2 Solid Ways To Sell Your Term Life Insurance Policy | We Discuss The Details And If This Transaction Makes Sense

Updated: April 12, 2024 at 9:38 am

Did you know you can sell your term life insurance policy to an unrelated third party?

Did you know you can sell your term life insurance policy to an unrelated third party?

It is true.

However, like anything, there are advantages and disadvantages to selling your term life insurance policy.

In this guide, we will discuss the process of selling your term life insurance policy. We will also discuss what you can expect, whether it is a good idea to do so, and other options available.

Here is what we will discuss:

- What Is A Term Life Insurance?

- Requirements To Sell Your Term Life Policy

- 2 Ways You Can Sell Your Term Life Insurance

- 5 Steps For Selling Your Term Life Insurance Policy

- Tax Implications Of Selling Your Term Life Insurance Policy

- When Does Selling Your Term Life Insurance Policy Make Sense?

- When You Should Keep Your Term Life Insurance Policy

- FAQs About Selling Your Term Life Insurance Policy

- Final Thoughts About Selling Your Term Life Insurance Policy

Let’s jump in and give a brief overview of term life insurance. We will contrast term life with other types of life insurance available to sell, including whole life and universal life policies.

What Is Term Life Insurance?

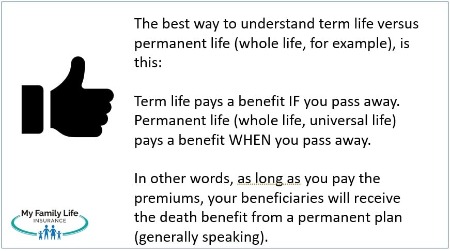

Term life insurance is one of 3 main types of life insurance available. Term life exists for a “term”, which is a set, fixed time period usually denoted in years. For example, you can purchase a 10-year term, a 30-year term, etc. Some carriers even offer a 40-year term! Moreover, a few carriers even offer 1-year annual renewable term life policies.

During the term period, the life insurance premiums remain the same.

If you pass away during the term period, your beneficiary receives the death benefit. If you don’t pass away, then your beneficiaries receive nothing. This is why many agents and brokers refer to term life insurance as “temporary” insurance because it lasts only a fixed number of years. (Technically, you can renew your term life insurance policy after the term period ends. However, your rates increase every year.)

What Is A Permanent Life Insurance Policy?

We just discussed how term life policies pay the death benefit if the insured passes away during the term period. Conversely, permanent life insurance policies are designed to last one’s lifetime and payout whenever the insured passes away. Hence, the name “permanent” because these types of policies are designed to last the insured’s lifetime.

passes away during the term period. Conversely, permanent life insurance policies are designed to last one’s lifetime and payout whenever the insured passes away. Hence, the name “permanent” because these types of policies are designed to last the insured’s lifetime.

Two main types of permanent policies exist: whole life policies and universal life policies. Each of these types of policies contains cash value. Cash value (also known as cash surrender value because it is the amount of money you’ll receive if you terminate your policy) is like a savings account. (But, don’t confuse it with a bank savings account because these aren’t the same.)

They are also permanent in nature. In other words, permanent policies pay the policy’s face value no matter when the insured passes away. That can be next week or when the insured is 95 years old. As we will discuss in this article, this permanency is a main component in the selling of your term life insurance policy to a third party.

Selling your term life insurance policy isn’t like selling books or widgets on Amazon. Certain requirements have to be met. Let’s discuss these requirements next.

Requirements To Sell Your Term Life Insurance Policy

You can sell your term life insurance policy on a secondary market, which we will describe further in the next section. However, not just anyone or any policy qualifies. In general, the following requirements exist for you to sell your term life insurance policy.

