Disability Insurance Underwriting: What You Need To Know To Get Approved Today!

Updated: April 12, 2024 at 9:39 am

In my opinion, there is no disputing how important disability insurance is. Just get on www.gofundme.com to see the pain many people and families are experiencing. The solution to many of these situations, simply, would have been a comprehensive, affordable disability insurance policy. Their lives could have been so much better. However, if you need disability insurance, you need to know about disability insurance underwriting first. Knowing how underwriting works is the first step to obtaining a disability insurance policy.

In my opinion, there is no disputing how important disability insurance is. Just get on www.gofundme.com to see the pain many people and families are experiencing. The solution to many of these situations, simply, would have been a comprehensive, affordable disability insurance policy. Their lives could have been so much better. However, if you need disability insurance, you need to know about disability insurance underwriting first. Knowing how underwriting works is the first step to obtaining a disability insurance policy.

We receive phone calls from many people who are interested in disability insurance. However, they are unaware of how their background and health affect their chances of obtaining a policy. Misunderstandings abound.

In this article, we discuss the important aspects of disability insurance underwriting. We will inform, clarify, and set expectations so you can get approved today.

- What is underwriting?

- How disability insurance is different?

- Underwriting fails and pitfalls

- Can the carrier remove exclusions?

- Why you need to accept a modified policy

- Other options if you can’t get approved

- Now you know how underwriting works so you can be approved today

Let’s get right into it and discuss underwriting.

What Is Underwriting?

Underwriting is simply the process of reviewing and analyzing a specific risk before insuring or undertaking that risk. Any type of insurance goes through underwriting – a mortgage application, auto loans, investment accounts, and, of course, insurance. The underwriter – the person skilled in analyzing the risk – reviews your situation. Specific to disability insurance underwriting, the underwriter will review your:

- health history

- occupation

- income

- medication

- “fun” activities

- and really, anything else he or she deems material to a decision

The risk, of course, that underwriters measure and analyze, is the risk of a disability happening to you

We discuss each of the above next. First, though, let me address something that needs saying.

The best time to purchase disability insurance is right now. You are the youngest and (probably) the healthiest you will ever be.

Additionally, once you are insured, disability insurance carriers can’t go back to their underwriting and change your plan. For example, let’s say you have a disability insurance policy. Five years later, you are diagnosed with heart disease, cancer, or depression. These situations are all covered if you make a claim.

The time to purchase disability insurance is right now.

Now, let’s discuss disability insurance underwriting in more detail.

Disability Insurance Underwriting – How Is It Different?

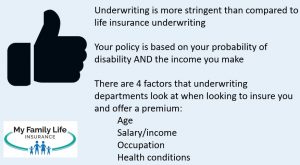

In our opinion, disability insurance underwriting is more stringent than other types of personal insurance, including life insurance and health insurance. Why? The underwriter and the carrier are insuring two things:

(1) your income

(2) your likelihood of disability

Additionally, the factors we described previously drive the underwriter’s decision.

Now, I know what you are thinking. “John, there is no way I am going to be disabled.”

As I have said previously, if you know your future, you should not be reading this article. You should play the lottery and win money.

But, you are reading this article…

Do you see what I mean?

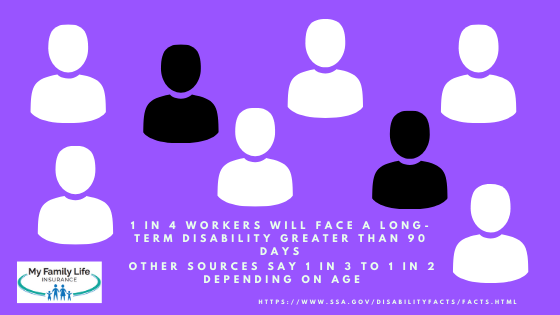

The fact is, 1 out of 4 workers, in general, will face a disability lasting greater than 90 days. That’s 3 months. Do you have enough money to survive that? Moreover, if a disability lasted 13 months, do you have enough money to survive that timeframe? Or 2 years? Or 5 years? Or more?

