such as cancer or heart disease, has a higher probability of disabling you than a skiing accident.

Okay, John, but I have workers’ compensation. I don’t need to worry about disability insurance.

That’s great. Workers compensation isn’t disability insurance. Did you know that 5% of disabling conditions are work-related, leaving the other 95% not covered by workers’ compensation insurance? That makes sense since 90% of disabilities are from illnesses.

Let’s revisit the questions I posed earlier.

What’s your plan if you can’t work?

Types of Disability Insurance for Real Estate Agents and Realtors

Three types of disability insurance exist for real estate agents and realtors.

- short-term disability insurance

- long-term disability insurance

- accident-only disability insurance

Short-term disability insurance is designed for disabilities of a short term. For example, a short term disability could be COVID or an injury like a broken hand. Typically, short-term disability insurance covers the disability for a few months (i.e., the benefit period).

If you are still disabled, then long-term disability insurance kicks in. Honestly, long-term disability insurance is more important. While most people can survive financially on a short-term disability, it is a long-term disability that can financially devastate families. Long-term disability insurance has a longer benefit period (more on that later) and more benefits. It provides a massive financial safety net on long term claims (which can happen).

Finally, accident-only disability insurance exists. Think of this as a “last resort” disability insurance as it only covers disabilities from accidents. This type of plan is typically much cheaper with less restrictive underwriting (more on that later) since it doesn’t cover illnesses. As I mentioned, most disabilities are from illnesses rather than accidents.

In this guide, we cover long-term disability insurance for real estate agents and realtors in greater detail, as it is the most important type of disability insurance.

How Disability Insurance Works For Real Estate Agents And Realtors

Hopefully, we have made a great case showing that real estate agents and realtors need disability insurance.

As I mentioned, long-term disability insurance provides a longer benefit period. The longest benefit period available to real estate agents and realtors is “to age 67” coverage. This means that for one disability claim, you could receive a benefit to age 67 (if your disability lasts that long). Most disabilities last only a couple of years, so a different benefit period, like 5 years, can work, too.

Let’s discuss disability insurance basics for real estate agents and realtors in more detail.

Disability Insurance Policy Basics For Real Estate Agents And Realtors

While every carrier is different, here are the important disability insurance policy basics for real estate agents and realtors.

You first need to understand what income disability insurance companies cover.

Most real estate agents and realtors receive commissions. They are 1099 independent contractors, not employees. Many real estate agents also have partnerships, have their business structured as an S-corp, or have K-1 statements.

I really don’t want to go into the weeds here, but all the disability insurance carriers insure your net income. What is your net income? It is essentially your gross income receipts (i.e., sales) – business expenses. The remaining amount is your net income. If you pay yourself a salary, add that back to your net income.

Why do disability insurance companies insure your net income instead of your gross income?

Your net income is the money you need to pay your electric bill, groceries, your own mortgage, etc. In other words, it’s the money you need to live on.

You’re not paying business expenses if you’re disabled, right? That’s why companies focus on your net income. (However, real estate agents and realtors do have access to a special type of disability insurance that helps pay your business expenses. We discuss this option further in the article.)

You generally can cover up to 60% to 70% of your net income. Every carrier is different, though. Some have 60% coverage maximums. Others have more, up to 80% coverage. For example, if you earned a net income of $80,000, you can insure $4,667 per month (70% of your net income).

What’s The Occupation Classification?

Obviously, your health matters for underwriting. (We will discuss that more.) What you may not know is that your occupation matters, too.

Most carriers will not cover high-risk professions for the simple reason of an increased probability of disability. Carriers classify this risk on a scale of 0 or 1 to 5 or B to 5A. I’m not going into the details of the A versus B. However, you should know the lower the number, the riskier the occupation, and the higher the premium, all things being equal.

Disability insurance companies typically assign an occupation class of 4 or 5, depending on the carrier, the years of your work experience, and the income you make.

Tell Me About This Elimination Period?

All disability insurance policies have an elimination period, or waiting period. Contrary to what you might think, the elimination / waiting period is the time that elapses before you are eligible for disability benefits. An example will make this clear.

Let’s say you have a disability insurance plan with a 90-day elimination period (waiting period). You make a disability claim and are approved for disability benefits. You don’t get your benefits right away. In this example, you have to wait 90 days. During these 90 days, you receive no benefits. On the 91st day of disability, you are eligible for benefits.

However, you won’t receive disability benefits the next day or right away. With long-term disability insurance, you’ll receive them around 15 to 30 days later. So, on a 90-day waiting period, expect to receive your disability benefit around day 105 to day 120 of your disability.