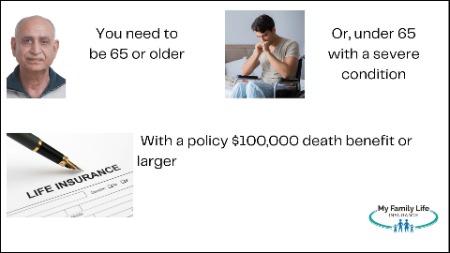

- The insured / policy owner must be age 65 or greater

- Or, under 65 if faced with a severe, chronic illness or terminal illness

- The policy’s death benefit amount must be $100,000 or greater

- The policy must be a permanent policy like whole life insurance or universal life

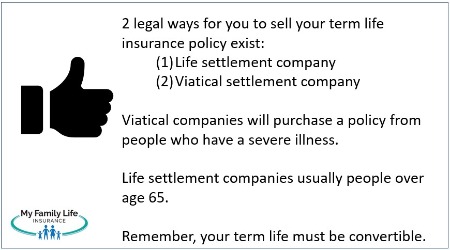

- Term life insurance policies will qualify as long as the policy is convertible to a permanent policy

Let’s briefly discuss the convertibility feature on term life insurance policies.

Some term life insurance policies have a conversion rider which allows the insured / owner to convert the policy to a permanent policy.

insured / owner to convert the policy to a permanent policy.

This is a valuable option and a requirement to sell your term life insurance policy. If you have a term life insurance policy, you’ll want to check and see if your policy has the convertibility feature.

If not, then your term policy won’t qualify.

John, why are people over the age of 65 or those really sick a requirement?

That is a good question. We can answer that in our next section, discussing the 2 ways you can sell your term life insurance policy.

2 Ways You Can Sell Your Term Life Insurance Policy

There are 2 solid, legal ways you can sell your term life insurance policy.

There are 2 solid, legal ways you can sell your term life insurance policy.

(1) Life Settlement Company

(2) Viatical Settlement Company

These are secondary market options. You are selling your life insurance policy to a third-party investor. Certain investors like purchasing life insurance policies because of the guaranteed death benefit amount. Think about it. Our deaths are guaranteed (as Ben Franklin said). As long as these investors continue to make premium payments, they receive a guaranteed dollar death benefit.

Life settlement and viatical settlement options work in a similar way. The main difference is that viatical settlement companies purchase policies from people who are terminally or chronically ill. Life settlement companies, on the other hand, purchase policies from anyone, over the age of 65, and not necessarily terminally or chronically ill.

What, John? This all doesn’t sound right and is morbid, in fact!

I know what you mean. However, life settlement transactions are completely legal. Many states regulate life settlement companies. Additionally, many life settlement companies belong to the Life Insurance Settlement Association (LISA).

However, you touch on an important point. These companies do not want younger individuals who are healthy. You see, life insurance policies are extremely valuable. These settlement companies buy your life policy and become the new owner. You are still the insured. However, upon your passing, the settlement company receives the death benefit. Their profit is the difference between the death benefit received and the price they paid for your policy + any premium payments.

Example Of A Term Life Insurance Sale

For example, let’s say Joe, age 68, has a term life insurance policy with a convertibility feature that ends at age 70. He has a $500,000 policy and has paid $75,000 in total premiums.

The life settlement company buys his policy for $300,000. The life settlement provider becomes the new owner. They convert the term life policy to a permanent life policy.

As the new owner, the life settlement company pays the monthly premiums and any future premiums. They pay another $25,000 in premiums when Joe passes away. Upon Joe’s passing, they receive the $500,000. Their profit is $175,000 ($500,000 – ($300,000 + $25,000)).

Again, life settlement and viatical settlement companies are legal. They may not be your best option (more on that later in the article), but they are a legal way of disposing your term life insurance policy.

Let’s discuss what life settlement companies look for in a policy.

Life Settlement Requirements

We discussed briefly the requirements of selling your term life insurance policy. Let’s get into the specifics.

Let’s get into the specifics.

Life settlement and viatical companies only want people over the age of 65 and/or those who are chronically or terminally ill. The reason, as we discussed, is the profit. These companies will be the new owner of your policy and resume premium payments. They pay a lump sum cash payment to you and want to minimize the continued monthly premiums as much as they can. (So, they can maximize their profit.)