The fact is, 1 out of 4 workers, in general, will face a disability lasting greater than 90 days. That’s 3 months. Do you have enough money to survive that? Moreover, if a disability lasted 13 months, do you have enough money to survive that timeframe? Or 2 years? Or 5 years? Or more?

Moreover, this statistic isn’t coming from me. It’s from the Social Security Administration.

As we have stated elsewhere in articles, this probability is worse than an unexpected death and even passing away from cancer.

If you understand how the underwriting works for disability insurance, you will be better educated and informed come time for the application.

Before we get into the specifics of disability insurance underwriting, let’s discuss how pre-existing conditions play into the underwriting decision.

How Pre-Existing Conditions Affect Disability Insurance Underwriting

Let’s discuss pre-existing conditions and the role they play in the underwriting decision.

Generally speaking, if you have been diagnosed or treated for any health condition, the carrier excludes said health condition from coverage.

So, if you are taking Wellbutrin for depression, the carriers will exclude mental or nervous disorders from coverage.

Additionally, if you have migraines or hurt your back, those are excluded as well.

What, John?! That is wrong!

I understand. But, from the carrier’s perspective, it is not.

Think for a moment. If you were a disability insurance carrier, would you cover pre-existing conditions on someone?

I’ll answer. Probably not, unless you want to charge a lot of money, and you would have to. No one would pay those premiums, and you’d be out of business.

Additionally, if you have a chronic condition that is managed well with your physician team, do you think that condition will cause a disability?

Yes!

The right answer is you don’t know. A million ways a disability happens. It’s not just from your pre-existing condition. Yet, we tend to only focus on the pre-existing condition.

I bet the chances of a cancer diagnosis, injury, or another type of illness has an equal, or even better chance, than your managed illness.

Again, anything can happen anytime and a million ways exist for a disability to happen.

If you want to protect your family and loves ones, which is the main purpose of disability insurance, you will simply have to get around the pre-existing condition situation.

If you can’t, you possibly leave your family in a tough position. You can read more in our pre-existing conditions guide and contact us if you have questions.

Your Health History

Now that we got the pre-existing conditions situations out of the way, let’s discuss your health history.

Like any personal insurance (long-term care, life, supplemental health, etc.), your health history matters. Unlike life insurance, seemingly innocuous injuries or illnesses could affect the underwriter’s decision. For example, that shoulder injury that laid you up for a couple of months won’t affect your life insurance approval decision. However, the disability insurance carrier might exclude that shoulder and injury from coverage. Why? Because the injury prevented you from working before. Moreover, the possibility is greater for that injury to happen again.

health history matters. Unlike life insurance, seemingly innocuous injuries or illnesses could affect the underwriter’s decision. For example, that shoulder injury that laid you up for a couple of months won’t affect your life insurance approval decision. However, the disability insurance carrier might exclude that shoulder and injury from coverage. Why? Because the injury prevented you from working before. Moreover, the possibility is greater for that injury to happen again.

You might be thinking, “This stinks, John. #^$% disability insurance!”

Not so fast. Think about this:

Would you insure someone who you know has a high potential of disability shortly down the road? Your answer should be “no”. If yes, you would be fast out of business.

Moreover, consider this: most disabilities are from illnesses rather than injuries. That is right. Illnesses like cancer or multiple sclerosis lead to many disability claims.

You also need awareness. If you have a chronic, pre-existing condition, chances are that condition will be reflected in the contract in some form or fashion. For example, if you have a history of depression, the carrier will likely exclude your condition from coverage. We discuss this more in the article.

Lastly, be honest about your health history. Carriers know when a person is lying. Underwriters review your application against databases such as the MIB, prescription drug history (discussed in more detail further), and even your driving records.

Your Occupation

This might be obvious. Your occupation matters in disability insurance underwriting. An accountant has a less risky job than a construction laborer, right?

Nearly all carriers classify your occupation from 1 to 5 (or 6) with 5/6 being the best. In other words, the higher the number, the lower the disability risk of your occupation. Moreover, the lower the disability risk…you got it, the lower the premium, all things being equal.

