3 Life Insurance Options Approved For An Autistic Child | Life Insurance Is Available. We Discuss Your Options.

Updated: April 12, 2024 at 9:38 am

In this article, we are going to discuss how parents can get life insurance for their autistic child.

In this article, we are going to discuss how parents can get life insurance for their autistic child.

Contrary to what you may have heard, you can obtain life insurance.

If you have an autistic child, have you applied in the past?

Was your son or daughter declined?

Unfortunately, that decision happens often for parents.

However, I am here to tell you it is possible to obtain life insurance for children with autism.

We’ve helped many families do so, and I am sure we can help you out, too.

Like anything, there is a “right way” and a “wrong way” to go about things.

We will tell you the “right way” to go about getting life insurance for your son or daughter.

In this article, we discuss:

- Why Life Insurance Companies Decline Autistic Children

- 3 Life Insurance Options For Your Autistic Child

- Approximate Cost Of Life Insurance

- Watch Out For This Major Misstep!

- Final Thoughts

Let’s jump right in and discuss why some carriers decline children with autism. Essentially, in this section, we discuss HOW you can get life insurance for your autistic child.

We then discuss life insurance availability, estimated cost, and a major misstep parents potentially make.

Why Life Insurance Carriers Decline Your Autistic Child

Obtaining life insurance for someone with autism can be tricky.

Many life insurance companies simply decline children with an autism diagnosis or confirmed with an autism spectrum disorder.

I’ve had many parents call me. They are upset that their child has been declined. Their child is in good health in every way and just has an autism diagnosis.

Here is why. Generally speaking, people with autism have a much lower life expectancy compared to a typical person. It is documented.

It’s not necessarily the autism itself. Rather, it is a combination of autism and other medical conditions.

However, we’ve worked with many parents who previously tried to purchase life insurance for their autistic child. We have been successful.

They may have applied at popular carriers like Gerber Life or Globe Life.

Both are solid life insurance companies, but are generally not good for children with autism.

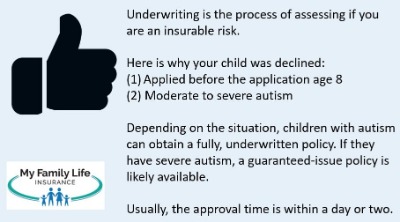

There are two main reasons why the carrier declined your child:

- He or she was too young to apply

- He or she has moderate to severe autism

We discuss these important points next.

Application Age

Many carriers have a minimum application age for children diagnosed with autism. That age is age 8, usually.

Why age 8, you ask?

That is when carriers have a good idea of the prognosis of your child and his or her future.

So, if you apply for life insurance when your child is, say, age 5, the carrier likely declines the application.

You’ll just have to apply around age 8. I even recommend waiting until age 10. Certainly, feel free to contact us. We can reach out to the carriers and see if their minimum age has changed.

Moderate-To-Severe Autism

The other reason carriers decline is due to the severity of the autism. Let’s say you apply for life insurance when your child is 9. If your child has severe autism, the carrier will decline the application.

Unfortunately, they can be healthy every other way. But, if they don’t communicate well, need assisted devices, and have trouble with ADLs, carriers will decline the application.

This is a good time to discuss the underwriting process for children with autism. Here’s what the carriers look at when you apply for life insurance.

Life Insurance Underwriting For Autistic Children

Underwriting is the process of reviewing an application and determining the insurable risk. It is a key component to all insurance – auto, home, disability, life, etc.

If the risk is too great, the carrier will either apply a table rating or decline the life insurance altogether. Here is, generally, what they want to know specifically about your child’s autism:

- if your child is in a mainstream classroom

- if he or she needs an aide

- does he or she communicate via spoken language

- does he or she have relationships with peers

- can he or she perform ADLs independently

- are these supported by IEPs or neuropsychology reports

- any documented IQ tests

Then, carriers also look at the following:

- Height and weight

- Any other health conditions and medical history (through medical records review)

- Any other previous moderate to severe injuries

- Neuropsychological evaluations including IQ tests

As you can see, underwriting is the key attribute in the application process.

If any of the above elements present an adverse outcome, the carriers will apply a table rating or decline altogether.

