How To Save Your Home With Massachusetts Long-Term Care Insurance [Here Are The Steps And Information You Need To Protect Your Home]

Updated: April 12, 2024 at 9:40 am

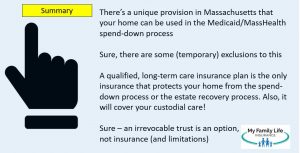

Massachusetts residents who possess long-term care insurance are granted a unique provision. The provision is the only of its kind in the nation.

Massachusetts residents who possess long-term care insurance are granted a unique provision. The provision is the only of its kind in the nation.

Let’s back up a bit. You’ve probably heard about people losing their homes during the estate recovery process. This happens when the state’s Medicaid department files for a claim on your loved one’s estate for using Medicaid for long-term care needs. The state wants to recoup what it paid to your family member.

Massachusetts is different from how they handle the process. You may think you will just let MassHealth pay for your long-term care needs. If you do that, you are setting yourself and your family up for a potential financial disaster (in our opinion). If you are a Massachusetts resident, a long-term insurance policy will protect your home and other assets. In this article, we discuss the steps and information for Massachusetts residents to protect their homes and assets using long-term care insurance.

We discuss the following topics:

- The Long-Term Care Insurance Options

- How You Can Lose Your Assets

- Massachusetts Treats Your Home Differently

- Why A Long-Term Care Insurance Policy Works

- Requirements Of A Qualified Plan In Massachusetts

- Now You Know You Can Protect Your Home And Other Assets

We have discussed the need for long-term care ad nauseam. We won’t discuss that again here. However, to put it simply, you and/or your spouse will most likely need some type of long-term care assistance in your future.

We have discussed the need for long-term care ad nauseam. We won’t discuss that again here. However, to put it simply, you and/or your spouse will most likely need some type of long-term care assistance in your future.

Time is valuable. Here’s a summary sheet about our article. If you don’t think you will need long-term care in your future, think again. Remember, long-term care is about custodial care. That is, someone helping you with normal activities of daily living. Do you really think your children or spouse will be up to the task, in this day and age?

4 Options For Your Long-Term Care Needs

There are 4 ways to pay for your long-term care needs. You can:

Self Pay

In other words, do nothing for planning and if you need long-term care, spend down your income and the assets you worked so long and hard for.

(Including your home, but we’ll get to that in a minute..)

What, John?

(Yes, we will get to how you can lose your home in this process.)

Unless you are rich, you’ll ultimately become destitute and qualify for MassHealth.

Does this sound good? It doesn’t, and it gets worse.

MassHealth will then call the shots on your health care needs. If this is what you want for yourself and loved ones, I wish you good luck.

Why is that? Well, simply, they are paying for your long-term care. Your doctor and staff will be limited by MassHealth’s rules. Is this what you want?

(Oh yeah…and they still go after any remaining assets upon your death.)

Establish An Irrevocable Trust

A lawyer can help you establish this. Essentially the trust becomes a separate entity. In general terms, you would title your assets in the name of the trust. If you need long-term care services, MassHealth can’t touch them (because they don’t necessarily belong to you), and you would qualify for MassHealth. Yes, the drawback is MassHealth will call the shots on your health care needs. (They are paying the bills, right, so some person whom you never met, will determine your needs. Is that what you want?)

While a trust can prevent your assets from being used for long-term care, the trust is irrevocable. So, once it’s set up, you lose control of the assets. We urge caution here and the consultation of a qualified attorney if this is how you want to proceed. Just like greedy insurance agents, there are lawyers who want to set up an irrevocable trust to set one up. Consult one who puts your best interest first.

Purchase An Asset-Linked Long-Term Care Insurance Policy

These asset-linked or hybrid long-term care insurance policies are becoming more and more popular as the “use-it-or-lose-it” stigma wears on traditional long-term care insurance policies. However, they leave Massachusetts residents with a glaring gap that we will discuss next. In terms of complete protection, these plans do leave you exposed.

Purchase A Traditional Long-Term Care Insurance Policy

While these are less common, they (in our opinion) provide the best protection of your assets. They still offer great benefits, even better than those offered by asset-long-term care insurance policies. If designed correctly, you don’t have that “use-it-or-lose-it” stigma as you think. We will discuss these policies next. They will protect your home and other assets. They will give your spouse and family peace-of-mind.

Isn’t that what you want?

How You Can Lose Your Assets. Easy.

Let’s say you decide to either self-pay, establish a trust, or purchase an asset-long- term care insurance policy. Probably in all cases, even in the case of the asset-based long-term care insurance policy, MassHealth will have to pay something.

term care insurance policy. Probably in all cases, even in the case of the asset-based long-term care insurance policy, MassHealth will have to pay something.

