Best Disability Insurance For Podiatrists | We Discuss This Important Insurance & The Best Options Available

Updated: April 12, 2024 at 9:39 am

As a podiatrist, your work is hands-on and busy. Most podiatrists don’t wake up in the morning and think, “Today is the day I’m going to look into disability insurance.”

As a podiatrist, your work is hands-on and busy. Most podiatrists don’t wake up in the morning and think, “Today is the day I’m going to look into disability insurance.”

I think you’ll agree with me on that. And, you go about your day.

However, what if you could no longer do that job?

Have you ever thought about what would happen if you became sick, ill, injured, and disabled?

How would you pay the bills if you could not work?

How long could you stretch your savings? (Probably not that long…)

Disability quickly affects your future plans and the lifestyle you worked so hard for. In this article, we discuss disability insurance and the best disability insurance for podiatrists.

For faster navigation, feel free to click on a link below:

- What Is Disability Insurance?

- Why Do You Need Disability Insurance?

- How Carriers Underwrite Podiatrists

- Elements Of A Disability Insurance Policy

- The Best Disability Insurance

- Is An Association Plan Right For You?

- Other Important Options For Podiatrists

- Now You Know The Best Disability Insurance To Protect Your Income Now

Let’s jump in and give a quick overview of disability insurance.

What Is Disability Insurance?

Disability insurance pays you a benefit if you can’t work due to illness or injury. It is that simple.

Essentially, if you:

- Make money, and

- You and your family rely on that money to live, and if

- You and your family would be in financial disarray if you were sick or hurt and could not work, then

Think of disability insurance as “paycheck protection”. We have our house, cars, vacations, luxury items, and necessities. Think of all that. All of that is derived from your ability to work and earn an income. Likewise, all of that is potentially gone with your inability to work and earn an income.

How much benefit do you receive if you can’t work? That depends on how much you make and your income. If you are an employee or a self-employed po diatrist, carriers pay between 60% and 80% of your income/salary.

diatrist, carriers pay between 60% and 80% of your income/salary.

Why don’t they pay 100%? Well, the reasons are simple:

- The disability benefit isn’t taxable, so that saves a ton of money, and

- To incent you to get back to work

Human nature tells us if we receive 100% of our income, we might as well stay home, right?

Another way to think of disability insurance is the spare tire in your car or AAA. If your battery dies or you have a flat tire, you are really happy to have the spare tire or AAA. You don’t want to use it, but you are happy it is there and available if you need it. Except, disability insurance is the spare tire for your life.

Why Podiatrists Need Disability Insurance?

That sounds great, John, you say. But, I am not going to need disability insurance.

That’s an interesting comment. Tell me about some of your patients.

Well, some are healthy and some are not.

OK, about those who are not. Why do they see you?

They have injuries or chronic problems, like diabetic ulcers, they need help with.

Did they expect to have these problems? These likely were or are disabilities.

Well…

You don’t need to answer that. I can see you know what I am getting at. The answer is no one does. A disability happens anytime. Disabilities do not discriminate. They don’t care about your ethnicity, income, or situation.

You don’t need to answer that. I can see you know what I am getting at. The answer is no one does. A disability happens anytime. Disabilities do not discriminate. They don’t care about your ethnicity, income, or situation.

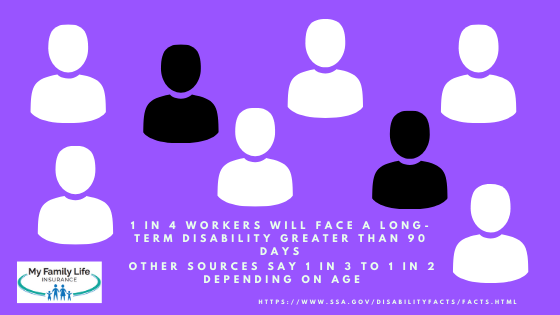

In fact, the SSA says that 1 in 4 working adults will be disabled before they turn 65.