No worries, though. As we said before, we can likely get you some type of life insurance for your autistic child. Let’s discuss those options next.

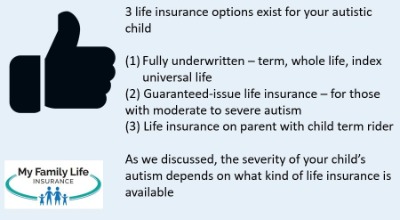

3 Life Insurance Options For Your Autistic Child

As we discussed, life insurance options exist for autistic children. The type of life insurance depends on the severity of the autism and then any other pertinent underwriting factors such as height and weight.

The way I see it, there are 3 life insurance options for your child. The good news is that your child can be approved rather quickly, even within a day or a few days. Let’s talk about these options next.

The way I see it, there are 3 life insurance options for your child. The good news is that your child can be approved rather quickly, even within a day or a few days. Let’s talk about these options next.

Fully Underwritten Life Insurance

If your child has low to mild autism and high functioning, then expect any type of life insurance available. In other words, your child is eligible for a fully underwritten plan.

Usually, children with Asperger’s syndrome or high functioning are eligible for fully underwritten life insurance.

That means whole life, index universal, and even term life insurance on children is available.

Don’t worry. Your child won’t have a paramedical exam or anything like that. They are too young for that. Underwriters won’t require a medical exam.

Carriers will likely classify your child at a standard rate up to table 2 or table 4. That’s just a fact. Remember the life expectancy.

If your child has mild autism, the best thing to do is contact us so we can estimate the rate.

Guaranteed-Issue Whole Life Insurance

f your child has moderate to severe autism, then a guaranteed-issue whole life insurance policy is available.

But, John. Guaranteed issue is only available to those who are age 50 and older, you say.

That is generally true, but there is a carrier that offers guaranteed-issue life insurance for individuals as low as a newborn.

So, there are options, as long as the life insurance is available in your state.

With any guaranteed-issue life insurance, there is a 2 year waiting period on the death benefit. This means if your child passes away (illness or natural causes) in the first 2 years of the policy’s start date, you receive the premiums you paid plus any interest back.

So, it is like a return of premium in those first 2 years.

After 2 years, the death benefit is paid 100% no matter what.

Guaranteed issue life insurance is a good option, and probably the best option, if your child has moderate to severe autism.

Anyone can pass away at any time. But, if your child is healthy, then the chances of surviving the waiting period are high.

Life Insurance On Yourself With A Child Rider

How about life insurance on yourself?

Many parents don’t think about that.

Well, John. I already have life insurance, you say.

Sure. Most people do. However, most people are don’t have enough life insurance. If you passed away tomorrow, will your death benefit provide support for your autistic child?

Having an additional policy on yourself, intended for your child, is a prudent approach.

If you pass away before your child, which likely will happen, the death benefit can be used to fund your autistic child’s future and needs.

The life insurance should be placed in a special needs trust. Upon your passing, the death benefit proceeds are paid out of the trust for your child. Generally speaking, this doesn’t affect Medicaid qualification or SSI assistance. (However, you still want to speak to a qualified attorney about the laws in your state.) We discuss this later.

Additionally, many of these carriers have child term riders to which you can add your child. These riders are guaranteed issue with a couple of carriers. That means, no health questions or underwriting. Moreover, it is an immediate benefit (no 2-year waiting period).

Child riders have limited death benefit amounts. Most carriers that offer child riders limit the death benefit to $25,000. It is basic term life insurance. However, when children are adult age, they can usually convert the term to whole life insurance.

Approximate Cost of Life Insurance On Your Autistic Child

As we mentioned, if your child is high-functioning with low to mild autism, then expect a standard rate to table 2 on life insurance.

How much is this?

Well, it depends.

$50,000 whole life insurance on a 1 year-old boy costs around $30 per month, maybe more and maybe less depending on the carrier.

Feel free to check out costs:

Term life insurance on your child is also possible. With one carrier we work with, you could purchase $20,000 for $25 annually. Yes, each year. In other words, you pay $25 each year. Cheap.

Index Universal Life is also available. Additionally, if you enroll in a life insurance plan with living benefits, your son or daughter potentially has a long-term financial planning tool.