That means if you are a skilled tradesman, you pay a higher premium compared to an accountant.

Regardless of your occupation, you should still enroll in a policy, even if you have to pay a higher premium. Why? A disability strikes anytime.

While occupational disabilities happen – and they happen all the time – they are not the #1 disability claim. As mentioned earlier, illnesses cause a majority of disabilities.

Depending on your occupation and situation, some carriers upgrade your occupation.

Your Income

Of course, your income matters. The higher you make, the higher your premium. It’s that simple.

Is this a bad thing? No! Remember, we are insuring your income in case you can’t work due to a disability.

Is this a bad thing? No! Remember, we are insuring your income in case you can’t work due to a disability.

If you don’t want to pay a high premium, you can always reduce your monthly benefit. For example, if your income allows you to have a $6,000 per month benefit, but you only want $3,000, then you can do that. The disadvantage is that, although you are paying a lower premium, you are potentially underinsured if you are disabled.

Remember, too, that you need to select the right income for disability insurance underwriting. If you are an employee, your income is your gross salary. Conversely, if you are a self-employed business owner, your income is your net income. (Moreover, anything else, such as your salary draw, etc.)

Your Prescription Drug History

You submit the application. One of the first things the carrier does is look up your prescription drug history.

This is private information; however, the carriers have access to it through Milliman Intelliscript.

Temporary prescription drugs probably won’t matter in the application. For example, if you took an antibiotic 2 years ago, the carrier may want to know what that was for. However, it should not matter unless it is a serious drug.

example, if you took an antibiotic 2 years ago, the carrier may want to know what that was for. However, it should not matter unless it is a serious drug.

Your prescription drug usage is not a secret. Disability insurance carriers rely on electronic data. Think you can avoid it? No. When you sign the application, you agree to let the carrier review your prescription drug history.

How does your prescription drug history work? Let’s say you have high blood pressure. You forgot to mention your high blood pressure on the disability insurance application, though. The underwriter sees your prescription drug history. She sees you are currently taking lisinopril. Next, she contacts you to find out more because you answered “no” on the application.

FYI – you don’t want the underwriter to do any more work than he or she has to. Again, it is best for honesty with your agent and on the application.

Your “Fun” Activities

All work and no play burns you out, right? We all need extracurricular activities. They recharge us. However, some activities are deemed too risky by insurance carriers. They include, but are not limited to:

- skydiving

- hang-gliding

- motor-vehicle racing

- scuba diving (beyond 100 ft usually)

- rock climbing

- mountaineering

- anything else like this

Depending on the frequency and degree of participation, the carrier will exclude your activity from the policy or decline your application altogether. In other words, if you like to rock climb, any disabling injury from rock climbing is not covered.

your activity from the policy or decline your application altogether. In other words, if you like to rock climb, any disabling injury from rock climbing is not covered.

However, don’t worry here. We have insured MANY professionals who engage in hazardous extracurricular activities. We tell them upfront about the exclusion (see what I wrote earlier).

Sounds good, John, you say. But, what if I join after the policy is issued?

Good question. You are likely covered 100%. However, the carrier will probably investigate before paying a benefit. It wants to see if you participated before the application and lied. Trust me; carriers have ways of finding out. If this is the case, the carrier will deny any disability benefit claim.

However, if not, then no worries.

Again, the moral of the story: be honest on your application.

Anything Else?

Could mean a lot of things.

One lately, in particular, is the recreational use of marijuana. While many states have approved the use of recreational marijuana, it is not approved at the federal level. Knowing this, and the risk behind it, carriers usually consider marijuana use as tobacco (i.e. smoker status) and apply a rating, depending on the use.

They will even decline your application for excessive use.

Moreover, while in some cases, your application can go through non-medical underwriting, the carrier may require a urine sample to test your level of THC.

Additionally, carriers will look up your credit and any bankruptcy. If you have a history of bankruptcies or severe credit issues, carriers will decline the application.