This means you need adequate savings to carry you and your family until benefits begin.

Lower waiting periods exist. On long-term disability insurance, companies offer 30-day waiting periods for real estate agents and realtors. Of course, the lower the waiting period, the higher the premiums you’ll pay (all things being equal).

Definition Of Disability

The definition of disability matters. You generally want “own occupation” coverage. Own occupation coverage means that a disability insurance company pays a benefit if you can’t perform the substantial and essential duties of your own, regular occupation. In this case, that is your duties as a real estate broker, agent, or realtor.

The definition of disability matters. You generally want “own occupation” coverage. Own occupation coverage means that a disability insurance company pays a benefit if you can’t perform the substantial and essential duties of your own, regular occupation. In this case, that is your duties as a real estate broker, agent, or realtor.

The plans we work with contain this favorable definition for real estate agents and realtors. Without getting in the weeds, various types of own occupation definitions exist. However, you will want some type of own occupation coverage.

You need to be aware of the “any” occupation definition. This disability definition exists, and I see it on many competing disability insurance quotes or existing disability insurance contracts (established by other insurance agents).

According to this definition, you’ll receive disability benefits if you can’t do the work of any occupation based on your education and experience. Let’s look at a quick example that showcases the impact of the any occupation definition.

You break your leg severely and also tore your ACL. You can’t work as a real estate agent. How can you show homes and meet with clients? Your policy has the “any” occupation definition. Instead of receiving a benefit, the carrier tells you that, based on your experience and education, you could work in an office or provide customer service assistance over the phone.

This definition is similar to that of Social Security disability insurance. It is very stringent. You essentially can’t do any type of job to receive benefits.

If you had the own occupation definition, no doubt you’d receive that disability benefit.

Optional Disability Insurance Riders

There are various additional disability insurance benefits available through the purchase of riders.

Riders allow you to customize your policy. However, you’ll pay more. Disability insurance riders typically include the following:

Partial / residual disability: contrary to what you may think, a total disability isn’t the only way to receive a benefit. Partial disabilities happen all the time. However, most of the time, you need to insure this disability through a rider. The residual disability is like an enhanced partial disability benefit rider. Most residual disability riders include a recovery benefit, which allows a benefit when you return to work after a total disability.

Return of Premium Rider: If you never make a claim, you can receive all of your premiums back. However, this option is rather limited and can be expensive. I have a better suggestion. Contact us to learn more.

Guaranteed Insurability Option Rider: Allows you to purchase additional coverage in the future without evidence of good health (i.e., NO underwriting). You generally can purchase additional coverage every 2 years up to age 55.

Retroactive Injury Benefit Rider: This rider pays benefits from the date of disability due to injury if disability occurs within 30 days of the injury and continues through the elimination period.

Activities of Daily Living Rider: This rider pays an additional benefit if you can’t perform two or more of the activities of daily living. Additionally, it will pay if you are cognitively impaired.

You can spend a lot of money on riders, and your costs will go through the roof. Riders are neither good nor bad; you just want to make sure they make sense in your specific situation. However, I believe every contract needs the following to create a solid, formidable plan:

- own occupation coverage

- partial/residual disability benefits

- guaranteed insurability options

Protect Your Real Estate Business If You Are A Business Owner

Remember I mentioned that you can insure your business expenses? If you own your real estate agency or are self-employed, you have an advantage. You can enroll in a policy that will pay your business expenses upon a disability. The policy is called a business overhead expense policy. Premiums are tax deductible. If structured properly, benefits are tax-free as well.

The advantage of this type of policy is that it pays your business expenses. Many real estate agents use the money to pay for their office rent, licensing, etc.

This type of policy will ensure your real estate business remains solvent during your inability to work from a disability. This is another reason real estate agents and realtors need disability insurance.

Carriers who offer this type of insurance typically offer a discount.

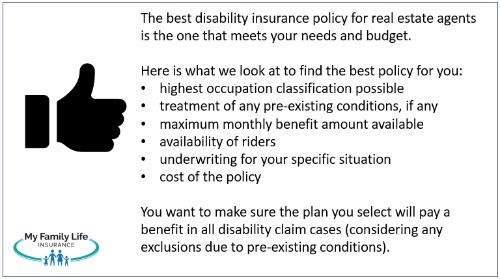

The Best Disability Insurance For Real Estate Agents And Realtors

The best policy is the one that meets your needs and budget. At My Family Life Insurance, we work with many disability insurance companies favorable to the real estate broker and agent occupation. They are A-rated companies, many of which have existed for over 100 years.