So, these companies will really want to know your health. They will order your medical records to confirm the severity of your health conditions. This is why they really don’t want people in good health. Your life expectancy affects their cash offer. They want older people or those with severe health conditions in order to maximize their profit and their rate of return. In other words, the lower the insured’s life expectancy, the sooner they can realize a profit and a higher rate of return.

Additionally, these companies want permanent policies or those term policies with a conversion rider/feature.

5 Steps To Selling Your Term Life Insurance Policy

5 Steps To Selling Your Term Life Insurance Policy

If you are interested in selling your term life insurance policy, please read on. Here are 5 steps to selling your term life insurance policy.

(1) Contact us – that is right. We are an independent broker and work with many life settlement companies. We can have them review your term life insurance policy to make sure it is sellable.

(2) Let us know your health status and medical information – this is an important component of the life settlement process.

(3) We reach out to many life settlement companies and compare the best offer. It could take up to a week to hear back from all options.

(4) Provide medical information, documentation, etc. Usually, the life settlement company will obtain that information on your behalf.

(5) Transfer ownership to the life settlement company and receive your cash payout

The process of selling your term life insurance policy is similar to that when you applied for term life insurance. However, life settlement and viatical companies aren’t going to require a paramedical exam or any of that. They really want your medical information to determine your life expectancy.

The whole process could take a couple of weeks to a month, depending on how soon the life settlement company receives your medical information.

As we discussed before, we will help you consider all options available to you.

What Are The Tax Implications Of Selling Your Term Life Insurance Policy?

This is an often overlooked area for people looking to sell their term life insurance policy.

The IRS taxes any gain on the sale of your term life insurance policy. Here is a very easy example, which excludes any cash value implications as well.

Rebecca has a convertible term life insurance policy with a death benefit amount of $250,000. She’s paid $6,000 so far. She sells her term policy to a life settlement provider for $100,000 cash. Her gain is $94,000, subject to ordinary income tax ($100,000 – $6,000).

Note: the IRS may tax sellers of a life insurance policy with a capital gains tax. Please consult a tax advisor for more information.

My recommendation is for you to consult a tax advisor before entering into a life settlement transaction. The reason, as I will explain further in the article, is that other, viable, non-taxable options exist.

When Does Selling Your Term Life Insurance Policy Make Sense?

As you can tell, selling your life insurance policy provides a cash payout. That is nice, right? You can use this money for whatever you want.

A few cases exist where selling your term life insurance policy makes sense. These situations include, but are not limited to:

- long-term care situations

- pay for medical bills or medical expenses

- you just don’t need the life insurance anymore

- premiums are now too expensive for your situation

- you already have critical illness or long-term care insurance

- money is really tight

- your beneficiaries don’t need the death benefit anymore

Contact us if you’d like to see if your situation warrants a life insurance sale. We only work in your best interests and communicate all the options available to you.

When Should You Keep Your Life Insurance Policy

I just outlined several scenarios where selling your term life insurance policy might make sense.

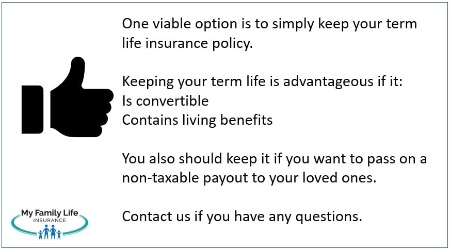

However, in my professional opinion, I think nearly all cases, you should keep your term life insurance policy (or any life insurance policy for that matter).

For one thing, the death benefit is a non-taxable cash payment to your beneficiaries. It is one of the few, remaining ways to pass wealth to a loved one without government tax interference.

beneficiaries. It is one of the few, remaining ways to pass wealth to a loved one without government tax interference.

