What’s The Life Insurance LexisNexis Risk Classifier Score Really About?

Updated: April 12, 2024 at 9:39 am

I guaranteed you’ve never heard of the LexisNexis Risk Classifier Score. Yet, it plays an important role in insurance.

plays an important role in insurance.

John, this sounds like it belongs in outer space, you say.

Ha. No. The risk classifier score is simply a consumer report that many insurance companies use to assess risk. In fact, a majority of life insurance carriers use it during the underwriting process.

This is why you need to know more about it because it can make an impact on the insurance approval decision.

Additionally, more and more life insurance carriers are using the LexisNexis Risk Classifier Score in their underwriting analysis and decision.

In this article, we will discuss:

- Who Is LexisNexis?

- What Is The Risk Classifier Score?

- Details Of The Risk Classifier Score

- Demystifying Of LexisNexis For Underwriting

- What If You Get A Bad Score?

- Now You Know LexisNexis Risk Classifier Score’s Role In Underwriting

Let’s jump in and discuss who (and what) is LexisNexis.

Who Is LexisNexis?

Contrary to what the name suggests, LexisNexis is not a planet or a solar system.

Contrary to what the name suggests, LexisNexis is not a planet or a solar system.

LexisNexis is actually LexisNexis® Risk Solutions, a global data analytics company that provides data services, research, analytics, and predictive and fraud information for many industries.

The life insurance industry is one of the many industries LexisNexis helps and supports.

How do they help the life insurance industry? They assist carriers and underwriters with applicant data information, which speeds up the underwriting process. They do this with a “risk classifier score”.

As we will discuss further, the risk classifier score helps with accelerated and predictive underwriting, which is a common underwriting process with many life insurance carriers.

Let’s talk about the LexisNexis Risk Classifier Score next.

What Is The LexisNexis Risk Classifier Score?

Have you heard of:

- No-exam underwriting,

- Accelerated underwriting,

- EZ-underwriting, or…

…something like this?

Yes, you say,

These types of underwriting aim to remove the paramedical exam from the life insurance underwriting process. Typically, the life insurance underwriting process contains a paramedical exam which includes a:

- Height/weight check

- Blood pressure check

- Pulse

- Health questions

- Blood sample

- Urine sample

- And possibly other information depending on your age and/or death benefit amount

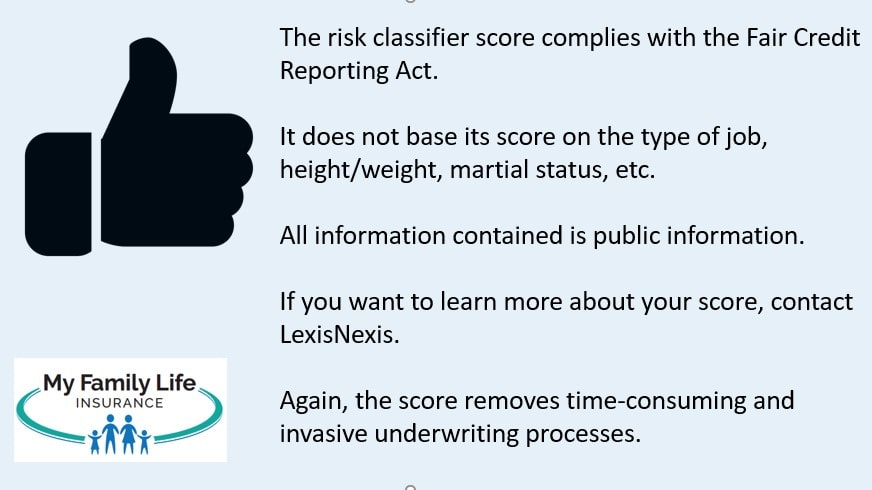

However, nowadays, many carriers want to remove the paramedical exam from the underwriting process. Why? It’s time-consuming, costly, and invasive.

More importantly, they can get decisions faster and people insured much sooner. Traditionally, the life insurance underwriting process could take months!

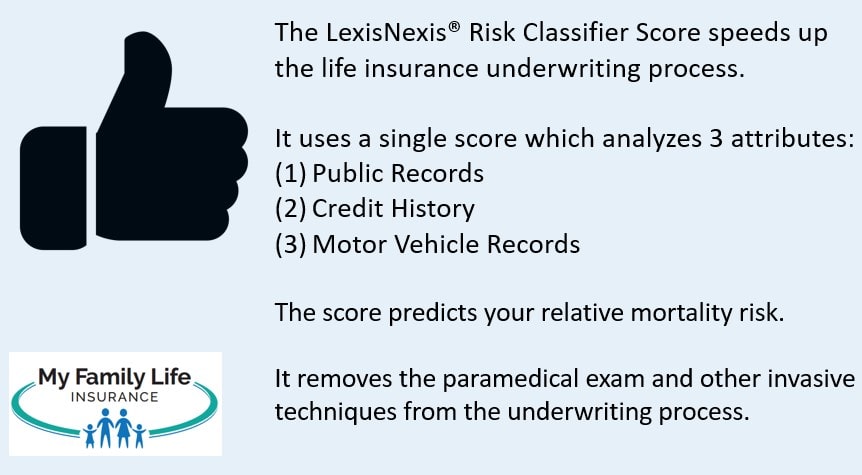

“The importance of the LexisNexis Risk Classifier Score is that it speeds up the life insurance underwriting process.”

Well, that is great, John, you say. However, how do they get the data they need to make an underwriting decision?

Good question. So, underwriters still look at your:

- MIB report, and

- Prescription drug history

However, they have introduced the risk classifier score that accelerates the underwriting process.