If your son or daughter has moderate to severe autism, then a guaranteed issue plan is likely the only option.

Again, there is a 2-year waiting period with guaranteed-issue life insurance. After 2 years, the death benefit is 100% paid.

A $25,000 guaranteed issue whole life insurance policy on a 5-year-old boy costs around $95 per month.

What To Do When They Are Older – Watch Out For This Misstep

Parents or Grandparents mean well when they purchase life insurance for their autistic child or grandchild. However, there is a potential misstep when these children are older.

At adult age, as determined by your state (usually, 18 or 21), your son or daughter technically becomes the owner of the life insurance policy.

Everything is OK if your son or daughter is a typical child. Even if your son or daughter is high-functioning, having him or her be the owner shouldn’t be an issue.

Life insurance on an autistic child gets really complicated and tricky in one situation, however.

This situation happens if he or she has moderate to severe autism in adulthood.

You see, at legal adult age – say age 18 – the state says your child is the legal owner of the policy. As the owner, he or she is able to make decisions about the policy, like changing the beneficiary, borrowing from the policy if it has cash value (etc.)

However, if your child has severe autism, then likely he or she can’t make those decisions. Yet, the state says, by law, he or she must. You see? Do you see the problem? This can be a major problem.

Additionally, if your son or daughter receives state assistance through Medicaid (like supplemental security income), having cash-value life insurance potentially disqualifies him or her from this assistance.

There are ways around this, however.

Before we discuss, let me say that we are not lawyers. I recommend that you speak to a qualified attorney specializing in special needs children regarding the laws in your state. However, what I discuss next is a general overview.

Power Of Attorney Or Guardianship

Obtaining proper guardianship or power of attorney helps.

Guardianship or power of attorney rights gives you the authority to make decisions on your child’s behalf. This usually occurs at adult age.

You’ll want to make sure these rights include signing documents on your child’s behalf. This includes insurance documents.

You’ll apply as the owner of the policy. Just make sure you yourself are not on Medicaid or anything like that. If you are, then owning the policy will affect your aid and resources.

Special Needs Trust

Additionally, you may want to create a special needs trust for your child.

A trust is a separate entity. Your child’s situation (and your situation, for that matter) will not affect the trust. Medicaid and other creditors can’t touch the money and value inside the trust. This includes life insurance.

Life insurance can easily be retitled to the trust.

Upon your child’s passing, the trust receives the death benefit money. It then pays out according to the terms of the trust.

As we mentioned earlier, we recommend you speak to a qualified attorney in your state. An attorney specializing in special needs situations will guide you the right way among your state laws.

There’s a lot here that we touched on. Everyone’s situation is different. The moral of this section: before your son or daughter becomes adult age, think about how you want the life insurance structured. If you don’t do anything, life insurance in your son’s or daughter’s name (as owner) may adversely impact them.

Final Thoughts About Life Insurance On Your Autistic Child

You can obtain life insurance on your autistic child. As with anything, there is a right way of doing so.

As mentioned, traditional types of life insurance are available to children with low to mild autism.

If your child has severe autism, a guaranteed issue life insurance policy is the only option.

We also discussed probable costs. Moreover, we discussed options on how you need to structure the life insurance policy when your child is an adult.

Do you have questions or need assistance? We can help. Contact us or use the form below.

There is no risk with contacting us. I know that sounds hard to believe! You see, we only work in your best interests. If we can’t help you, we will point you in the right direction as best we can. We’ll part as friends, and you can always reach back out to us should your situation change. It’s the only way we know how to work with our clients.

Learn More

Are you interested in learning more about the information in this article? Please fill out the form below, and we will email you additional information or give you a call. We always work in your best interest. By entering your information, you are providing your express consent that My Family Life Insurance may contact you via e-mails, SMS, phone calls, or prerecorded messages at any phone number(s) that you provide, even if the number is a wireless number or on any federal or state do-not-call list. Additionally, you understand that calls may be placed using automated technology, and that consent is not a requirement for purchase. Your information will NOT be sold and will remain private. However, you may opt out at any time. We respect your privacy first and foremost. By contacting us, you agree to receive text messages from our number (800) 645-9841. If you no longer wish to receive text messages, you may opt out at any time by replying "STOP".