The right company for you is on a case-by-case basis. However, here are the factors we consider when looking for the best disability insurance policy for you:

(1) highest occupation classification possible

(2) treatment of any pre-existing conditions, if any

(3) maximum monthly benefit amount available

(4) availability of riders

(5) underwriting for your specific situation

(6) cost of the policy

As mentioned, we ensure your policy has the 3 “formidable” characteristics of the own occupation definition, enhanced partial disability / residual benefits, and guaranteed insurability options.

Contact us. We can help. We work with many disability insurance companies and can find the one that meets your needs and budget.

Disability Insurance Underwriting for Real Estate Agents and Realtors

If you apply for disability insurance, you need to know how underwriting works for real estate agents and realtors.

John, I already got life insurance. I know how underwriting works.

John, I already got life insurance. I know how underwriting works.

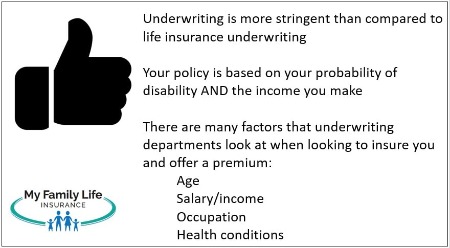

Disability insurance underwriting is completely different from life insurance underwriting, and in fact, it is more stringent. I have had clients get approved for life insurance with no problem; however, they are declined for disability insurance.

What? How?

Disability insurance underwriters look at your chance of disability and the income you make. As I mentioned earlier, your chance of a disability is like 1 in 4 (from the Social Security Administration). The chance of an unexpected death is much, much, much smaller. However, there’s no dispute about how important life insurance is. We all know someone who died unexpectedly and too soon.

Disability insurance underwriters look at the following factors:

(1) your age and gender

(2) occupation

(3) the income you make

(4) your health, nicotine use, pre-existing conditions, etc.

(5) lifestyle situations (like marijuana use, driving habits, etc.)

(6) anything else the underwriter deems material to your application

Although the disability insurance underwriting process has changed with many carriers (for the better), underwriters may require:

- a phone interview to clarify answers on the application

- your tax returns or W-2 to verify income

- a paramedical exam to obtain verified height/weight, blood work, and urine sample

- your medical records if you have a moderate to severe pre-existing condition

If you have any questions, please consult our disability insurance underwriting guide or contact us.

Estimated Premium Cost of Disability Insurance for Real Estate Agents and Realtors

Many realtors and real estate agents want to know how much disability insurance will cost. Well, underwriting determines the cost. It is a function of everything we discussed in the underwriting section. If you are older, expect to pay more than someone younger (all things being equal). If you are not as healthy, expect to pay more than someone who is.

Having said that, we aim to get you the lowest premium cost for your given situation. We have this advantage by working with many disability insurance companies. We know you have other things to pay for, so our focus is on getting you the best disability insurance policy for your given situation. The best means the lowest premium and a policy that pays a benefit to you no matter what (of course, subject to pre-existing conditions and specific plan exclusions).

Nevertheless, expect to pay between 2% and 5% of your net income / gross salary. I think you’ll agree that 2%, 3%, or whatever the number is low. Usually, the cost averages the cost of a cup of coffee from your favorite coffee shop. I think you’ll agree that if you can pay for a cup of coffee each day, you can afford disability insurance.

Frequently Asked Questions About Disability Insurance

We discuss and answer frequently asked questions about disability insurance and real estate agents.

Why Do Real Estate Agents Need Disability Insurance?

Disability insurance is the only type of insurance that pays a benefit if you are sick or hurt and can’t work. It pays a percentage of your salary or income back to you so that you can pay for:

- your mortgage

- car payment

- health costs

- groceries

- heat and electricity

- gas

- you name it

Without disability insurance, how will you make ends meet if you are sick or hurt and can’t bring in an income? This is how disability insurance helps. If you are a realtor with a solid income, and your family relies on that income, you need disability insurance.

My Friend Says Disability Insurance is Health Insurance. I Already Have Health Insurance, so Why Do I Need Disability Insurance?

Your friend is wrong. Health insurance isn’t disability insurance. Health insurance pays for a portion of your medical bills. Disability insurance pays you a portion of your salary or net income. You can (and should) have both. Here is an example to make things clear.

Joan is a top real estate professional in her town. She makes a lot of money and has a nice lifestyle. However, she hasn’t been feeling well lately. After many doctor visits and tests, an oncologist diagnosed Joan with leukemia. Chemotherapy will start immediately. Joan averages $30,000 monthly in real estate earnings. Currently, she has no disability insurance.