Disability Insurance Underwriting Fails And Pitfalls

We have helped many white, blue, and gray-collar professionals obtain disability insurance.

We have seen, almost, every underwriting scenario and situation.

Below is a list of pitfalls. You need to be aware of these. These probably won’t lead to an application decline. However, they will lead to adjusted benefits and/or exclusions.

If these scenarios apply to you, that’s no need to ignore disability insurance. Just be aware of these possible exclusions and limitations.

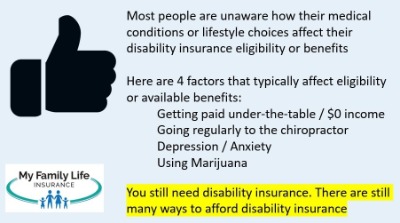

You Get Paid Under-The-Table

Carriers insure income. We addressed income earlier. If you get paid under-the-table, you are out of luck.

Carriers insure income. We addressed income earlier. If you get paid under-the-table, you are out of luck.

You need to show earned income through a W-2 or positive net income through your tax returns.

If you make no money or get paid under the table…sorry. You don’t report it, so the money isn’t insurable.

It’s no problem, John, you say. I just won’t provide the information.

Well, think again.

Let’s say you get paid under-the-table. You trick the carrier, and they issue a policy.

A year later, you get in an accident. You file a disability claim, and the carrier requests your income tax return.

Uh-oh…

Moreover, they may even cancel or rescind your policy.

If you are serious about disability insurance – and you should be – the remedy here is simple. Record your income properly.

You Go To The Chiropractor

Seems benign, right? You routinely go to the chiropractor for a spine adjustment. It also feels good. There’s nothing wrong with your back, of course.

That’s not how carriers see it.

Every application has a question like this:

“In the past 5 years, have you ever consulted another healthcare provider, chiropractor, therapist, counselor, psychiatrist, or psychologist?”

Here is the carrier’s point of view: Chiropractors are doctors, right? Why would you go? For fun? Nah…there must be a problem with your back.

In other words, you have a back and spine issue. Most carriers simply apply a back and spine exclusion to your policy.

However, you don’t see it that way. You go to the chiropractor because it keeps your back strong. You feel it prevents a back disability from happening.

So, first, let’s just say, in general, that chiropractor visits lead to a back and spine exclusion.

However, a few carriers have taken a more lenient approach to chiropractic visits.

If you only go a few times a year, just for “maintenance” and no documented back issues, a few carriers won’t exclude coverage.

However, if you go a lot, let’s say more than 6 times per year, carriers will exclude your back and spine from coverage.

That is just how it works. Think about it. If you go like 12 times a year, that is 1 time per month. That is a lot. Anyone would think you have a back or spine issue, even if you like going and the adjustment feels good.

Contact us, let us know your occupation, and we can help.

You Have Documented Depression Or Anxiety

This is a tricky area. We receive many phone calls from folks who take first-line medication for depression and/or anxiety. The pandemic hasn’t helped, either, with a significant increase in depression and anxiety in young adults.

We are always upfront. What I tell them is that nearly all the carriers limit your benefit to a 90-day waiting period / elimination period and a maximum 5-year benefit period.

Additionally, they place an exclusion. Any disabilities arising from any emotional or nervous disorder aren’t covered. This includes substance and drug abuse.

Usually, the carriers don’t budge.

Why is that? That doesn’t seem fair…

Same here. I understand. I have spoken to nearly all of them about it. Rather than try to explain here their reasons (as it gets really detailed), contact us, and I am happy to discuss.

But, John. I am prescribed anxiety medication to help me sleep only.

Doesn’t matter. If you are taking anxiety medication to help you sleep, then you have anxiety. That’s the way carriers see it. If it’s hard for you to fall asleep, and you need medication to help you with that, then that is anxiety and an exclusion.

This is another example of stringent disability insurance underwriting. With life insurance, a first-line medication for controlled anxiety and/or depression is no big deal. However, remember, carriers are insuring your chance of disability.

As an aside, we have helped many people maneuver this situation and still have disability insurance. Please see our topic on removing exclusions below for more detail.