Tiger Woods knows this. As of this writing, he is disabled. Surely, you heard about his accident. He entered his car at 7AM. By 7:10, he may not play golf again. Golfing is his job. He can’t do that. I can bet with certainty that at 7AM, he did not expect a disability. No one does.

What if you faced a situation where you could no longer practice? That is a disability.

However, a disability isn’t only a severe accident. It can be a cancer diagnosis, an ALS diagnosis, weird nerve pain shooting through arms that prevents you from using your hands.

Any type of illness or injury that prevents you from doing your job is a disability.

What would you do if you could not bring in an income to support your family?

Now, do you see the importance of disability insurance for podiatrists?

More Important People Rely On You

So, now we know a disability happens anytime. Before this discussion, I bet you valued your patients quite a bit. Am I right?

Well, yes. They bring in my income. Without them, I am nothing.

Yes, your patients are very important. However, there is also a group of people who are more important. Who can be more important than my patients, you think. They pay my income. Without them, I wouldn’t have an income.

True. They do pay your income, which keeps your business going. However, they don’t love you as your family loves you. By far, if you have a family, your spouse and children rely on you more than you think. They love you more than anything.

True. They do pay your income, which keeps your business going. However, they don’t love you as your family loves you. By far, if you have a family, your spouse and children rely on you more than you think. They love you more than anything.

If you are faced with a disability, without disability insurance, there are tough questions that need answering.

- Would you and your family be able to continue your standard of living without your income? If not, what changes would need to be made?

- Would your spouse have to work or work more?

- Would you need to sell your home to make ends meet? (just happened to a prospect I spoke to.)

- Who could be flexible with the children?

- Would you have the money to hire someone to take care of the kids?

The tough questions can go on and on.

Disability is known as the destroyer of dreams. Your future and family dreams could be destroyed. They don’t have to, though. With disability insurance, you have peace of mind knowing that you have a plan – and income – in place should the unexpected happen.

Think about that spare-tire analogy from earlier…

OK, John. You have made your point. I need this insurance. How do I get it?

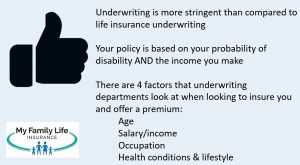

Well, let’s first discuss disability insurance underwriting.

How Disability Insurance Carriers Underwrite Podiatrists

Hopefully, we have made a great case showing that podiatrists need disability insurance.

Before you apply, however, you need to know how carriers underwrite occupations.

For podiatrists, disability insurance underwriting is usually “in the middle”. I’ll explain what that means.

First, though, let’s start at the beginning.

When it comes to underwriting, carriers look at your:

- Age

- Health

- Income / Salary

- Occupation

- Other hazards and lifestyle situations

If you are healthy, then that shouldn’t be an issue. But the unhealthier you are, the more costly the policy will be. Moreover, carriers limit benefits depending on the

severity and type of health condition.

Age is age. The older you are when you apply, the more expensive the policy. That happens to everyone. This is why we recommend applying as soon as possible to lock in relatively lower premiums.

Your Occupation Matters In Disability Insurance

Carriers also look at your occupation.

All the disability insurance carriers classify occupations based on disability risk.

Carriers classify this risk on a numerical scale, usually from a 1 to a 5 or a 6. A 5/6 occupation class is the lowest disability risk. Conversely, an occupation with a 1 has the highest disability risk.

For example, two people have the same birthday, height/weight, health status, and income. One is a construction worker and the other is an accountant. The construction worker pays more simply due to occupation compared to the accountant (all things being equal, of course).

For podiatrists, disability insurance carriers classify the occupation at a 3 or a 4.

That means moderate disability risk.

Now that you know how disability insurance carriers underwrite, let’s go over some important policy characteristics for podiatrists.

Important Elements Of A Disability Insurance Policy For Podiatrists

You’ve worked hard to make a living. Likely, you had tons of certification exams, board exams, and residencies. It took a lot of hard work to get where you are at today.