Yep, it’s true. Not certain at 100%, but likely.

Not to get off a tangent, however, depending on your level of custodial needs, MassHealth may have to pay for something.

Here is something many people do not realize: MassHealth is not a free service. Sure, they are paying for long-term care services now, but they want their money back! And, they’ll do this at your death. Anything they spend on you for your long-term care and custodial needs, they will want the money back.

How is that, you ask? From a process called Estate Recovery.

But, John, I won’t have anything left, you say. Actually, you will. While there are many assets that are not countable towards the MassHealth spend down process, these assets are now off limits. MassHealth will place a claim on your assets in your estate upon your death to pay back their services.

What?!?!?!

You did not know that? A lot of people don’t, until it is too late. Fortunately, there are ways to mitigate estate recovery, and we will discuss those soon. But first, we discuss the estate recovery process in more detail.

What Is Estate Recovery?

When a recipient of MassHealth long-term care services dies, MassHealth has the authority to make a claim on the deceased recipient’s assets and estate in an amount of the total paid out on the recipient’s behalf.

Let’s say MassHealth spent $200,000 on your nursing home care. It wants $200,000 back. So, it places a lien or claim on your remaining assets.

It is a federal requirement that the MassHealth program does this so as to reduce the costs associated with the program.

Wouldn’t you? It’s not that the state “stinks” or is lousy. Every state has these rules. Nothing is free. I am sure if you paid for someone’s care out of your savings, you’d want to be paid back, right?

A claim can be made to pay for:

- long-term care services

- prescription drugs

- hospital expenses

- anything associated with MassHealth paying

You are subject to estate recovery process if you are:

- age 55 or older at time of death, and

- received MassHealth benefits after 10/1/1993

So, that means YOU!

Here is the kicker: assets that were exempt (i.e., non-countable) for the MassHealth eligibility process are now considered non-exempt (i.e they are COUNTABLE) for the estate recovery process. Assets include:

- household furniture

- bank accounts

- saving accounts

- your car

- your personal belongings (such as family heirlooms)

This means the value of your remaining assets can be used to pay for anything MassHealth paid on your behalf. You may not think you’ll have anything, but you would have some value – jewelry, cars, etc.

Your Home Is Treated Differently, Though

Notice we did not discuss your home. Massachusetts is one of the few states – really the only one – which includes the value of your home in the spend-down process.

You heard us right.

Remember that spend-down to the $2,000 asset base to qualify for MassHealth? Your home is included.

Yes. I know you don’t think that, but it is.

So, if you haven’t prepared for your long-term care needs, and you just think you’ll pay your way until MassHealth kicks in, Massachusetts will say, “Hey, don’t forget to sell your home to pay for your care.” Sure, there are some stipulations. For example, the state can’t kick your spouse out of the house if he or she is living there. We discuss those exemptions further down in the article.

So, if you haven’t prepared for your long-term care needs, and you just think you’ll pay your way until MassHealth kicks in, Massachusetts will say, “Hey, don’t forget to sell your home to pay for your care.” Sure, there are some stipulations. For example, the state can’t kick your spouse out of the house if he or she is living there. We discuss those exemptions further down in the article.

But, if you are alone or your children live with you (and independent), they will force you to sell your home.

In other words, if you need long-term care services paid by the state, MassHealth can force you to sell your home if certain requirements are met. Those proceeds are then used to pay for your long-term care needs.

There Is A Way To Stop This!

So, what you just read must have you down. Yes, in Massachusetts the value of your home can be used to pay for your long-term care needs on the front end.

If it is not, then the state can make a claim on your home to reimburse MassHealth for money paid on your behalf during the estate recovery process.

While many states keep the home off limits during the spend-down process (and may require selling during the estate recovery process), in Massachusetts the home is part of the spend-down process. That means you may have to sell your home in order to have MassHealth pay for your long-term care.

But, there are a couple of exemptions to this.

You WON’T have to sell your home IF your home has less than $750,000 of home equity AND any of the following applies: (Be careful of the “AND.” If you don’t qualify for anything below, then homes with less than $750,000 of equity WILL have to be sold!)

♦you intend to return to the home

♦one or all of the following people live in your home:

- spouse

- child under the age of 21

- disabled or blind child of any age

- a child who cared for you for at least 2 years before you moved into a nursing home

- a sibling who has an equity interest in the home

- dependent relative

♦you have a qualified long-term care insurance policy

The spend-down process will include your home if these exceptions do not exist. Even if the spend-down process excludes your home, Massachusetts can, and will, make a claim of your home upon your death to pay for any long-term care services paid by MassHealth. (During the estate recovery process.)