The risk classifier score gives underwriters (more so in the life insurance industry, but others as well) an idea of your relative mortality based on a confluence of factors.

It’s all public records and compliant with the Fair Credit Reporting Act. So, no worries there.

Let’s talk about those factors next and dive into the risk classifier score in more detail.

The Details Of The LexisNexis Risk Classifier Score

The LexisNexis Risk Classifier Score provides a single score, ranging from 200 to 997, based on the following categories:

- Public Records

- Motor Vehicle Records (MVR)

- Credit Records

It looks at the positive attributes and negative attributes of these 3 categories and then provides the score. The underwriters then use that score to assess your relative mortality risk.

So, John, it takes all of that information and then can predict, on average, when I will pass away?

Yes, it predicts your relative mortality. This is an important point, and we will discuss this further. If you are a 24-year old African American woman, your score measures against other 24-year old African American women.

This is cockamamie, you exclaim!

Well, it seems like it, but it is not. One of the measures in the score is the number of credit cards a person has. Generally speaking, the more cards one has, the longer the mortality.

Now, on the surface, that may not make sense. However, think about this more. People who don’t have any credit cards are likely in tough situations. They may have direct express social security cards or on Medicaid. Do you know these people? Unfortunately, these people (supported through the data in LexisNexis) have lower mortality.

Do you see how that works?

If you think it can’t, Munich RE, one of the largest insurance companies in the world, validated the LexisNexis Risk Classifier Score for its underwriting purposes.

Before we get into the details of the attributes, it is important to note that the risk classifier score complies with the Fair Credit Reporting Act (FCRA). We will discuss this more in our “Demystifying…” section.

Let’s go into these 3 attributes in more detail.

Public Records

The LexisNexis Risk Classifier Score includes public records. These records include, but are not limited to:

- Property ownership

- Felonies and convictions

- Professional licensing

- Bankruptcies and Liens

- And more

Positive attributes here improve your relative mortality score whereas negative attributes drop your score.

Motor Vehicle Records

Motor vehicle records are also part of the attributes.

While you may think that accidents are the only factor, they are not.

Not having a driver’s license also plays a part.

Credit Records

Credit records also play a part in the score.

John, my FICO score is great, you say.

Great, but this has nothing to do with your credit score.

Your credit score deals with your ability to pay a loan back. It looks at your creditworthiness.

However, the credit records align with your mortality risk.

As we indicated before, the number of credit cards one holds is an example.

With your FICO score, that’s also the case, but it relates to your credit score and creditworthiness. In most cases, too many credit cards negatively impact your FICO score.

Other factors in this area include, but are not limited to:

- Collections

- Payment history

- Credit history

Demystifying The LexisNexis Risk Classifier Score

As we mentioned earlier, the LexisNexis Risk Classifier Score speeds up the underwriting process by analyzing public records. It then assigns a score that measures your relative mortality risk.

Also, as we mentioned, LexisNexis complies with FCRA.

Here’s what it does not do.

It does not compare you to other people of different ages and ethnicities. We provided an example earlier.

It follows the FCRA, so it does not report based on religion, gender, job, disability, etc.

It also does not factor in social media profiles, etc.

Again, it just simply takes the 3 attributes we discussed earlier, compiles that information, analyzes against other people of similar characteristics of age, gender, and ethnicity, and provides a relative mortality score.

The higher the score, the better.

OK, John, but what happens if I obtain a bad score?

We discuss that next.

What If You Receive A Bad Score?

Let’s say you apply for life insurance at preferred rates. But, you are approved at standard rates (which isn’t bad at all, either).

You’ll receive something like this if you receive a different outcome than what you applied for:

“Our offer is based on the risk classifier score which is a mortality score derived from, but is not limited to public records, driving records, court records, and property records. Factors include payment behavior and # of open accounts with a high % of balance to credit limit.

If your client would like a detailed report outlining the exact attributes which adversely impacted their score, please have them contact:

Lexis Nexis Consumer Center

Attn: Life Report

P.O. Box 105108

Atlanta, Georgia 30348-5108

Or they can call and ask for their Life Report by dialing:

888-497-9215.”

So, you would just contact LexisNexis at the information above.

They will then send you your risk classifier score report with up to 4 reasons why your score negatively impacted the underwriting decision.

Now You Know How The LexisNexis Risk Classifier Score Impact Life Insurance Underwriting

We hope you learned more about the LexisNexis Risk Classifier Score and how it impacts life insurance underwriting.

As we mentioned, if you apply for any type of life insurance with accelerated underwriting, the carrier likely uses the LexisNexis Risk Classifier Score to complete the underwriting process.

The LexisNexis Risk Classifier Score predicts relative mortality. It aids in the life insurance underwriting process.

Do you have any questions about the risk classifier score? We are happy to answer them.

Feel free to contact us or use the form below.

As with everything we do, we only place you and your interests first and foremost.

Learn More

Are you interested in learning more about the information in this article? Please fill out the form below, and we will email you additional information or give you a call. We always work in your best interest. By entering your information, you are providing your express consent that My Family Life Insurance may contact you via e-mails, SMS, phone calls, or prerecorded messages at any phone number(s) that you provide, even if the number is a wireless number or on any federal or state do-not-call list. Additionally, you understand that calls may be placed using automated technology, and that consent is not a requirement for purchase. Your information will NOT be sold and will remain private. However, you may opt out at any time. We respect your privacy first and foremost. By contacting us, you agree to receive text messages from our number (800) 645-9841. If you no longer wish to receive text messages, you may opt out at any time by replying "STOP".