You want your policy to reflect that hard work. In other words, you want to make sure you have enough coverage in case you file a claim.

We all want to save money, but being economical here does not help anyone. In particular, a skimpy plan does not help your family at all.

One of the largest disability insurance mistakes I see is cost being at the centerpoint, at the expense of coverage.

It should be the other way around.

Having said that, there are ways to save on premiums AND still have a comprehensive policy.

We specialize in that. We don’t allow our clients to spend needlessly. Contact us if you would like to learn more.

Nevertheless, let’s jump into some important disability insurance policy basics for podiatrists.

Disability Insurance Basics For Podiatrists

While every carrier is different, here are the important policy basics for podiatrists.

You generally can cover up to 70% of your gross salary. Every carrier is different, though. Some have 60% coverage maximums. For example, if you have a gross monthly salary of $5,000, you can cover up to $3,500 (70%).

If you are self-employed, carriers insure your net income, which is your gross income less any business expenses. This is typically found on schedule C of your tax return.

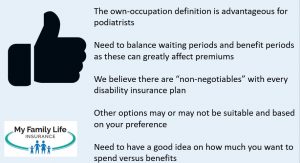

What Is The Elimination Period / Waiting Period And Benefit Period?

There is an elimination period, which is like a deductible. It is the length of time – a waiting period – that elapses before disability benefits begin upon an approved claim. For example, a 90 day elimination period means your benefit period will begin after 90 days of disability. You typically won’t get paid until 30 days later, until day 120. This means you need to have adequate savings to carry you and your family until benefits begin.

You can usually go as low as 30 days, but you will pay a higher premium.

We find that many individuals and families can “get by” for a few months of disability; however, it is after 90 days that they feel a negative financial impact.

The maximum benefit period is “to age 67” coverage. This is based on claim. Let’s say you’ve had your policy for 3 years, and you severely hurt your back skiing. Per your policy, you could receive a benefit until age 67 for your hurt back IF a doctor feels that you could never return to your podiatrist occupation.

The Definition Of Disability Matters…

The definition of disability matters. You generally want some type of own occupation period. This could be “true” or “modified” own-occupation definition.

The definition of disability matters. You generally want some type of own occupation period. This could be “true” or “modified” own-occupation definition.

What is “true own-occupation”? Simply, it means you can continue to work in another occupation while receiving disability benefits for your own occupation as a podiatrist. So, if you can’t use your hands, but you can greet people at Walmart, you will receive disability benefits in addition to your earnings as a Walmart greeter.

Modified own-occupation is a bit different. You will receive a disability benefit based on your occupation as a podiatrist. However, you can’t work in another job. So, if you worked as a Walmart greeter, you won’t receive disability benefits under the modified own-occupation definition.

Finally, there is the stringent “any occupation” definition. This means, simply, if you can work in any other gainful occupation (for which you are reasonably suited, considering your education, training, and experience), the carrier will deny benefits. So, under this definition, you won’t receive a disability benefit based on your education and experience as a podiatrist because the insurance carrier says you can work as a Walmart greeter.

The plans we work with contain the favorable true own-occupation definition for podiatrists.

Optional Disability Insurance Riders

You can add optional riders at an additional cost to your policy to best fit your needs and budget. Some popular rider options for podiatrists include:

Guaranteed Insurability Option Rider: This allows you to obtain the coverage you need now with the option to purchase additional coverage in the future without evidence of good health.

Residual Benefit Rider: This rider will pay a benefit if you are partially disabled in your occupation, and you experience an income loss of 20% or more compared to your pre-disability income. Usually, the amount of disability income you receive is a percentage of your total monthly disability benefit.

For example, you are diagnosed with carpal tunnel in your left wrist. Your doctor wants you to try some relaxation and rehabilitation techniques before considering surgery. Sounds great, but your doctor says you can only work 3 days a week, not 5. That’s a disability. A partial disability, but a disability nonetheless. Let’s say you experience a 40% income loss. If your monthly disability benefit is $4,000, you will receive $1,600 ($4,000 X 40%). Easy math.