Additionally, many term life insurance policies nowadays have living benefits. What are living benefits? They allow you to accelerate the death benefit sooner if you:

- are diagnosed with a terminal illness,

- are diagnosed with a covered critical illness like cancer, or

- need assisted living or nursing home care

By converting your term life insurance plan into a permanent plan, you just created a solid safety net in case of these scenarios. Moreover, these are non-taxable distributions. Conversely, selling your term life insurance subjects you to tax.

Check your policy if you have an accelerated death benefit rider. This is another, more common name for living benefits.

If you do have living benefits on your term life policy, you should consider keeping the policy rather than selling it.

Of course, every situation is different. Please contact us with any questions you have.

FAQs About Selling Your Term Life Insurance Policy

We compiled a list of frequently asked questions about selling your term life insurance policy.

Can I Sell My Term Life Insurance Policy For Cash?

Yes, you can sell your term life insurance policy for a lump sum cash payout.

Is It Legal To Sell My Term Life Policy?

It is legal to sell your term life insurance policy to a viatical settlement or a life settlement company. Your state insurance department regulates these companies.

However, as we discussed, you want to make sure selling your policy is in YOUR best interests. Keeping your policy might be the best option.

How Much Do I Get For My Policy?

Other websites say 20% to 30% of your policy’s face value / death benefit. However, the amount really depends. It depends on several factors, namely your age, health situation, and estimated life expectancy.

Whom Do I Speak To About Selling My Policy?

Us! We work with over 10 settlement companies. If you work with us, we will provide the details and your situation to the 10 companies. They will make offers based on your situation. We pick the best one.

However, by working with us, we can give you all the viable options that are available to you. You can pick the best option that meets your needs. Sometimes, that option is just sticking with your policy.

What Is The Difference Between Selling and Surrendering My Life Insurance Policy?

There is a major difference. In this article, we discussed selling your life insurance policy.

Surrendering your life insurance policy essentially means you cancel it. The terminology “surrendering” is more common with a whole life insurance policy or universal life insurance policy. When you “surrender”, you receive the policy’s cash surrender value back to you. Recall that the cash surrender value is the cash that accumulates within a permanent policy.

Can I Get My Life Insurance Back Or My Money Back If I Change My Mind?

I know other websites say otherwise, but really, when you sign your life insurance over to a viatical or life settlement company, there is no recouping your life insurance or getting your money back.

If you are seriously considering selling your term life insurance policy, you need to consider all of your options. As we discussed, better options may exist.

Final Thoughts About Selling Your Term Life Insurance Policy

We went through a lot of information in this article. Yes, you can sell your term life insurance policy. In general, if you want to sell your term life insurance policy, you:

- need to be over the age of 65 or under 65 if you have severe health conditions

- have a policy with a death benefit of $100,000 or higher

- have a policy that has a conversion option

As we discussed, there are cases where you want to sell your term life insurance policy and other cases where you will want to keep it.

Do you have questions or see if you qualify? Contact us or use the form below. Selling your term life insurance policy requires a commitment from an independent broker who holds a duty of care and your best interests first and foremost. We at My Family Life do just that.

We will provide your options and discuss if it makes sense for you to sell your policy. If it does, we work with many life settlement companies that will provide cash offers for your policy. We will take you through each step of the process.

Of course, there is never a risk to working with us. If you don’t want our help, just let us know anytime. You can always reach back out to us if your situation or needs change.

Learn More

Are you interested in learning more about the information in this article? Please fill out the form below, and we will email you additional information or give you a call. We always work in your best interest. By entering your information, you are providing your express consent that My Family Life Insurance may contact you via e-mails, SMS, phone calls, or prerecorded messages at any phone number(s) that you provide, even if the number is a wireless number or on any federal or state do-not-call list. Additionally, you understand that calls may be placed using automated technology, and that consent is not a requirement for purchase. Your information will NOT be sold and will remain private. However, you may opt out at any time. We respect your privacy first and foremost. By contacting us, you agree to receive text messages from our number (800) 645-9841. If you no longer wish to receive text messages, you may opt out at any time by replying "STOP".