You Smoke or Use Marijuana

As of this writing, getting life insurance with marijuana use is no big deal.

However, this is not the case with disability insurance.

I can write an entire blog about disability insurance and marijuana use.

Many disability insurance carriers will decline an application from someone who uses marijuana.

Sure, it might be legal in your state. But, it is not on a federal level.

This is an evolving scenario. I predict carriers will be more lenient with people who use marijuana. However, currently, there are a few carriers that will insure people who use marijuana. But, at tobacco use rates.

John. That’s OK, you say. I will just hide the information.

Think again. If you file a disability claim, and the carrier finds out you are a marijuana user, likely the claim is denied.

Listen, we have helped people who use marijuana obtain disability insurance. We can help you, too. Just contact us.

Can Carriers Remove Exclusions In Disability Insurance Underwriting?

The short answer. Yes!

However, it is not that easy.

Moreover, the ability to remove exclusions depends on the situation. It’s possible, though.

Here’s a real story. A doctor prescribed a client of ours anxiety medication during her college years. Our client felt anxious about school, etc. So, the doctor prescribes medication.

She’s out of school now and contacted us about disability insurance.

Of course, we explained how carriers underwrite people diagnosed with anxiety. In her case, however, her and her doctor felt that was a one-time situation. Our client hadn’t taken the medication for awhile, either.

In her case, the carrier placed the 90 day / 5 year benefit period with the exclusion. However, we discussed reviewing in 2 years. If the client demonstrates no need for the medication, the carrier will remove the exclusion.

So, yes. Exclusions can be removed. But, you will need to show you are no longer requiring or participating. If you like going to the chiropractor, you’ll have to stop going. If you like rock climbing, you’ll have to stop that, too.

Some exclusions probably could never be removed. These are moderate to serious illnesses like bipolar disorder, rheumatoid arthritis, alcoholism, etc.

Why A Modified Policy Is Better Than No Policy

As stringent as disability insurance underwriting is, we have been able to help people with moderate to serious health conditions. We have helped people with bipolar depression, moderate anxiety, previous cancer diagnosis, and more.

When you work with us, and you have a unique situation, we contact the underwriters directly and discuss your situation. We don’t give them your name or anything like that, so your personal information is safe.

However, you may be thinking,“@$^# this! I’m not going to go through this!”

Well, you may be doing a disservice.

Remember, who is behind this disability insurance? Well, it is you. And then your family, and then your life.

If you are disabled, and can’t work, how will you pay your bills?

Well, will you tap into retirement savings – and destroy your future?

Will you sell your home – and destroy your future?

Will you rack up debt – and destroy your future?

Do you see what I am getting at? There is no good alternative, except for taking a modified or rated policy that will still pay a percentage of your income. The peace of mind is invaluable.

Yes, there is John, you say. I will just invest!

So, FYI I am a CFP® Professional, and I know how hard it is for people to save. Be honest with yourself, will you? I doubt it.

Just look at this example.

The Math – How Savings Doesn’t Work

Even if you dedicated yourself, the amount is insurmountable.

For example, let’s say you are eligible for a $5,000 monthly benefit, 5-year benefit period. You make $90,000 per year. You are age 45. The premium is $132 per month.

However, because of health conditions, the carrier rates you, and your premium is now $210 per month for the same $5,000 benefit. Is it a good deal? Absolutely! Let’s put some math behind it.

In that 5-year benefit period, you are insuring up to $300,000 of income ($5,000 per month X 12 months X 5 years). That’s a lot. Think about how your life changes having that safety net.

The obvious non-math answer is: if you were disabled tomorrow, do you have $300,000 dedicated (not your home or retirement) to support you? The answer I know is “no”. (This is why it makes sense to take a modified policy). But on with the analysis…

Results

Do you know how long it will take to insure your income by investing? At $132 per month and a conservative 5% annual return (why would you put risk if you need this money), it will take you 47 years to save $300,000 at $132 per month!!!

Do you think you will do better by saving $210 per month?

No.

It will take you only 38 years.