It’s important that you select partial disability / residual disability benefits that do not require a total disability first. Many carriers have this negative provision, and insureds are not fully aware until they file a claim.

Let’s use the example above. If your policy said that partial disability benefits are only paid AFTER a total disability, then you would not receive any partial benefits during your rehabilitation. That stinks, doesn’t it?

There are other riders available. Of course, additional riders come with an additional cost. However, these may be important to you:

- Retroactive injury benefit

- Catastrophic disability benefit

- Mental illness/drug use option

- Critical illness option

And more, depending on the carrier.

The Best Disability Insurance For Podiatrists

You are probably wondering who we like to work with. First, we work with many disability insurance carriers. So, we are sure we can find one that meets your needs and budget.

It’s important to note that the “best” carrier is the one who will pay a benefit, and not give you a hard time during a claim.

Additionally, some carriers classify the podiatrist occupation differently. Some carriers are better with some occupations than others.

Here are some of the disability insurance carriers we like to use for podiatrists:

- Illinois Mutual

- Assurity

- Guardian

- Standard

- Principal

- Mass Mutual

- Petersen International

These carriers all contain the important elements we discussed earlier.

I wouldn’t put too much faith in the premium rates you see elsewhere online. They may not be updated or exclude certain provisions. Contact us to learn more, and we can give you a quote.

Keep in mind, too, all of the carriers have different nuances and plan structure. For example, some may have a different definition of disability.

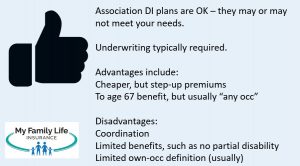

Is An Association Plan Right For You?

Many podiatric associations offer disability insurance. Are these plans right for you? Maybe. Maybe not, though.

Disability insurance plans through associations are usually limited and “plain vanilla”. It doesn’t mean they are bad. It just means they contain a basic structure to meet the needs of everyone.

vanilla”. It doesn’t mean they are bad. It just means they contain a basic structure to meet the needs of everyone.

Some podiatrists think association plans are guaranteed issue. Nope.

You still have to go through underwriting. There’s no avoiding that.

Here are some advantages of association plans:

- Some coverage for pre-existing conditions

- Might be cheaper, initially, but then premiums might “step-up” every year or 5 years

And some disadvantages:

- Other benefit coordination, including group coverage

- Limited waiting periods

- Cap on monthly benefits

- 2 year true own-occupation definition

- To age 65 coverage available, but possibly at the “any” occupation definition

- Partial disability after total disability only (likely) or no partial benefits at all

- Premiums could “step-up” (i.e. increase) as you age

Like anything, there are advantages and disadvantages. Feel free to contact us about any specifics. We are happy to explain, compare, and contrast so you can make an educated decision.

Let’s discuss other disability insurance options for podiatrists.

Other Important Disability Insurance Options For Podiatrists

So far, we have discussed individual long-term disability insurance.

There are other options that may work for podiatrists. We define and discuss them below.

Group Employer Disability Insurance

We have helped podiatrists with group disability insurance. Group employer disability insurance is established through your business.

Group employer disability insurance can be flexible.

No way, you say. I tried that before, and I needed to go through underwriting and participation requirements. Moreover, they would not insure my spouse and me since we are in business together.

So, yes, there are participation requirements if you, as the employer, are not paying 100% of the premiums.

However, we work with one group disability insurance plan that is guaranteed issue. For real.

Additionally, they will insure spouses working together in the business and family members with no restrictions.

Like all group employer disability insurance, the plan:

- Has own occupation and then transitions to any occupation (3 years own occupation)

- Step up rates in 5 year age bands, with a premium freeze for the initial 3 years

- Covers pre-existing conditions

- Will integrate with social security

However, it has additional benefits:

- Carve-out occupations are possible. This means you can insure only the podiatrists or only the office staff. Or, both, with separate plans.