There’s no way around it, unless…

…you have a qualified long-term care insurance policy. Your home won’t be subject to the spend-down process or estate recovery.

Yes, A Long-Term Care Insurance Policy Works In Massachusetts!

Do you see the theme here? In Massachusetts, you can avoid this mess, save your home, and many other valuables by purchasing a qualified long-term care insurance policy.

If you don’t believe us, here is the language written in the state’s legislature as summarized:

No claim for costs of a nursing facility or other long-term care services shall be made . . . if the individual receiving medical assistance was permanently institutionalized, had notified the division that the individual had no intention to return home and, on the date of admission to the nursing facility or other medical institution, had long-term care insurance that, when purchased, met the requirements of 211 CMR 65.00.

Here is a link to the verbiage.

Not just any long-term care insurance policy will work, though. The policy has to meet the state’s requirements as defined in 211 CMR 65.00. What are these requirements? We discuss them next.

What Is A Qualified Long-Term Care Insurance Policy In Massachusetts?

Here are the provisions which make a long-term care insurance policy qualified in Massachusetts. The policy…

- benefit trigger is the insured’s inability to perform two or more ADLs due to loss of functional capacity or severe cognitive impairment.

- cannot condition receipt of any services on any standard of medical necessity (except medical services provided by licensed medical professionals).

- cannot condition benefits on a prior hospitalization or prior receipt of long-term care services.

- must be issued as guaranteed renewable or noncancelable.

- cannot condition receipt of benefits on a requirement that the insured must make “steady improvement” or have “recuperative potential” (or words of similar import).

- cannot include an elimination period of more than 365 days.

Additionally, the insurer must make available at the time of application an option for you to…

- add inflation-adjusted benefits.

- purchase a nonforfeiture benefit.

Before you go any further, those asset-long-term care insurance policies do not qualify under 211 CMR 65.00. Massachusetts residents need a traditional long-term care insurance policy that meets the requirements of 211 CMR 65.00.

That’s right, those asset-based or life insurance with LTC riders do not qualify for the exemption

Myths Of Long-Term Care Insurance

Many people, including agents and the industry, discredit traditional long-term care insurance policies. The main stigma is the “lose or use it” structure of long-term care insurance.

However, people need to see what long-term care insurance is. It is insurance.

When you have insurance, more often than not, the carrier wins and you lose. What do I mean by that? Well, it’s insurance! Think of your homeowners and car insurance. Do you hope to use it? No! It’s the safety net in case you need to make a claim.

The good news is that the remaining carriers in the long-term care insurance market have remained steady. Premiums have leveled. Additionally, many carriers have introduced “return-of-premium” options if you don’t need long-term care insurance. No more “lose-it-or-use-it” stigma.

That’s great, but I beg to differ. Think about what this insurance is going to do. Not only will it protect your home on the front-end, but also your assets on the back-end upon your death. If the value of your long-term care insurance is $500,000, then $500,000 of your assets are exempt (excluding your home) from estate recovery, even if you need MassHealth assistance. Truth!

You can’t say that about asset-based or life-LTC insurance. I can almost guarantee if you use up your benefit from an asset-based insurance option, MassHealth will implement its spend-down rules.

Now You Know Massachusetts Residents Can Protect Their Home With A Long-Term Care Insurance Policy

We hope this article educated you on why Massachusetts residents need a traditional long-term care insurance policy. None of us want to lose our assets and especially our home to long-term care services. The good news is that Massachusetts residents have a way to mitigate this event through the purchase of a qualified long-term care insurance policy as defined in 211 CMR 65.00. Remember, even though they are useful, asset-backed or hybrid long-term care insurance policies do not qualify.

If you don’t know where to start or what is even the right policy for your needs and budget, we can help. We have certified long-term care specialists on our staff who can customize and design a plan. We go through all the steps and work with you to a final plan, only selecting the one that meets your goals, needs, protection, and budget.

Feel free to contact us or use the form below. We would be very happy to help you with this important coverage.

Learn More

Are you interested in learning more about the information in this article? Please fill out the form below, and we will email you additional information or give you a call. We always work in your best interest. By entering your information, you are providing your express consent that My Family Life Insurance may contact you via e-mails, SMS, phone calls, or prerecorded messages at any phone number(s) that you provide, even if the number is a wireless number or on any federal or state do-not-call list. Additionally, you understand that calls may be placed using automated technology, and that consent is not a requirement for purchase. Your information will NOT be sold and will remain private. However, you may opt out at any time. We respect your privacy first and foremost. By contacting us, you agree to receive text messages from our number (800) 645-9841. If you no longer wish to receive text messages, you may opt out at any time by replying "STOP".