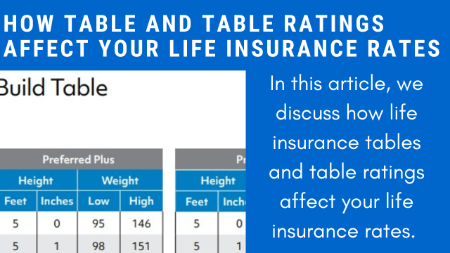

We aren’t talking about kitchen tables. In your search for affordable life insurance, you may have heard of the terms “life insurance tables” or “table rating”.

We aren’t talking about kitchen tables. In your search for affordable life insurance, you may have heard of the terms “life insurance tables” or “table rating”.

Or, maybe you applied for life insurance, and the life insurance company offered a “table rating”. You probably have no idea what this means.

Yeah, John. I am confused. They want to charge me a higher premium!

No problem. In this article, we discuss the importance of understanding life insurance tables and table ratings (hint: it saves you money!).

Did you know that people with Huntington’s Disease can obtain life insurance?

Did you know that people with Huntington’s Disease can obtain life insurance? Did you know you can sell your term life insurance policy to an unrelated third party?

Did you know you can sell your term life insurance policy to an unrelated third party? If you are like most people, you probably don’t think about how your driving record affects your life insurance rates.

If you are like most people, you probably don’t think about how your driving record affects your life insurance rates.