Her health insurance pays for most of her medical bills – CT scans, blood work, hospital visits, chemotherapy, etc. However, she still has out-of-pocket costs that she needs to pay.

More serious, however, is that she has no disability insurance. She has a good prognosis, but her doctor thinks she will be out a year – or more – battling cancer.

Without disability insurance, how does Joan pay her mortgage, utilities, medical costs, etc.?

Note: If she had disability insurance, she could have had a monthly benefit of around $18,000 to $19,000. This would have been enough to pay her mortgage and give her peace of mind while she battled cancer. Now, do you see the benefits of disability insurance?

If you think this story is made up, it is not. It is from a phone call I received from a real estate agent who called me too late. (Of course, I changed the name.)

If you are like Joan, without disability insurance, please call me.

How Much Coverage Can Realtors Qualify For?

The amount of disability insurance coverage depends on the income you make. Most disability insurance companies will insure between 60% and 70% of your net income. A couple others could be higher.

The reason you do not receive 100% of your income is:

(1) your monthly benefit is income tax-free

(2) incentivize you to get back to work

Note: You could achieve 100% of your income if you enroll in a catastrophic disability benefit rider. The catastrophic benefit rider pays an additional benefit, in addition to your monthly benefit, if your disability prevents you from performing 2 out of 6 activities of daily living or you have cognitive impairment.

I Am Offered Disability Insurance Through My Association. Anything Wrong With That?

Many associations offer disability insurance. Associations like the National Association of Realtors and many state realtor associations offer some type of disability insurance.

The Hartford, New York Life Insurance Company, and MetLife are the more common disability insurance companies that support association disability insurance plans.

While it may sound good to purchase a disability insurance plan through your association, know that many association disability insurance plans are very limited.

For example, many of them offer a modified own occupation definition for 2 years followed by the any occupation definition. Maybe that is OK for you, but I would want (for peace of mind) my monthly benefit based on some form of own occupation definition throughout the benefit period.

Additionally, many association plans do not have partial benefits. If they do, they are rather limited.

Moreover, association plans typically coordinate your disability benefit with social security. As I mentioned earlier, that just creates more work and red tape for you if you make a claim.

Riders aren’t plentiful as well.

Association plans are cheap…and they have to be. Carriers keep the plans plain vanilla to meet everyone’s needs. So, while you may pay a much lower price than a private, individual plan, you’ll (generally) have a plan with limited benefits if you make a claim.

Does Disability Insurance Cover Pregnancy / Child Birth?

Yes, short-term disability insurance will cover pregnancy or normal childbirth as an illness. In other words, you can make a claim, which becomes like a paid maternity leave. We have a plan that has a 9-month waiting period on childbirth claims. In other words, the plan MUST be in force a minimum of 9 months to qualify for childbirth benefits.

I recommend getting the short-term disability insurance policy well in advance so the 9-month waiting period isn’t an issue when you make a claim.

Long-term disability insurance does not cover normal childbirth. However, it covers complications of pregnancy or childbirth.

If you would like a quote on short-term disability insurance or have questions, don’t hesitate to contact us.

Now You Know About Disability Insurance For Real Estate Agents And Realtors

We hope now you have a solid idea why real estate agents and realtors need disability insurance. This was a very thorough guide. We discussed:

- the need for real estate agents to have disability insurance

- types of disability insurance available

- structure of a policy

- disability insurance underwriting

- premium costs

Confused? Don’t feel that way. We’re here to help educate you and protect your income and future. Feel free to contact us or use the form below for our assistance or a quote. We only work for you, your family, and your best interests only. We have helped many real estate agents and realtors secure the right disability insurance for their specific situation, giving them and their families peace of mind. I am confident we can help you, too.

Learn More

Are you interested in learning more about the information in this article? Please fill out the form below, and we will email you additional information or give you a call. We always work in your best interest. By entering your information, you are providing your express consent that My Family Life Insurance may contact you via e-mails, SMS, phone calls, or prerecorded messages at any phone number(s) that you provide, even if the number is a wireless number or on any federal or state do-not-call list. Additionally, you understand that calls may be placed using automated technology, and that consent is not a requirement for purchase. Your information will NOT be sold and will remain private. However, you may opt out at any time. We respect your privacy first and foremost. By contacting us, you agree to receive text messages from our number (800) 645-9841. If you no longer wish to receive text messages, you may opt out at any time by replying "STOP".