And, what will you do if you are disabled with no policy?

Just for your knowledge, let’s say you dedicated to saving $300,000 in 10 years as a disability fund. So age 55 through your retirement age, you have some protection in case of disability. At a 5% annual return, you will need to save almost $2,000 per month! That is $24,000 per year and probably 1/3 of your take-home pay. Yikes!

Let’s say you only have that $210 to save, well, you need an annual return (over 10 years) of 40% each year. That is just not going to happen unless you are extremely speculative with your money.

The math doesn’t work. Taking a modified policy is the right choice.

Back To Accepting A Modified Policy

This is the reason why you need to take a modified policy. You don’t know when you will be disabled. Additionally, it takes a very long time to save that money, if you even can.

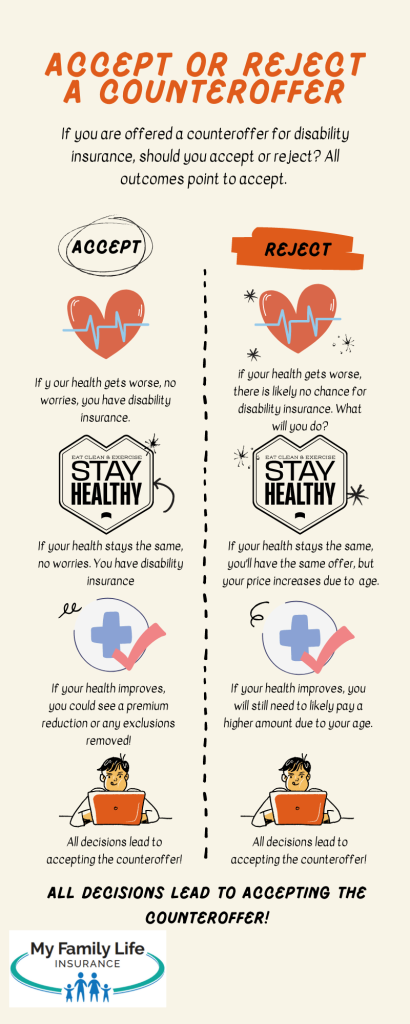

Here is a succinct illustration, which shows your options if you accept or do not accept a modified disability insurance policy. All points to accept.

What If I Am Declined For Disability Insurance?

What if you go through the underwriting process, and you are still declined for disability insurance? You still have options. (Note: we really don’t let our clients go through all that first. If you have moderate to serious medical conditions, we tell you and/or contact the underwriters for eligibility.)

However, if you are declined for disability insurance or seeking other options, let us know. We have helped people with alternative options for disability insurance. Although these options are not ideal, they will provide some benefits.

These options include critical illness insurance and hospital indemnity insurance. Additionally, we do offer guaranteed issue disability insurance based on your situation.

If you are a business owner, we do have guaranteed issue disability insurance options.

Now You Know How Disability Insurance Underwriting Works So You Can Get Approved Today!

We hope this article explained the disability insurance underwriting process better and how to get approved today!

Although the underwriting is more stringent, there is nothing to worry about or fear. We help you along the way.

Now that you are aware of disability underwriting, are you ready to take the next step? Contact us or use the form below if you would like our assistance in helping you find the right disability insurance policy. As we mentioned earlier, we have helped many individuals, even those with health conditions, obtain important disability insurance. As with everything we do, we always have your best interests.

Learn More

Are you interested in learning more about the information in this article? Please fill out the form below, and we will email you additional information or give you a call. We always work in your best interest. By entering your information, you are providing your express consent that My Family Life Insurance may contact you via e-mails, SMS, phone calls, or prerecorded messages at any phone number(s) that you provide, even if the number is a wireless number or on any federal or state do-not-call list. Additionally, you understand that calls may be placed using automated technology, and that consent is not a requirement for purchase. Your information will NOT be sold and will remain private. However, you may opt out at any time. We respect your privacy first and foremost. By contacting us, you agree to receive text messages from our number (800) 645-9841. If you no longer wish to receive text messages, you may opt out at any time by replying "STOP".