- Covers family members

- Relatively affordable

There are other group employer options as well, including short-term disability insurance. We typically advise against individual short-term disability insurance. Individual short-term disability insurance can be a waste of money. Additionally, short-term disability costs a lot. However, a plan through your business can be more affordable.

If you are an employee without a group employer disability insurance offering, feel free to speak with the business owner and reach out to us. I am happy to go over the plan and answer any questions you have.

Business Overhead Expense Insurance

Business overhead expense insurance is an important type of policy for business-owner podiatrists. This type of policy pays your business expenses if you are disabled.

Business overhead expense insurance is an important type of policy for business-owner podiatrists. This type of policy pays your business expenses if you are disabled.

Sounds great, John, you say. But, I already have this policy.

You actually don’t. Many people think that, but what they really have is business interruption insurance. That is part of your liability or commercial insurance. It pays you for lost income if your business doesn’t operate due to damage, like a fire.

Business overhead expense insurance pays for your business expenses if you can’t work due to a disability. It will help pay for your:

- Rent

- Employee salaries

- Liability, commercial, and other insurances

- Property taxes

- and more

Business overhead expense insurance keeps the lights on, rent paid, and employee’s happy.

Additionally, the premiums are tax-deductible. If you use the policy to pay for your business expenses, then the benefit is income tax-free.

Most of the time, the cost of business overhead expense insurance is very inexpensive compared to an individual policy.

Disability Insurance For Business Loans

Paying back a loan is a serious matter.

Paying back a loan is a serious matter.

You pay a promissory note that says you will pay back the loan…

…no matter what.

What if you get disabled? What do you think happens to those payments?

Oh, John, you say. I’ll just work with the bank or the lender on managing the payments.

You will?

How sure are you about that? That promissory note essentially says you will pay no matter what.

What if you invest in new equipment – or even a loan to purchase a new practice – and suddenly you are disabled?

Do you think the bank will let you off scot-free?

No, you say.

Right. This underscores how disability insurance for business loans protects you. It will continue your loan payments – right to the lender – with no involvement from you.

But, John, what about the individual disability insurance?

That’s for your everyday needs. That pays your mortgage and groceries. It keeps your personal lifestyle afloat while you get better.

If you assign your individual disability benefit to pay your loans, you’ll ultimately be stuck between a rock and a hard place.

A disability insurance plan designed to cover your business loans does the trick. It’s generally affordable, too, because your loans should be lower than your income.

Feel free to contact us if you have any questions. We are happy to help.

Now You Know Why Podiatrists Need Disability Insurance & The Best Disability Insurance For The Podiatry Profession

We hope now you have a solid idea why podiatrists need disability insurance and the ones we like to use for the podiatry profession. Confused? Don’t feel that way. We’re here to help educate you and protect your income and future. Don’t know where to start? Use this disability insurance needs analysis worksheet. Follow the instructions; it is rather easy to fill out (we at My Family Life Insurance try to make understanding insurance easy). Next, feel free to reach out to us for our assistance or a quote. Or, use the form below.

There is no risk of contacting us. We only work for you, your family, and your best interests only. If we can’t help you, we will point you in the right direction as best we can and part as friends. You can always reach out to us again. We have helped many podiatrists secure the right disability insurance for their specific situation, giving them and their families peace of mind. I am sure we can help you out, too.

Learn More

Are you interested in learning more about the information in this article? Please fill out the form below, and we will email you additional information or give you a call. We always work in your best interest. By entering your information, you are providing your express consent that My Family Life Insurance may contact you via e-mails, SMS, phone calls, or prerecorded messages at any phone number(s) that you provide, even if the number is a wireless number or on any federal or state do-not-call list. Additionally, you understand that calls may be placed using automated technology, and that consent is not a requirement for purchase. Your information will NOT be sold and will remain private. However, you may opt out at any time. We respect your privacy first and foremost. By contacting us, you agree to receive text messages from our number (800) 645-9841. If you no longer wish to receive text messages, you may opt out at any time by replying "STOP".